Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

The process of raising debt in the capital markets for larger borrowers

Debt origination is the process that larger borrowers, such as corporations, financial institutions, and government entities, go through in order to raise debt. Generally speaking, the amount and frequency that the borrowers are looking to raise exceed the threshold for a traditional financial institution or group of financial institutions to undertake.

Companies may use debt proceeds to finance operations, internal projects, and acquisitions. Financial institutions may use debt to alter their exposures and match the duration of their assets with that of their liabilities. Governments may raise debt to finance projects or support the economy.

Debt is raised through the debt capital markets, utilizing investment banks as an intermediary to assist in raising capital. The investment banks act as a middleman to help distribute the debt raising to institutional investors, such as pension funds, hedge fund managers, and private banks.

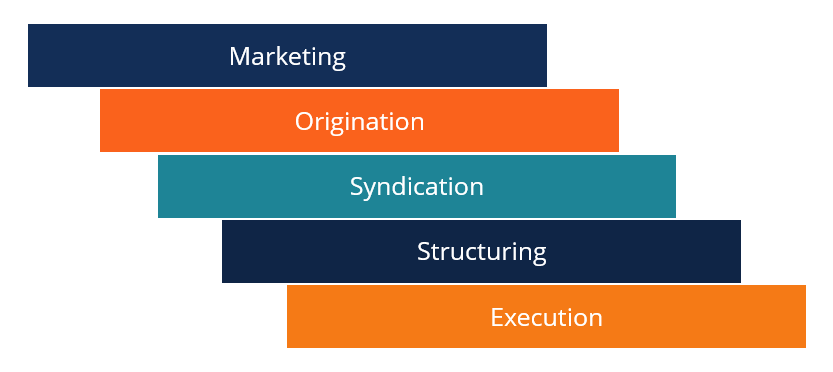

As mentioned, debt origination is the process that companies undertake in order to raise debt. In the context of capital markets, it is only one part of the process of raising debt.

The total process of raising debt includes:

The debt capital markets (DCM) are a function of the capital markets that are associated with debt securities. Investment banks employ DCM teams that are responsible for the origination, structuring, execution, and syndication of various debt-related products.

Debt-related products include interest-bearing instruments such as:

The securities may be issued by companies looking to raise capital to finance investments or finance an acquisition or other growth opportunities. The borrowers will raise from various types of investors, including those mentioned above and:

Investment banks are important intermediaries that carry out the debt origination process within the capital markets. Included in the process are three key factors:

On the investors’ side, originators must gauge several factors, including:

On the other side of the deal, the borrower’s or issuer’s needs must be considered, including:

The interest rate environment is very important to consider in the pricing of debt deals since the market interest rate serves as a benchmark for debt instruments. Pricing is generally done through the use of credit spreads relative to a reference government benchmark (such as the U.S. Treasury yield), which is considered a risk-free asset. Floating rate bonds are priced as a spread to a different reference benchmark (such as LIBOR or SOFR).

In return for their efforts, the investment bank charges an underwriting fee to help intermediate the debt raising. The fee depends on several factors, such as:

Furthermore, the investment bank may also make money from helping either the borrower or the investors structure the cash flows from the debt raising to suit their needs, called “hedges.” It is usually done with financial instruments called “derivatives,” which can either help reduce costs for the borrower or enhance the return for investors. Because of the opaque nature of pricing derivatives, the hedges are very lucrative for investment banks, often more so than the fees.

As an example, let’s say there is an industrial parts manufacturer that needs to raise debt to finance the refurbishing of one of their large manufacturing facilities. They require $300 million to do so and are looking to raise debt to finance the investment.

Given the large amount of the debt to be raised, the company’s primary bank is unable to provide the financing by itself and believes that even a small group of bank lenders (called a “club deal”) would not be able to take down the entire loan.

The company’s banker refers the manufacturer to their investment banking division colleagues, who can assist in meeting the funding needs of the manufacturer by raising debt from institutional investors from the public markets. However, the originator must be sensitive to the market and must structure the deal in a way that ensures it can be sold to investors.

The above is a highly simplified example. For larger debt issuances, there tend to be many more investors and a syndicate of investment banks that work together to originate the debt securities. Furthermore, there can be multiple types of securities issued, with some investors being higher on the capital structure (greater claim to assets in the event of a default).

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.