Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

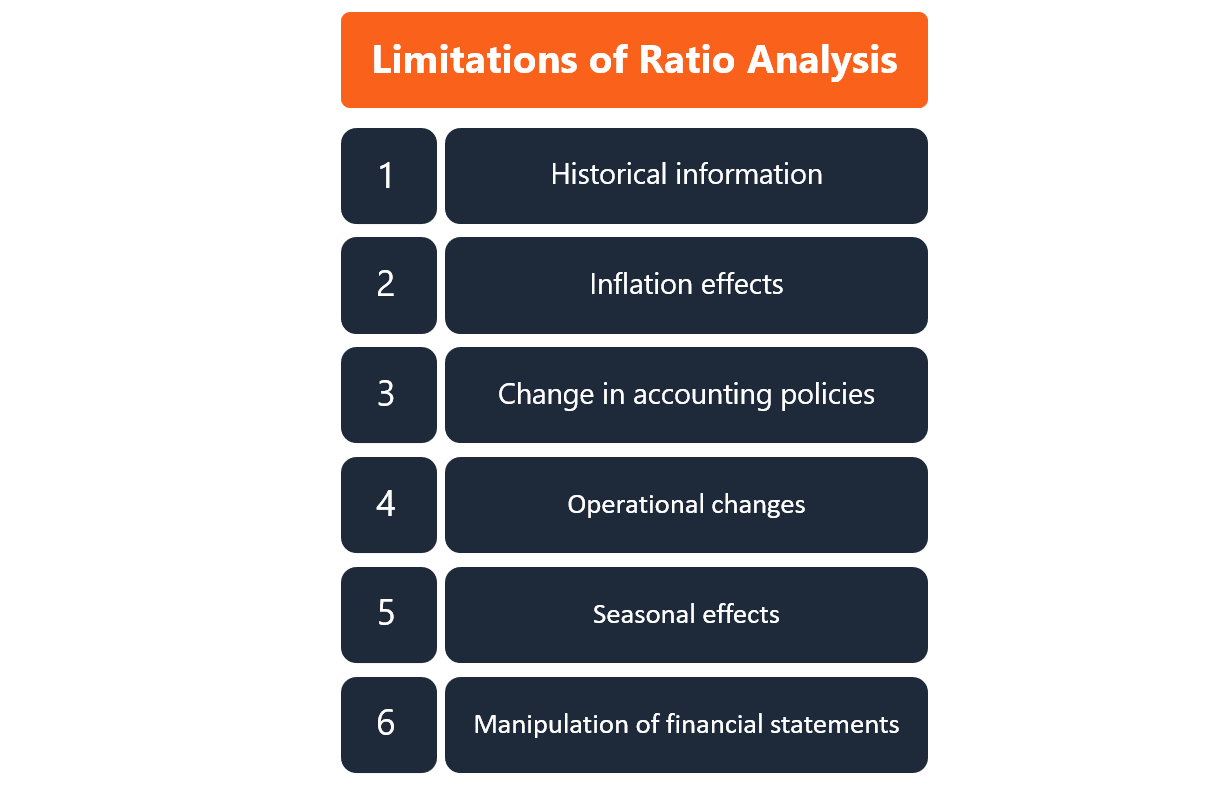

Factors that limit the efficacy of ratio analysis

Ratio analysis is a popular technique of financial analysis. It is used to visualize and extract information from financial statements. It focuses on ratios that reflect profitability, efficiency, financing leverage, and other vital information about a business. The ratios can be used for both horizontal analysis and vertical analysis. While they are a popular form of analysis, there are many limitations of ratio analysis that financial analysts should be aware of.

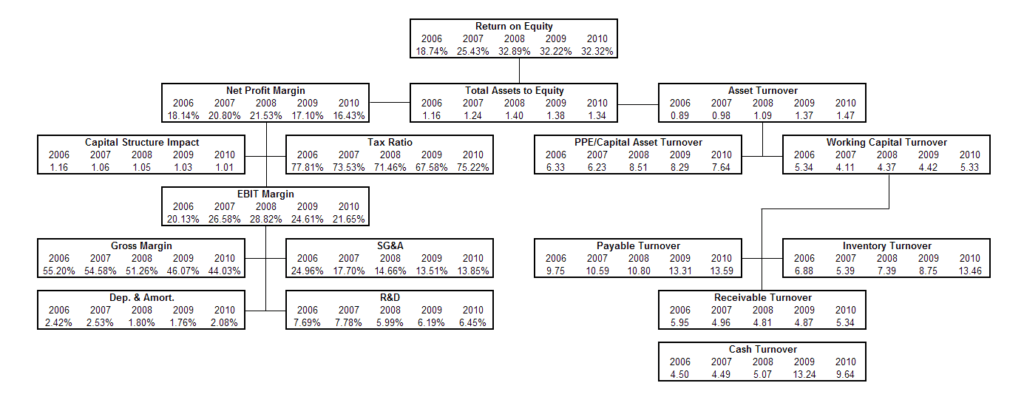

Image: Pyramid of Ratios from CFI’s Financial Analysis Course.

One of the key factors in ratio analysis is the comparison to the benchmark companies of an industry. This type of financial analysis can be useful to both internal management and outsider analysts of the company, as it provides significant insights from the financial statements.

As with any financial analysis technique, there are several limitations of ratio analysis. It is crucial to know these limitations to avoid misleading conclusions.

Some of the most important limitations of ratio analysis include:

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to the limitations of ratio analysis. To keep learning and advancing your career, the following CFI resources will be helpful: