Get In-Demand Finance Certifications

An approach used to assess the total cost of owning a facility or running a project

Life cycle cost analysis (LCCA) is an approach used to assess the total cost of owning a facility or running a project. LCCA considers all the costs associated with obtaining, owning, and disposing of an investment.

Life cycle cost analysis is especially useful where a project comes with multiple alternatives and all of them meet performance necessities, but they differ with regards to the initial, as well as the operating, cost. In this case, the alternatives are compared to find one that can maximize savings.

For example, LCCA helps to determine which of the two alternatives will raise the initial cost but will reduce the operating cost. However, LCCA should not be used for the purpose of budget allocation.

Life cycle cost analysis is ideal for estimating the overall cost of a project’s alternatives. It is also used to choose the right design to ensure that the chosen alternative will offer a lower overall ownership cost that is consistent with function and quality.

LCCA needs to be performed during the initial stages of the design process, as there is room to make changes and refinements that will ensure that the life cycle cost is reduced. The first step when performing an LCCA is determining the economic impact of the alternatives available. The effects are then quantified and expressed in monetary terms.

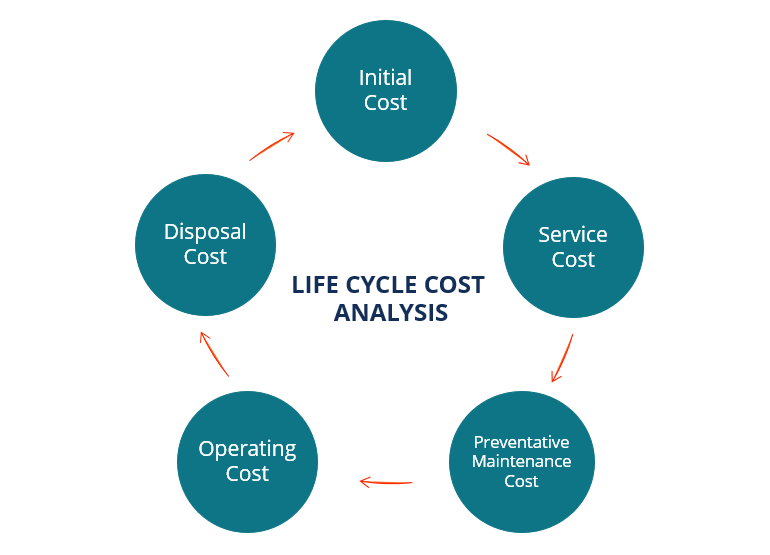

Various costs arise when procuring, operating, or disposing of a project. Project-related costs can be classified into initial costs, fuel costs, replacement costs, operation and maintenance costs, finance charges, and residual values.

Only relevant and significant costs in each of the categories above can be used to make investment-related decisions. Costs are considered significant when they are substantial enough to cause a dependable impact on a project’s LCC.

All the costs involved are treated as base year values equivalent to present-day dollar amounts; LCCA transforms all dollar values into future year occurrence equivalents and then discounts all the values to their base dates. In such a way, it’s easy to find their present value.

Life cycle cost analysis can be used to assess different infrastructural sectors such as rail and urban transport, airports, highways, and ITS, as well as ports and industrial infrastructure. Such kinds of projects make use of capital expenditure, which is the initial cost involved when constructing or delivering an infrastructural asset. Simply put, it is the cost of construction for the infrastructure of choice.

The other thing that is important in infrastructural development is operating expense, which consists of a number of costs, including utility, manpower, insurance, equipment, health, and routine and planned repairs.

Replacement costs are incurred every cycle based on the predefined age of replacement for different assets and the manufacturer’s preference.

Probably another important element of LCCA is disposal cost. When the disposal cost is incorporated, it is possible to offset any additional cost incurred during a particular year.

Rigorous modeling based on LCCA incorporates value engineering so that a project’s cost outline can lower expenditures by a huge margin. The procedures are done through a series of tests on the cost of operation.

Modeling using LCCA requires a lot of flexibility when adjusting the types of costs associated with materials and assets used in a project over its lifetime. That way, a developer can access all the information relating to the financial impact connected with choosing a combination of project options.

Value engineering offers the potential to assist developers in choosing the right material and assets. Since a material or asset may come with a unique specification with regards to maintenance and the cost of acquisition, their overall characteristics will not be the same.

For example, the most expensive asset may provide superior performance and quality but will require a significant amount of maintenance. On the other hand, a cheaper material or asset may require less regular maintenance, but its overall cost is significantly lower.

Further simulation can be carried out to ascertain the timing of financial responsibilities in the different phases of an asset’s useful life. Using LCCA in the right way can help users identify development groupings that can lead to favorable timing of financial exposure.

By using LCCA when carrying out tests, comparisons, and analyses, a user can work out enhanced development arrangements for infrastructural projects that offer a favorable financial experience and cost profile.

Life cycle cost analysis offers a general framework that can be used to assess the need for additional costs during a project’s useful life. With such knowledge in mind, it is possible to regulate cash outflows by forecasting the requirements of a project.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Life Cycle Cost Analysis. To keep learning and advancing your career, the following CFI resources will be helpful: