Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

A set of policies, procedures, and technologies that prevents money laundering

Anti-Money Laundering (AML) is a set of policies, procedures, and technologies that prevents money laundering. It is implemented within government systems and large financial institutions to monitor potentially fraudulent activity.

Money laundering refers to the process of taking illegally obtained money and making it appear to have come from a legitimate source. It involves putting the money through a series of commercial transactions in order to “clean” the money.

For example, money may be placed in a business and disguised as sales revenue in order to camouflage its origin. Money laundering is illegal in itself.

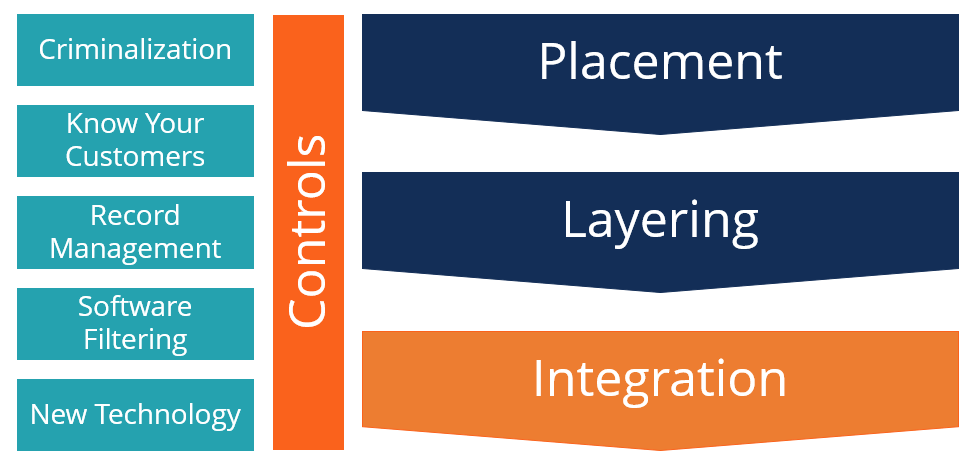

The figure below shows the three steps in money laundering and some of the controls that are used to prevent it. Money laundering is carried out through placement in a financial institution carrying out a series of transactions to disguise its original source (layering) and obtaining/using the cleaned money (integration).

Many governments, financial institutions, and businesses impose controls to prevent money laundering. The first is criminalization by the government. The United Nations Convention Against Transnational Organized Crime has set forth guidelines that help governments to prosecute individuals involved in money laundering schemes.

Financial institutions must also have “know your customer” policies in place to help prevent money laundering. This involves monitoring the activity of clients and understanding the types of transactions that should raise red flags. Financial institutions are required to report suspicious activity to a financial investigation unit.

Financial institutions and businesses also keep detailed records of transactions and implement software that can flag suspicious activity. Customer data can be classified based on varying levels of suspicion, and transactions denied if they meet certain criteria.

Many banks require deposits to remain in an account for a designated number of days (usually around five). This holding period helps manage risk associated with money being moved through banks to launder money.

The technology used to identify suspicious activity linked to money laundering continues to evolve and become more accurate. Technologies, such as AI and Big Data software, allow these systems to become more sophisticated.

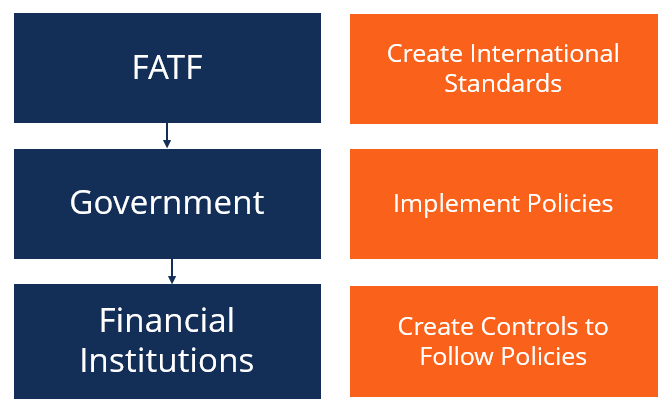

The first anti-money laundering structures came about with the Financial Action Task Force (FATF). It ensures that international standards are put in place to prevent money laundering.

Since the 2001 terrorist attacks, the FATF now also includes terrorist surveillance in an effort to mitigate terrorist financing. Recently, cryptocurrency has come under scrutiny, as it provides anonymity to its users. This has facilitated a lower-risk method for criminals to go about their transactions.

Financial institutions are held to high standards with regards to following procedures to identify money laundering. All bank employees are trained to some degree to identify and monitor suspicious customer activity. Larger financial institutions will also have dedicated departments to track fraud and money laundering.

Many of the institutions put in place a “know your client” measure, which can help flag suspicious transactions based on particular clients. Transactions and processes at financial institutions are recorded extensively so that law enforcement can trace the crimes back to the source.

While such institutions are legally obligated to follow anti-money laundering regulations as they relate to the country they operate in, not all agree with them. Implementing the policies are often costly and ineffective, and the net benefit of having them in place often comes into question.

HSBC went through a period of restructuring and cost-cutting, which caused them to decrease the size of their compliance department. As a result, many of the control systems to detect fraud and money laundering were weakened.

It was later found that HSBC had facilitated transactions that involved terrorist groups in the Middle East and drug cartels in Mexico. HSBC would eventually pay a fine of $1.9 billion, as regulators agreed that their control processes were inefficient in catching suspicious activity.

Thank you for reading CFI’s guide to Anti-Money Laundering. To keep learning and advancing your career, the following resources will be helpful: