Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The number of days required to receive, sell and receive cash from the sale of inventory

An Operating Cycle (OC) refers to the days required for a business to receive inventory, sell the inventory, and collect cash from the sale of the inventory. This cycle plays a major role in determining the efficiency of a business.

The OC formula is as follows:

Where:

Using the Operating Cycle formula above:

Where the formula for Inventory Turnover is:

Where the formula for Receivables Turnover is:

Therefore, the detailed formula for OC is:

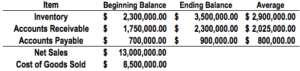

Calculating the OC with the data provided above:

Operating Cycle = 124.53 + 56.862 = 181.38 = 182 days

The OC offers an insight into a company’s operating efficiency. A shorter cycle is preferred and indicates a more efficient and successful business. A shorter cycle indicates that a company is able to recover its inventory investment quickly and possesses enough cash to meet obligations. If a company’s OC is long, it can create cash flow problems.

A company can reduce its OC in two ways:

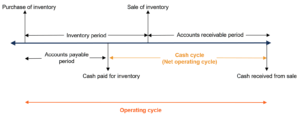

The operating cycle (OC) is often confused with the net operating cycle (NOC). The NOC is also known as the cash conversion cycle or cash cycle and indicates how long it takes a company to collect cash from the sale of inventory. To differentiate the two:

Additionally, the formula for the NOC is as follows:

The difference between the two formulas lies in NOC subtracting the accounts payable period. This is done because the NOC is only concerned with the time between paying for inventory to the cash collected from the sale of inventory.

The following image illustrates the difference between the cycles:

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Operating Cycle. To continue learning and advancing your career, these free CFI resources will be helpful: