Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Occurs when a company owns greater than 50% of another company, but not 100%

A non-controlling interest (NCI) typically occurs when a company owns more than 50% of another company but less than 100%. Since the first company (parent company) effectively controls the second company (subsidiary company), the parent will fully consolidate the subsidiary’s financials with its own.

As an example, assume Company A owns 75% of Company B: This creates a 25% non-controlling interest in Company B. Company A will fully consolidate its financials with Company B. In other words, Company A will claim 100% of Company B’s revenues and expenses and assets and liabilities. However, Company A will allocate 25% of Company B’s net income to the 25% non-controlling interest in Company B. There will also be a non-controlling interest in Shareholder’s Equity on the balance sheet.

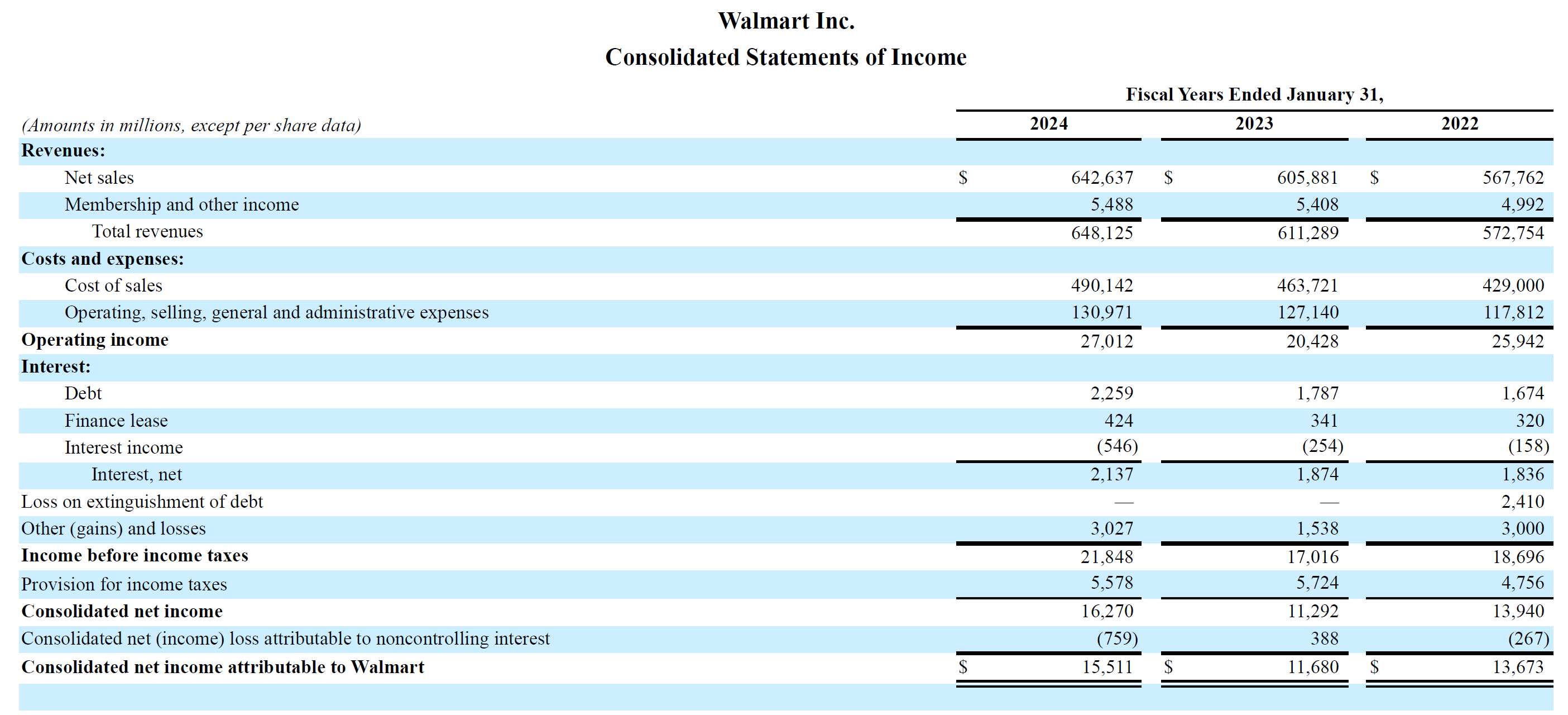

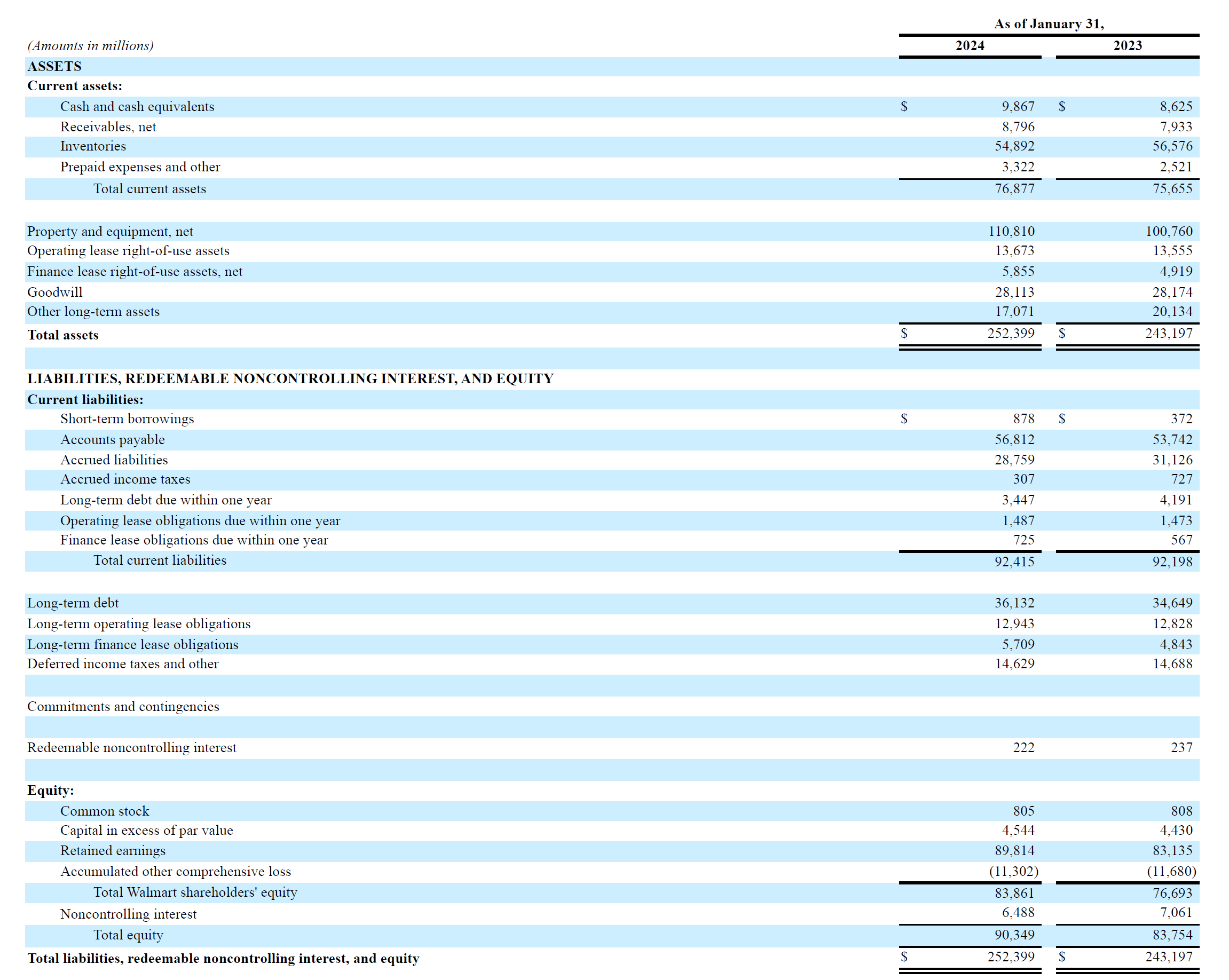

Below, you can see an example of how non-controlling interest is reported on both Walmart’s income statement and balance sheet. Non-controlling interest was formerly known as minority interest.

Source: Walmart 2024 10-K

Source: Walmart 2024 10-K

Non-controlling interest typically occurs when one company owns greater than 50% of another company but not 100%. Since the first company has greater voting power, it effectively controls the second company. However, this ownership level is just a rule of thumb. A company may still consolidate another company’s financials even if it owns less than 50%. This may occur if the consolidating company controls the subsidiary’s board of directors and is, therefore, able to direct the subsidiary’s business decisions.

Valuing a company requires financial statements to better forecast future trends around profits and cash flows. Unfortunately, companies with a non-controlling interest prepare consolidated financials and rarely disclose enough information to properly value the NCI. However, analysts can still attempt to value NCI using some of the methods discussed below.

The constant growth method is seldom used because the assumption is that there is hardly any decline or growth in the performance of the subsidiary company.

In the historical growth method, previous financials are analyzed to ascertain existing trends. The model predicts the growth of a subsidiary at a rate based on past trends. However, this method is not applicable to companies experiencing dynamic growth or severe decline.

This analysis method evaluates each subsidiary on its own and then adds up the individual interests of each subsidiary to achieve a consolidated value. This method is much more flexible, and the results may be theoretically more accurate.

Unfortunately, it is quite difficult to perform due to a lack of disclosures by the parent company. In addition, if a company has many subsidiaries, then it may not be worth the time and effort to try and value each one.

Assuming markets are efficient and a stock is fairly priced, a company’s market cap reflects the parent’s partial ownership of a consolidated subsidiary. Therefore, when calculating enterprise value, an analyst needs to add the non-controlling interest to the market cap. This is because enterprise value is often used in valuation multiples like EV/EBITDA.

Since EBITDA includes 100% of the non-controlling interest’s EBITDA, then adding NCI to the market cap when calculating enterprise value makes the numerator and denominator consistent (both now reflect 100% of the subsidiary). The bottom line is to include non-controlling interest when calculating enterprise value.

It is important to investors that companies provide transparency regarding non-controlling interests because it will give them a better understanding of the effect of the NCI on a group’s financial position, financial results, and cash flows, as well as the risks faced by the group. Investors will then be better positioned to form their own opinion regarding the impact of NCI on the parent company.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.