Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Also known as full costing (cost of materials, labor, and fixed and variable manufacturing overhead)

Absorption costing is a costing system that is used in valuing inventory. It not only includes the cost of materials and labor, but also both variable and fixed manufacturing overhead costs. Absorption costing is also referred to as full costing. This guide will show you what’s included, how to calculate it, and the advantages or disadvantages of using this accounting method.

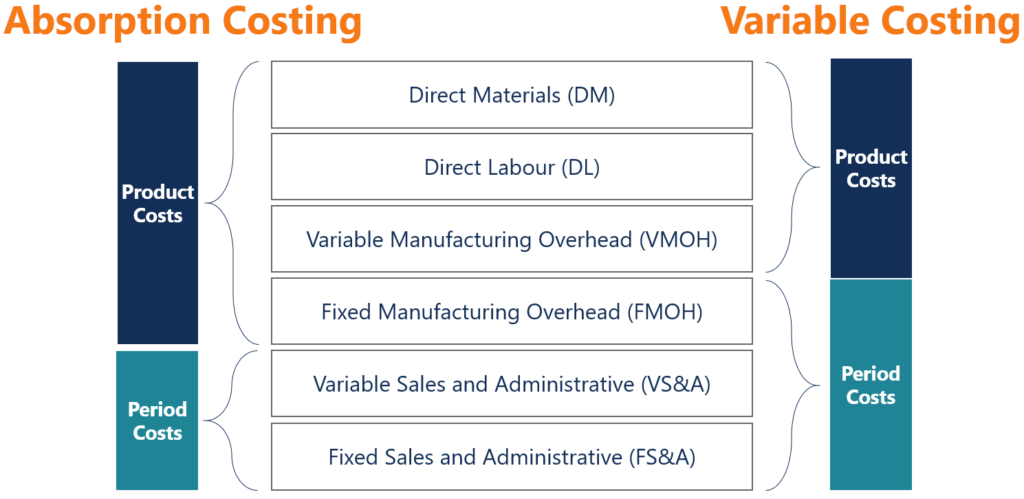

Under the absorption method of costing (aka “full costing”), the following costs go into the product:

Under absorption costing, the costs below are considered period costs and do not go into the cost of a product. They are, instead, expensed in the period occurred:

For your reference, the following diagram gives an overview of costs that go into absorption costing compared to variable costing:

Company A is a manufacturer and seller of a single product. In 2016, the company reported the following costs:

Over the year, the company sold 50,000 units and produced 60,000 units, with a unit selling price of $100 per unit.

Using the absorption method of costing, the unit product cost is calculated as follows:

Direct Materials + Direct Labor + Variable Overhead + Fixed Manufacturing Overhead Allocated = $25 + $20 + $10 + $300,000 / 60,000 units = $60 unit product cost under absorption costing

Recall that selling and administrative costs (fixed and variable) are considered period costs and are expensed in the period occurred. Those costs are not included in the product costs.

There are several advantages to using full costing. Its main advantage is that it is GAAP-compliant. It is required for preparing financial statements and for stock valuation.

In addition, absorption costing takes into account all costs of production, such as fixed costs of operation, factory rent, and the cost of utilities in the factory. It includes direct costs, such as direct materials or direct labor, and indirect costs, such as the plant manager’s salary or property taxes. It can be useful in determining an appropriate selling price for products.

Since absorption costing includes allocating fixed manufacturing overhead to the product cost, it is not useful for product decision-making. Absorption costing provides a poor valuation of the actual cost of manufacturing a product. Therefore, variable costing is used instead to help management make product decisions.

Absorption costing can skew a company’s profit level because not all fixed costs are subtracted from revenue unless the products are sold. By allocating fixed costs into the cost of producing a product, the costs can be hidden from a company’s income statement in inventory. Hence, absorption costing can be used as an accounting trick to temporarily increase a company’s profitability by moving fixed manufacturing overhead costs from the income statement to the balance sheet.

For example, recall that the company incurred fixed manufacturing overhead costs of $300,000. If a company produces 100,000 units (allocating $3 in FMOH to each unit) and only sells 10,000, a significant portion of manufacturing overhead costs would be hidden in inventory in the balance sheet. If the manufactured products are not all sold, the income statement would not show the full expenses incurred during the period.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading this guide to calculating the full costing of inventory. To keep learning and developing your knowledge base, please explore the additional relevant resources below: