Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

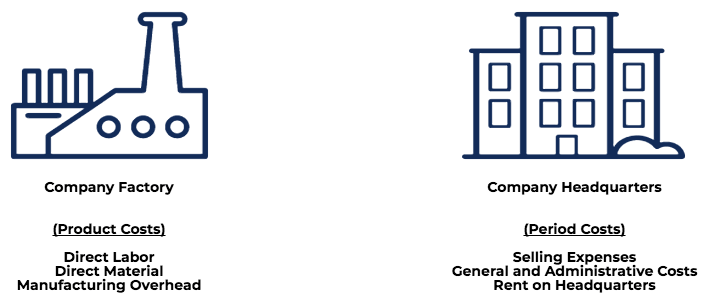

Costs incurred in manufacturing a product

Product costs are costs that are incurred to create a product that is intended for sale to customers. Product costs include direct material (DM), direct labor (DL), and manufacturing overhead (MOH).

Product costs are the costs directly incurred from the manufacturing process. The three basic categories of product costs are detailed below:

Direct material costs are the costs of raw materials or parts that go directly into producing products. For example, if Company A is a toy manufacturer, an example of a direct material cost would be the plastic used to make the toys.

Direct labor costs are the wages, benefits, and insurance that are paid to employees who are directly involved in manufacturing and producing the goods – for example, workers on the assembly line or those who use the machinery to make the products.

Manufacturing overhead costs include direct factory-related costs that are incurred when producing a product, such as the cost of machinery and the cost to operate the machinery. Manufacturing overhead costs also include some indirect costs, such as the following:

Company A is a manufacturer of tables. Its product costs may include:

Company A produced 1,000 tables. To produce 1,000 tables, the company incurred costs of:

Total product costs: $12,000 (direct material) + $2,000 (direct labor) + $100 (indirect material) + $500 (indirect labor) + $500 (other costs) = $15,100. As this is the cost to produce 1,000 tables, the company has a per unit cost of $15.10 ($15,100 / 1,000 = $15.10).

Product costs are costs necessary to manufacture a product, while period costs are non-manufacturing costs that are expensed within an accounting period.

| Definition | Costs incurred to manufacture a product | Costs that are not incurred to manufacture a product and, therefore, cannot be assigned to the product |

| Components | Manufacturing and production costs | Non-manufacturing costs |

| Examples | Raw material, wages on labor, production overheads, rent on the factory, etc. | Marketing costs, sales costs, audit fees, rent on the office building, etc. |

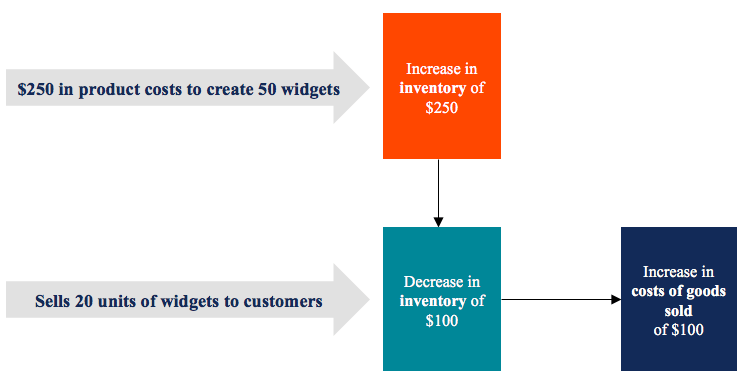

Consider the diagram below:

Product costs are treated as inventory (an asset) on the balance sheet and do not appear on the income statement as costs of goods sold until the product is sold.

For example, a company manufactures 50 units of widgets at a unit product cost of $5. On the balance sheet, there would be a $5 x 50 = $250 increase in inventory. If the company sells 20 units of widgets, $5 x 20 = $100 in inventory would be transferred to the cost of goods sold on the income statement while the remaining $150 would remain in inventory on the balance sheet.

Click the button below to download our free Product Costs template!

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide on Product Costs. To keep learning and advancing your career, the following resources will be helpful: