Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

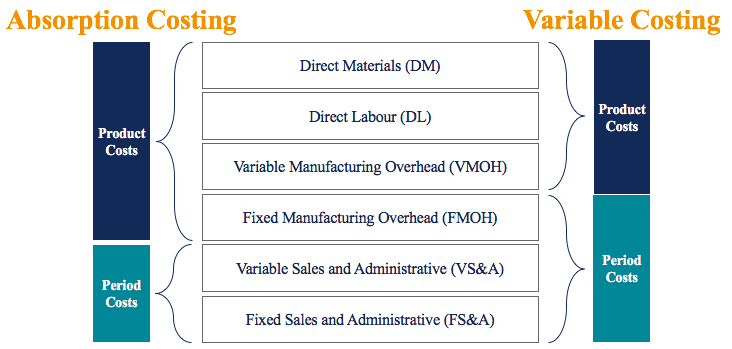

Fixed manufacturing overhead excluded from product-costs

Variable costing is a concept used in managerial and cost accounting in which the fixed manufacturing overhead is excluded from the product-cost of production. The method contrasts with absorption costing, in which the fixed manufacturing overhead is allocated to products produced. In accounting frameworks such as GAAP and IFRS, variable costing cannot be used in financial reporting.

Although accounting frameworks such as GAAP and IFRS prohibit the use of variable costing in financial reporting, this costing method is commonly used by managers to:

Under variable costing, the following costs go into the product:

Under absorption costing, the following costs go into the product:

For your reference, the diagram provided below provides an overview of which costs go into variable costing vs. absorption costing methods:

Note that product costs are costs that go into the product while period costs are costs that are expensed in the period incurred.

IFC is a manufacturer of phone cases. Below are excerpts from the company’s income statement for its latest year-end (2018):

IFC does not report an opening inventory. During 2018, the company manufactured 1,000,000 phone cases and reported total manufacturing costs of $598,000 (around $0.60 per phone case).

The manufacturer recently received a special order for 1,000,000 phone cases at a total price of $400,000. Despite having ample capacity, the manager is reluctant to accept this special order because it is below the cost of $598,000 to manufacture the initial 1,000,000 phone cases as outlined in the company’s income statement. Being the company’s cost accountant, the manager wants you to determine whether the company should accept this order.

First, it is important to know that $598,000 in manufacturing costs to produce 1,000,000 phone cases includes fixed costs such as insurance, equipment, building, and utilities. Therefore, we should use variable costing when determining whether to accept this special order.

Variable Costing:

Total = $305,000 / 1,000,000 units produced = $0.305 variable cost per case

Cost to produce special order of 1,000,000 phone cases = $0.305 x 1,000,000 = $305,000. Therefore, there is a contribution margin of $400,000 – $305,000 = $95,000.

Based on our variable costing method, the special order should be accepted. The special order will add $95,000 of profits to the company.

It is crucial to understand why the manager was reluctant to accept the order. The manager included fixed costs in the cost calculation, which is incorrect in decision-making. Given ample capacity, the company will not incur additional fixed costs to produce the special order of 1,000,000. As you can see, variable costing plays an important role in decision-making!

In accordance with the accounting standards for external financial reporting, the cost of inventory must include all costs used to prepare the inventory for its intended use. It follows the underlying guidelines in accounting – the matching principle. Absorption costing better upholds the matching principle, which requires expenses to be reported in the same period as the revenue generated by the expenses.

Variable costing poorly upholds the matching principle, as related expenses are not recognized in the same period as related revenue. In our example above, under variable costing, we would expense all fixed manufacturing overhead in the period occurred.

However, if the company fails to sell all the inventory manufactured in that year, there would be poor matching between revenues and expenses on the income statement. Therefore, variable costing is not permitted for external reporting. It is commonly used in managerial accounting and for internal decision-making purposes.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI offers the Financial Modeling & Valuation Analyst (FMVA)® certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following CFI resources will be helpful:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: