Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

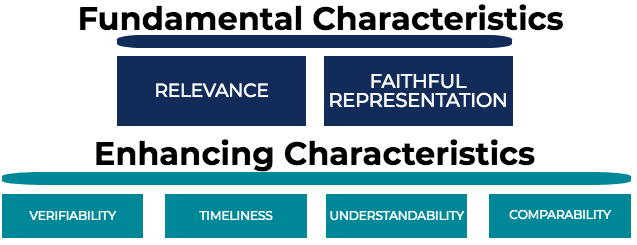

The fundamental (primary) and enhancing (secondary) qualitative characteristics

The demand for accounting information by investors, lenders, creditors, etc., creates fundamental qualitative characteristics that are desirable in accounting information. There are six qualitative characteristics of accounting information. Two of the six qualitative characteristics are fundamental (must have), while the remaining four qualitative characteristics are enhancing (nice to have).

Qualitative characteristics of accounting information that must be present for information to be useful in making decisions:

We will look at each qualitative characteristic in more detail below.

Relevance refers to how helpful the information is for financial decision-making processes. For accounting information to be relevant, it must possess:

Therefore, accounting information is relevant if it can provide helpful information about past events and help in predicting future events or in taking action to deal with possible future events. For example, a company experiencing a strong quarter and presenting these improved results to creditors is relevant to the creditors’ decision-making process to extend or enlarge credit available to the company.

Representational faithfulness, also known as reliability, is the extent to which information accurately reflects a company’s resources, obligatory claims, transactions, etc. To help, think of a pictorial depiction of something in real life – how accurately does the picture represent what you see in real life? For accounting information to possess representational faithfulness, it must be:

Qualitative characteristics of accounting information that impact how useful the information is:

Verifiability is the extent to which information is reproducible given the same data and assumptions. For example, if a company owns equipment worth $1,000 and told an accountant the purchase cost, salvage value, depreciation method, and useful life, the accountant should be able to reproduce the same result. If they cannot, the information is considered not verifiable.

Timeliness is how quickly information is available to users of accounting information. The less timely (thus resulting in older information), the less useful information is for decision-making. Timeliness matters for accounting information because it competes with other information. For example, if a company issues its financial statements a year after its accounting period, users of financial statements would find it difficult to determine how well the company is doing in the present.

Understandability is the degree to which information is easily understood. In today’s society, corporate annual reports are in excess of 100 pages, with significant qualitative information. Information that is understandable to the average user of financial statements is highly desirable. It is common for poorly performing companies to use a lot of jargon and difficult phrasing in its annual report in an attempt to disguise the underperformance.

Comparability is the degree to which accounting standards and policies are consistently applied from one period to another. Financial statements that are comparable, with consistent accounting standards and policies applied throughout each accounting period, enable users to draw insightful conclusions about the trends and performance of the company over time. In addition, comparability also refers to the ability to easily compare a company’s financial statements with those of other companies.

The qualitative characteristics of accounting information are important because they make it easier for both company management and investors to utilize a company’s financial statements to make well-informed decisions.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide on Qualitative Characteristics of Accounting Information. To keep learning and advancing your career, the following resources will be helpful: