Get In-Demand Finance Certifications

Valuation case studies can make or break a job interview, especially for highly competitive roles in investment banking, equity research, and private equity. Miscalculate enterprise value or apply the wrong multiple, and you risk looking unprepared in front of hiring managers. Let’s make sure that doesn’t happen.

This guide breaks down common valuation mistakes that candidates make in job interviews. You’ll learn how to avoid these pitfalls and demonstrate your analytical skills to hiring managers. By the end, you’ll be better prepared to tackle valuation questions in interviews — and land the job you want.

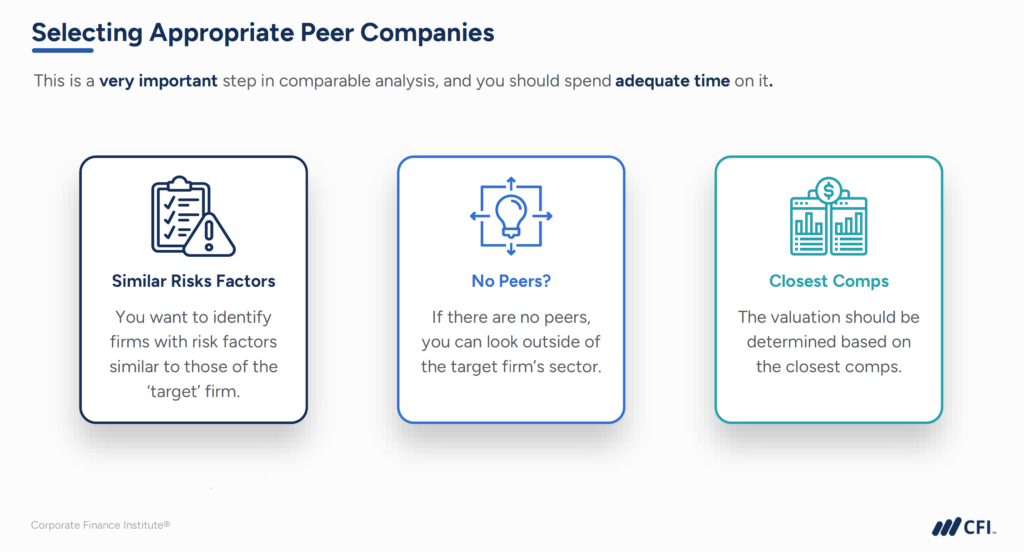

Comparable company analysis is a widely used valuation method in finance, but choosing the wrong peer group can distort valuation multiples. Sometimes candidates rush this step, failing to consider whether selected companies are truly comparable. This error can lead to overvaluing or undervaluing the target company.

Imagine you’re valuing TechCorp, a high-growth SaaS company with a 40% EBITDA margin and 30% annual revenue growth. You mistakenly compare it to ManufactureCo, a capital-intensive manufacturing firm with a 15% EBITDA margin and 5% revenue growth.

Since TechCorp operates in a completely different industry with higher margins and growth potential, using ManufactureCo as a comparable company results in a significant undervaluation of TechCorp.

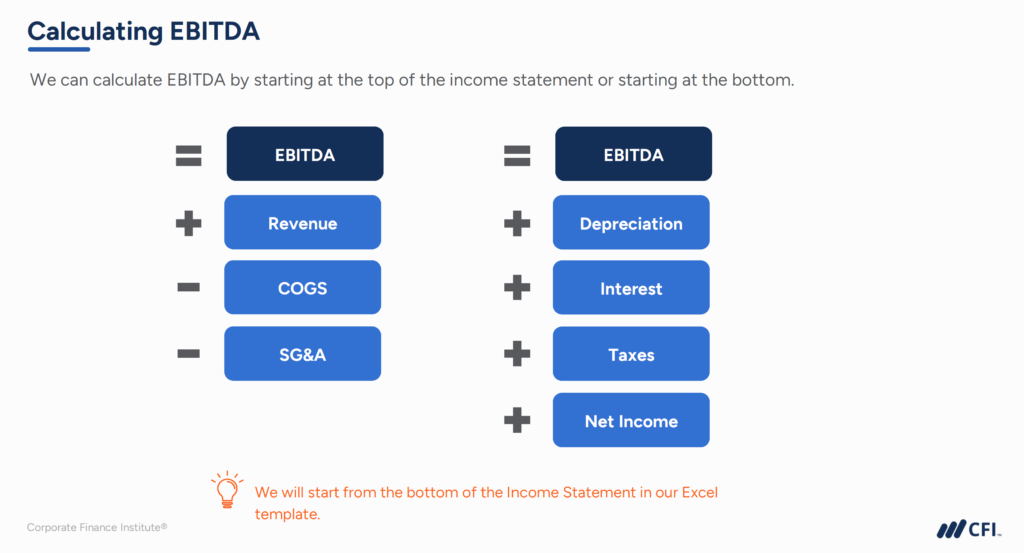

Even with the right peer group, your valuation is only as good as your inputs. The next challenge? Calculating EBITDA correctly to maintain consistency across companies.

Miscalculating or improperly adjusting EBITDA (Earnings Before Interest, Taxes, Depreciation & Amortization) skews valuation multiples like Enterprise Value to EBITDA (EV/EBITDA). Sometimes candidates make adjustment errors, leading to incorrect valuations.

Suppose RetailCorp reported an EBITDA of $100 million, but this figure includes a one-time $10 million legal expense and $5 million in gains from selling old equipment. If you don’t adjust for these non-recurring items, you understate RetailCorp’s true EBITDA, leading to a higher EV/EBITDA multiple than its industry peers.

Accurately calculating EBITDA is essential, but a complete valuation also requires determining EV.

Enterprise Value (EV) represents a company’s total value, including debt and equity. Miscalculations lead to inconsistent valuation multiples, making cross-company comparisons misleading.

A job candidate values AutoCorp using the following inputs:

However, they incorrectly calculate EV as: EV = Market Cap + Total Debt = $700 million.

The simple EV formula is EV = Market Capitalization + Market Value of Debt – Cash and Equivalents. The candidate failed to subtract Cash & Equivalents of $50 million, so their calculation overstates EV by $50 million.

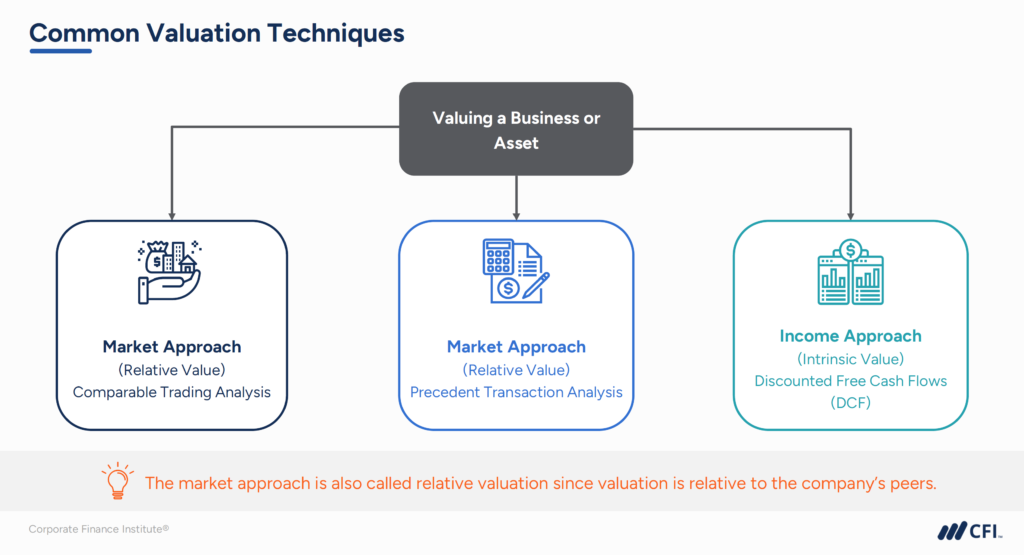

Accurate enterprise value calculations are essential, but even the best formulas can be misleading if you’re relying too heavily on a single valuation method.

Many candidates assume that valuation methods like comparable company analysis and precedent transactions are all they need to value a company. However, using only one valuation method often results in an incomplete picture of a company’s value.

A candidate values BioPharma Inc. using only EV/EBITDA but ignores DCF (Discounted Cash Flow). If BioPharma is a high-growth biotech firm with negative EBITDA, EV/EBITDA is meaningless — a DCF model would provide a better valuation.

Even with accurate valuations, you need to communicate your methodology and reasoning to stand out and get the job offer.

Even if you get the valuation calculations right, you still need to communicate your reasoning and assumptions clearly. This shows hiring managers how well you can work through valuation methodologies, justify your assumptions, and clearly communicate your thinking.

An interviewer asks, “Walk me through how you valued this company.”

A weak answer: “I used trading comps and got an EV of $650M.”

From this answer, the interviewer knows nothing about your reasoning, why you chose an EV approach, or what steps you followed to arrive at your answer.

Here’s an example of a strong answer: “I selected SaaS companies with similar revenue growth. I adjusted EBITDA to exclude one-time expenses, then applied an EV/EBITDA multiple of 12x, yielding an EV of $650M.”

This response follows a specific structure:

By structuring your answers clearly and anticipating follow-up questions, you’ll show hiring managers that you can think like a valuation analyst.

Mastering valuation techniques will help you impress hiring managers, communicate your insights clearly, and confidently tackle complex case studies.

By refining your approach to valuation, you’ll show employers that you can analyze financial data, justify assumptions, and deliver well-structured responses — skills that set top candidates apart.

Ready to master valuation and conquer job interviews? CFI’s Investment Banking & Private Equity Modeling Specialization equips you with financial modeling and valuation techniques used by top investment banks and private equity firms. Gain critical valuation skills to thrive in high-stakes finance roles.

Earn Your Investment Banking & Private Equity Modeling Specialization!

Paper LBO Example: A Tutorial for Private Equity Interviews

Learning Valuation: Essential Models, Skills, and Tools for Success