Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

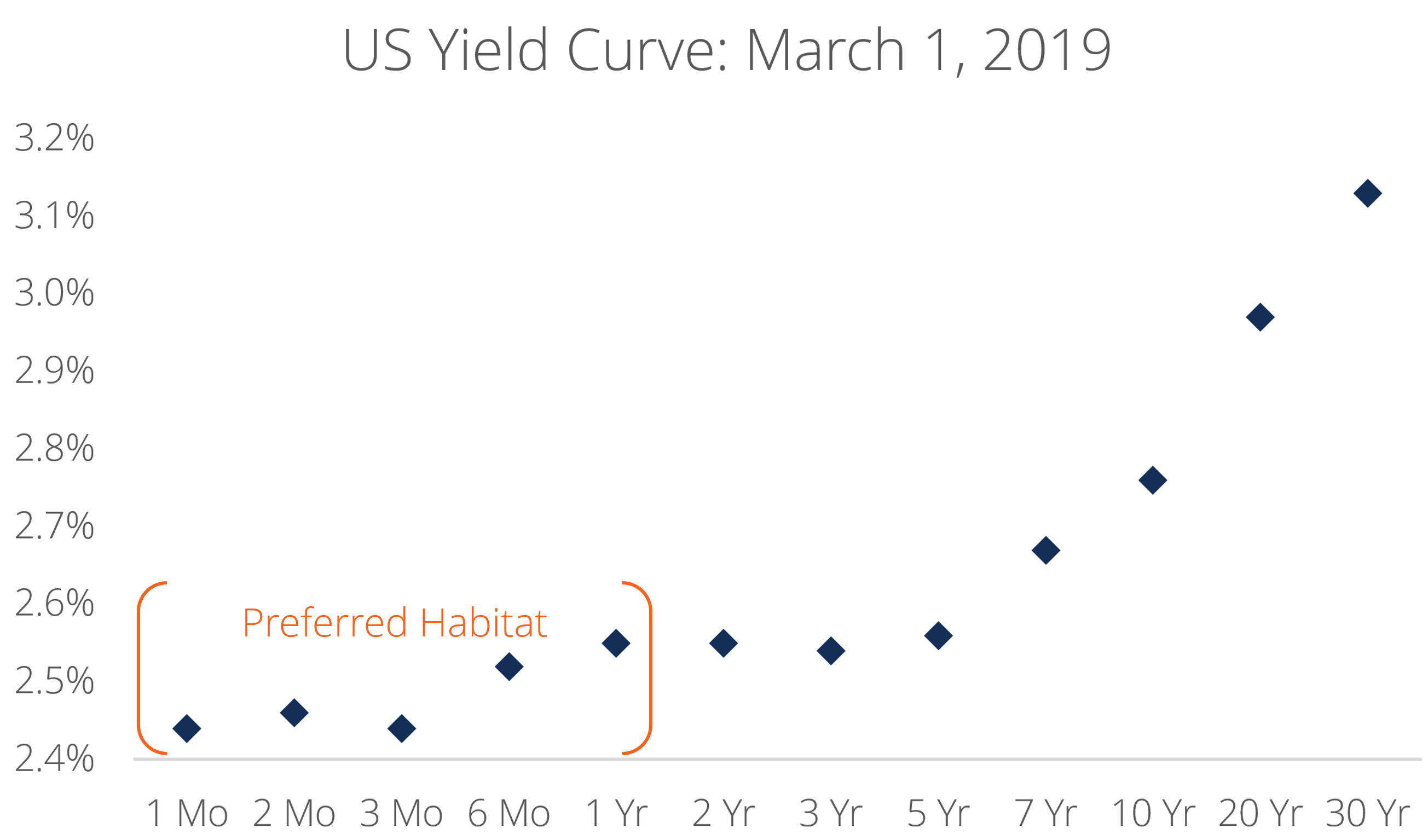

Bond market investors prefer certain terms to maturity.

The preferred habitat theory states that the market for bonds is ‘segmented’ by term structure and that bond market investors have preferences for these segments. According to the theory, bond market investors prefer to invest in a specific part or ‘habitat’ of the term structure.

The preferred habitat theory was introduced by Italian-American economist Franco Modigliani and the American economic historian Richard Sutch in their 1966 paper entitled “Innovations in Interest Rates Policy.” It is a combination of Culbertson’s segmented markets theory and Fisher’s expectations theory.

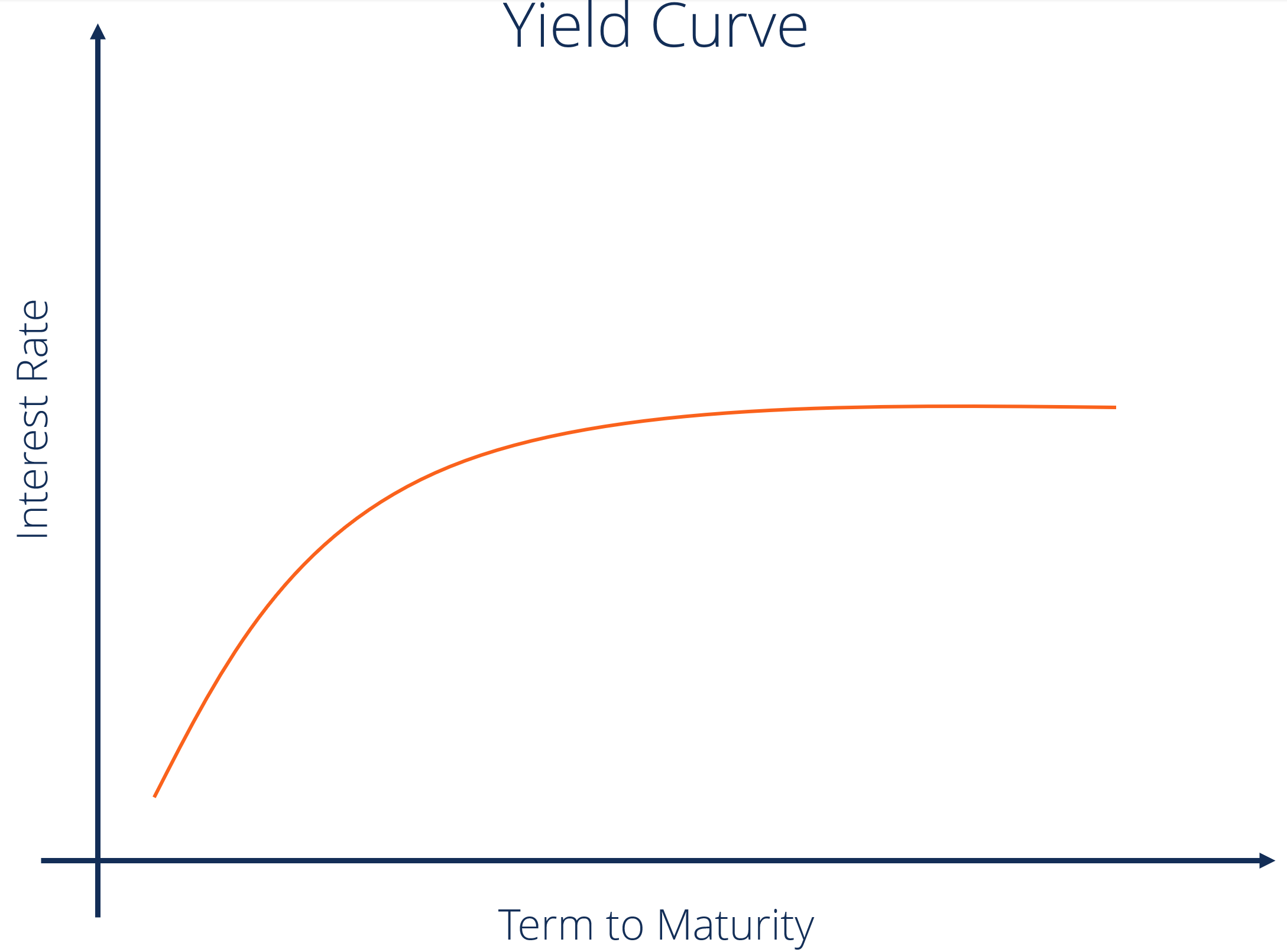

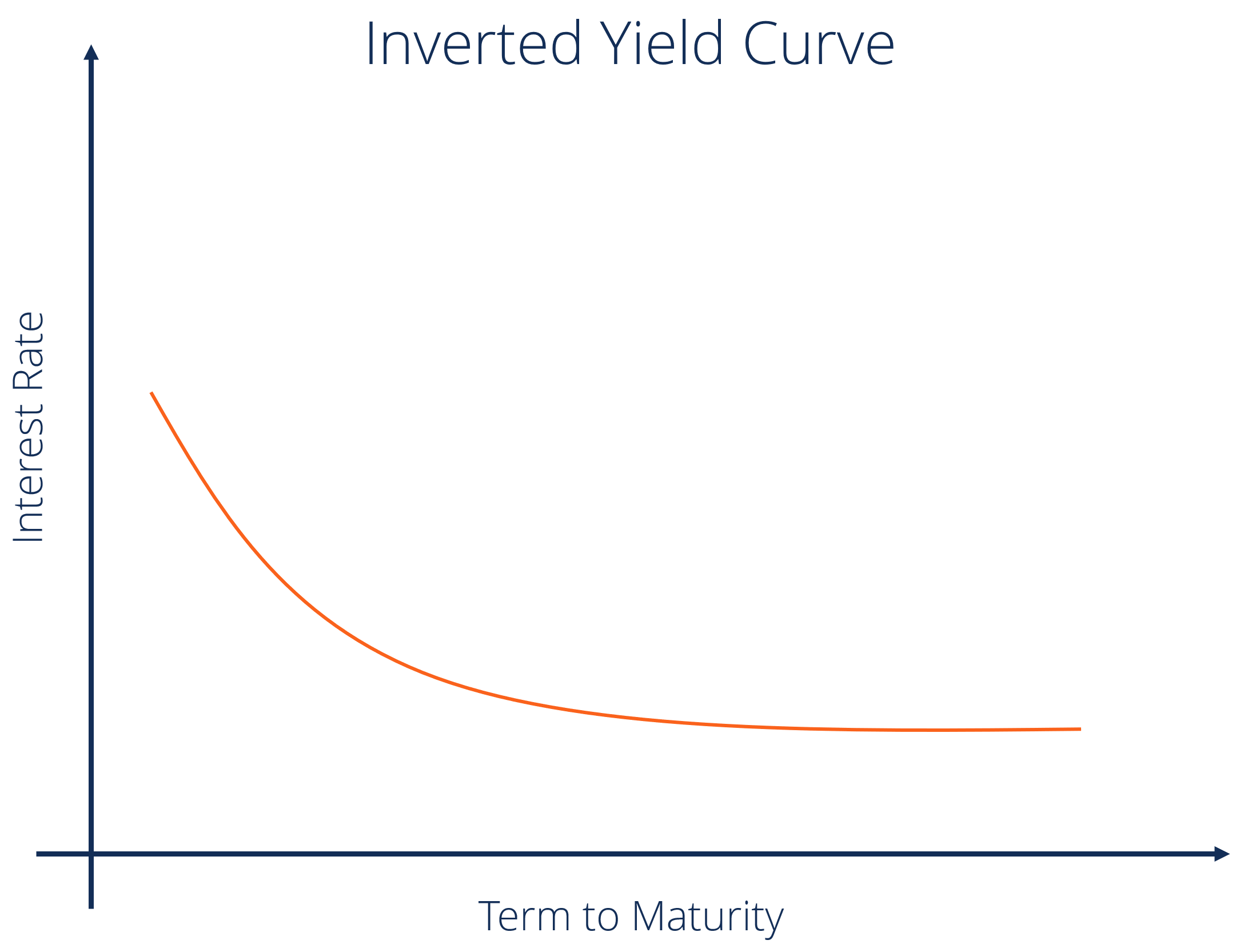

Term structure, also known as the yield curve when graphed, is the relationship between the interest rate of an asset (usually government bonds) and its time to maturity. Interest rate is measured on the vertical axis and time to maturity is measured on the horizontal axis.

Normally, interest rates and time to maturity are positively correlated. Therefore, interest rates rise with an increase in the time to maturity. It results in the term structure assuming a positive slope. The yield curve is often seen as a measure of confidence in the economy for the bond market.

The segmented markets theory states that the market for bonds is ‘segmented’ on the basis of the bonds’ term structure and that the ‘segmented’ markets operate more or less independently. Under the segmented markets theory, the return offered by a bond with a specific term structure is determined solely by the supply and demand for that bond and independent of the return offered by bonds with different term structures.

The expectations theory claims that the return on any long-term fixed income security must be equal to the expected return from a sequence of short-term fixed income securities. Therefore, any long-term fixed income security can be recreated using a sequence of short-term fixed income securities.

Learn more about fixed income securities with CFI’s Fixed Income Fundamentals Course!

The preferred habitat theory states that bond market investors demonstrate a preference for investment timeframes, and such preference dictates the slope of the term structure. Bond market investors require a premium to invest outside of their ‘preferred habitat’.

For example, an investor favoring short-term bonds to long-term bonds will only invest in long-term bonds if they yield a significantly higher return relative to short-term bonds. Conversely, an investor favoring long-term bonds to short-term bonds will only invest in short-term bonds if they yield a significantly higher return relative to long-term bonds.

Therefore, investor preferences that favor short-term bonds over long-term bonds would give rise to the standard upward sloping yield curve, whereas investor preferences that favor long-term bonds over short-term bonds would give rise to the inverted yield curve. When the preferred habitat theory was first propagated, an upward sloping yield curve was the norm. Thus, the short term was known as the preferred habitat for bond market investors.

CFI is the official provider of the Capital Markets & Securities Analyst (CMSA®) certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below!

Become a certified Financial Modeling and Valuation Analyst (FMVA)® by completing CFI’s online financial modeling classes!