Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

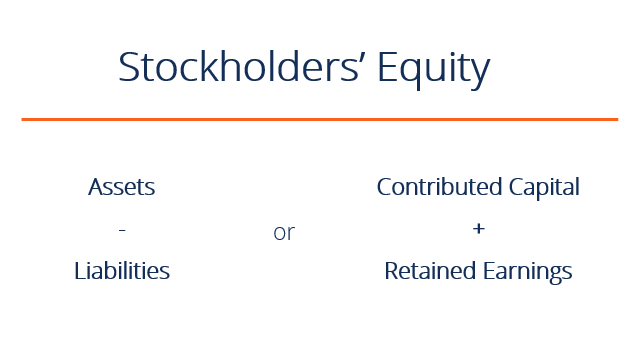

Share capital plus retained earnings

Stockholders Equity (also known as Shareholders Equity) is an account on a company’s balance sheet that consists of share capital plus retained earnings. It also represents the residual value of assets minus liabilities. By rearranging the original accounting equation, Assets = Liabilities + Stockholders Equity, it can also be expressed as Stockholders Equity = Assets – Liabilities.

Stockholders Equity provides highly useful information when analyzing financial statements. In events of liquidation, equity holders are last in line behind debt holders to receive any payments. This means that bondholders are paid before equity holders.

Therefore, debt holders are not very interested in the value of equity beyond the general amount of equity to determine overall solvency. Shareholders, however, are concerned with both liabilities and equity accounts because stockholders equity can only be paid after bondholders have been paid.

Stockholders Equity is influenced by several components:

Share Capital (contributed capital) refers to amounts received by the reporting company from transactions with shareholders. Companies can generally issue either common shares or preferred shares. Common shares represent residual ownership in a company and in the event of liquidation or dividend payments, common shares can only receive payments after preferred shareholders have been paid first.

If a company were to issue 10,000 common shares for $50 each, the contributed capital would be equal to $500,000. The journal entry would be:

DR Cash 500,000

CR Common Shares 500,000

In addition to shares being sold for cash as in the previous example, it is also common to see companies selling shares on a subscription basis. In these situations, the buyer usually makes a down payment on purchasing a certain number of shares and agrees to pay the remaining amount at a later date. For example, if XYZ Company sells 10,000 common shares for $10 each on a subscription basis that requires the buyer to pay $3 per share when the contract is signed and the remaining balance 2 months later, the journal entry would appear as follows:

DR Cash 30,000

DR Share Subscriptions Receivable 70,000

CR Common shares subscribed 100,000

The share subscriptions receivable functions similar to the accounts receivable (A/R) account. Once the receivable payment is paid in full, the common shares subscribed account is closed and the shares are issued to the purchaser.

DR Cash 70,000

CR Share Subscriptions Receivable 70,000

DR Common shares subscribed 100,000

CR Common Shares 100,000

A few more terms are important in accounting for share-related transactions. The number of shares authorized is the number of shares that the corporation is allowed to issue according to the company’s articles of incorporation. The number of shares issued refers to the number of shares issued by the corporation and can be owned by either external investors or by the corporation itself.

Finally, the number of shares outstanding refers to shares that are owned only by outside investors, while shares owned by the issuing corporation are called treasury shares.

The relationship can be visualized as follows:

Shares Authorized ≥ Shares Issued ≥ Shares outstanding

Where the difference between the shares issued and the shares outstanding is equal to the number of treasury shares.

Retained Earnings (RE) are business’ profits that are not distributed as dividends to stockholders (shareholders) but instead are allocated for investment back into the business. Retained Earnings can be used for funding working capital, fixed asset purchases, or debt servicing, among other things.

To calculate retained earnings, the beginning retained earnings balance is added to the net income or loss and then dividend payouts are subtracted. A summary report called a statement of retained earnings is also maintained, outlining the changes in retained earnings for a specific period.

The Retained Earnings formula is as follows:

Retained Earnings = Beginning Period Retained Earnings + Net Income/Loss – Cash Dividends – Stock Dividends

Learn more in CFI’s Retained Earnings guide.

Dividend payments by companies to its stockholders (shareholders) are completely discretionary. Companies have no obligation whatsoever to pay out dividends until they have been formally declared by the board. There are four key dates in terms of dividend payments, two of which require specific accounting treatments in terms of journal entries. There are various kinds of dividends that companies may compensate its shareholders, of which cash and stock are the most prevalent.

| Date | Explanation | Journal Entry |

| Declaration Date | Once the board declares a dividend, the company records an obligation to pay, through a dividend payable account | DR Retained Earnings

CR Dividends Payable |

| Ex-dividend Date | The date on which a share trades without the right to receive a dividend that has been declared. Prior to the ex-dividend date, an investor would be entitled to dividends. | No Journal Entry |

| Date of Record | The date when the company compiles the list of shareholders to receive dividends | No Journal Entry |

| Payment Date | When the cash or other form of dividend is actually paid to the shareholder | DR Dividends Payable

CR Cash |

With various debt and equity instruments in mind, we can apply this knowledge to our own personal investment decisions. Although many investment decisions depend on the level of risk we want to undertake, we cannot neglect all the key components covered above. Bonds are contractual liabilities where annual payments are guaranteed unless the issuer defaults, while dividend payments from owning shares are discretionary and not fixed.

In terms of payment and liquidation order, bondholders are ahead of preferred shareholders, who in turn are ahead of common shareholders. Therefore, from an investor’s perspective, debt is the least risky investment, and for companies, it is the cheapest source of financing because interest payments are deductible for tax purposes and also because debt generally offers a lower return to investors.

However, debt is also the riskiest form of financing for companies because the corporation must uphold the contract with bondholders to make the regular interest payments regardless of economic times.

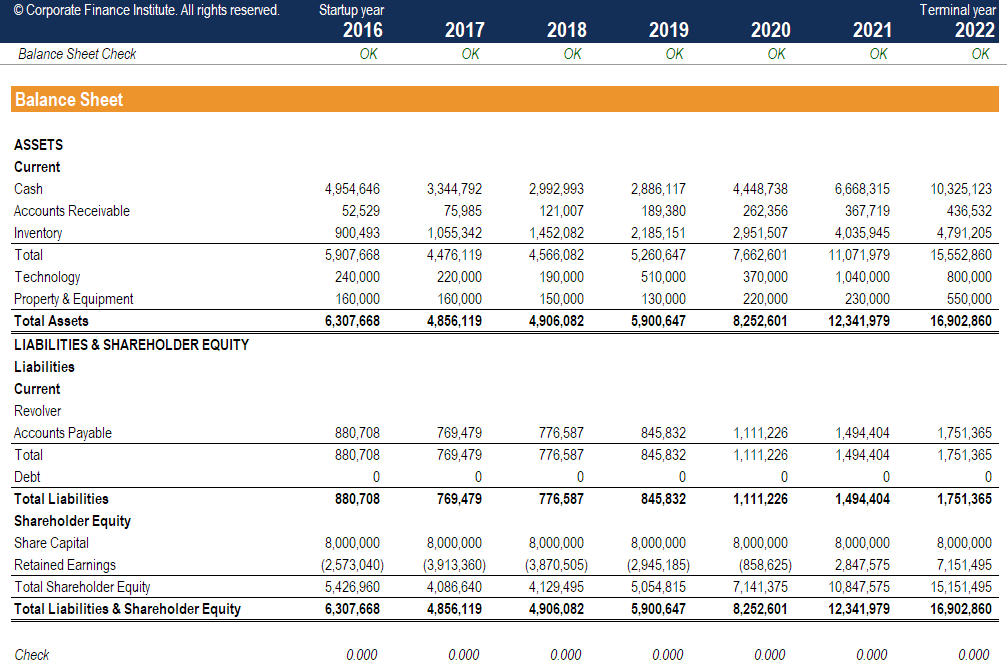

Calculating stockholders equity is an important step in financial modeling. This is usually one of the last steps in forecasting the balance sheet items. Below is an example screenshot of a financial model where you can see the shareholders equity line completed on the balance sheet.

To learn more, launch our financial modeling courses now!

Thank you for reading CFI’s guide to Stockholders equity. To keep learning and advancing your career, the following resources will be helpful:

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: