Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

The adjusted value of collateral assets being pledged as security for a loan

A borrowing base represents the adjusted value of eligible collateral that a lender will be extending credit against, before applying a discount factor (e.g. maximum LTV) that determines the credit limit.

Borrowers pledge many different categories of assets as security for a loan. But the book value of those assets doesn’t always tell the whole story; understanding the true collateral value of those assets requires thoughtful consideration.

Lenders make adjustments to an asset’s value based on a variety of factors, including its age, how active its secondary market is, and how easily transferable the title is.

In commercial lending, the term borrowing base is usually used in reference to working capital assets like accounts receivable (A/R) and inventory (INV), as opposed to property, plant and equipment (PP&E).

PP&E, being a non-current asset, serves as collateral for long term debt (like term loans and commercial mortgages). With a non-current asset, lenders often rely on an appraisal for a professional estimate of its value. The value of non-current assets tends to remain stable over time, and they depreciate in a predictable, mostly linear fashion.

But with working capital assets like A/R and INV, balances fluctuate daily, as does the balance on the client’s revolver (or operating line of credit). This constant fluctuation requires more regular monitoring by a lender, and so clients are often asked to provide a “borrowing base” certificate (sometimes called an attestation) either monthly or quarterly to confirm that the amount drawn against the revolver is supported by an appropriate borrowing base of A/R and INV.

The starting point to calculate a borrowing base is the book value of A/R and INV at a given period (usually the end of a month or a quarter). From there, lenders make adjustments to account for specific risks, informed by the firm’s credit policies.

Risks or characteristics that must be considered include the following:

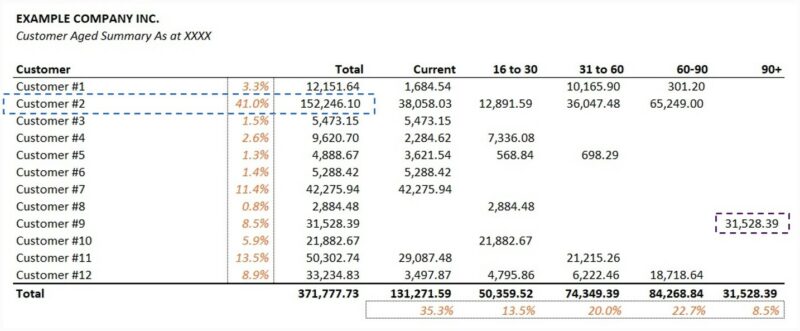

Concentration risk emerges when a client has a high proportion of A/R from a single customer (or a few particular customers). In Figure 1, EXAMPLE COMPANY INC. is the prospective borrower; the blue box shows that customer #2’s A/R represents 41% of the borrower’s total A/R.

If customer #2 went out of business and didn’t pay, or if they stopped doing business with our example company altogether, then that’s a sizable amount of cash owing and/or future business that could seriously impact the borrower’s financial health.

Some more conservative lenders might remove A/R values from their client’s borrowing base to try and capture and mitigate some of this concentration risk.

When a company sells on credit, management can’t control how quickly its customers settle those invoices. In general, many companies want to be paid within 30 days, but there are practical and strategic reasons why some customers will be granted longer terms.

In general, once accounts receivable get into the 60-90 day range, lenders may want to start asking questions. Beyond 90 days, the collection of the full account becomes much less likely.

In Figure 1, the purple box highlights $31,528 from customer #9, which has aged beyond 90 days. Most lenders would remove this amount from the client’s borrowing base.

Obsolescence is an important consideration when assessing inventory as collateral. Just because a borrower’s inventory balance is going up, it doesn’t mean that its value as collateral is increasing uniformly.

Sometimes management teams hold inventory on the company’s balance sheet even though it’s likely unsellable, instead of writing it down and taking a loss. Lenders should look for trends where a borrower’s inventory turns are decreasing (or its inventory days are increasing); this can be indicative of unsellable inventory that’s piling up in a warehouse somewhere.

Where practical, lenders should be doing site visits at a borrower’s places of business to ask questions about inventory stockpiles and any changes in trends.

Prudent lenders don’t just remove obsolete inventory from the borrowing base; they may proactively cap the amount of inventory they’re willing to use as collateral altogether in order to stay ahead of future obsolescence.

For example, a borrower may have $10MM in inventory on site, but the bank may have a policy that no more than $3MM of inventory be included in a client’s borrowing base (even though that only represents 30% of book value).

While a bank will cap borrowing to individual asset classes, as defined in the borrowing base definition within a loan agreement, it does not mean a borrower is able to finance the excluded amount with another lender.

A loan-to-value (LTV) is the proportion (or percentage) of an asset that a creditor is willing to lend against. A common example is 75% LTV for equipment; if the appraised value of that equipment comes in at $1MM, then 75% LTV represents a loan amount of $750,000.

Commercial banks also have LTV policies for working capital assets; common thresholds are 75% of “good” A/R and 50% of “good” INV (possibly subject to an inventory cap, as noted earlier).

“Good” A/R has been adjusted for concentration and aging, and “good” inventory has been adjusted for obsolescence, so borrowing base represents “value” when calculating LTV for a revolver and the variable credit limit up to and including the maximum credit limit.

Understanding the true value of collateral is paramount when structuring credit, since these assets serve as primary security for the lender under a general security agreement if a borrower triggers an event of default and it can’t be remedied or refinanced.

Extending a revolving line of credit to a commercial borrower without understanding and monitoring its borrowing base is like offering a commercial mortgage on a property without an appraisal.

As commercial borrowers grow and their revolving credit lines get larger, tighter controls are usually introduced to help monitor the value of working capital assets.

The most common means of control is margining. Margining is where a borrower is required to provide an aged A/R and INV listing at regular intervals, along with management’s borrowing base attestation (calculated monthly, quarterly, or annually). As the client’s borrowing base changes, the amount management is permitted to draw against the maximum credit limit on its revolver will vary accordingly.

Margining ensures that a borrower isn’t able to draw more funds against its operating line than there is security to backstop that exposure.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.