Get In-Demand Finance Certifications

A popular digital payment network built on its own blockchain, XRPL

Today, Ripple is one of the largest cryptocurrency platforms by market capitalization. However, Ripple Labs, the company behind Ripple and its native cryptocurrency token XRP, had been around since 2012 and was one of the earliest pioneers in the blockchain space, only behind Bitcoin and even before the Ethereum network.

The network was designed to be faster, cheaper, and more scalable than Bitcoin, and XRP is meant to facilitate financial transactions as a bridge currency.

Since the use case of the XRP digital token is very much tailored to the needs of banks and other financial institutions as an efficient global payment system, the blockchain ledger is centralized, and there is no mining of XRP.

Ripple was first founded back in 2004 as RipplePay in Vancouver, Canada by Ryan Fugger as a way of securely moving money around the world. In 2012, Fugger sold the company to Jed McCaleb, Arthur Britto, and David Schwartz, who transformed the company into a digital currency network and renamed it OpenCoin. McCaleb, who was the former founder of failed cryptocurrency exchange, Mt. Gox, left the company and forked Ripple into Stellar in 2013.

The company was renamed Ripple Labs in 2013 and, in 2015, was finally shortened to just “Ripple.”

The basis for Ripple, like any other cryptocurrency, lies in its blockchain that provides a permanent and unchangeable record of transactions. In Ripple’s case, the blockchain, or electronic ledger, that keeps track of transaction information such as accounts, balances, and transfers, is called XRPL (which stands for XRP Ledger).

The blockchain is secured cryptographically with key pairs, and transactions are only authorized by the holder of private keys. This is where the similarity with Bitcoin and other cryptocurrencies ends.

Ripple doesn’t use Proof-of-Work or Proof-of-Stake network consensus protocols. Instead, it has a quorum-based consensus method, which Ripple calls RPCA (Ripple Protocol Consensus Algorithm) to allow a majority of validators – servers specifically configured to participate actively in consensus – to agree a set of transactions should occur in a ledger entry.

That agreed-upon version of the ledger entry is validated and written to the blockchain, and its contents can never change.

While Ripple provides a default recommended list of ~35 validators based on past performance, each participating node in the network is free to choose its own list of validators. This list is called a Unique Node List, or UNL, that is specific to each node.

Each node should carefully choose validators from among the 150+ present validators based on who they believe will behave honestly most of the time and not collude with other validators to break the rules.

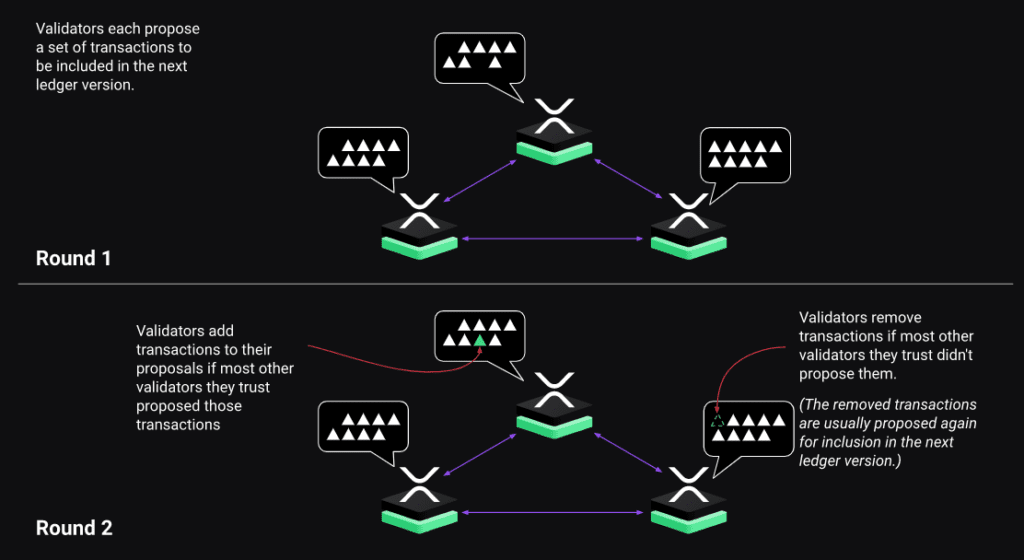

Each validator proposes what they deem to be the correct block containing new transactions. They compare blocks, or ledger entries, every 3 to 6 seconds, and if an 80% majority of validator nodes agree on the transactions and order, a consensus is achieved, and the block is added to the XRPL and forms the starting point of the next block.

However, if 80% of validators don’t agree on what transactions should be written to the ledger, each validator modifies their proposals to more closely match the other validators they trust on their UNLs. This may repeat for several rounds until a consensus is reached.

Source: XRPL.org

As long as fewer than 20% of trusted validators are faulty, consensus can continue unimpeded; and confirming an invalid transaction would require over 80% of trusted validators to collude. If more than 20% but less than 80% of trusted validators are faulty, the network stops making progress

You may hear some say that Ripple is not a “real cryptocurrency,” but that’s not exactly correct. Even though Ripple is somewhat different, it does fit the definition of a cryptocurrency, which is a digital token built upon a decentralized ledger that allows for the peer-to-peer transfer of value over the internet.

Let’s look at some differences of Ripple:

Some detractors will say that Ripple controls their blockchain because it presently controls six of the validators on its default UNL, which is used to achieve the quorum-based consensus.

However, in reality, individual nodes can pick whoever they wish for their own UNLs.

Unlike Bitcoin, Ripple does not pay any rewards for adding new blocks to the blockchain. They believe that incentives tend to warp validators’ behavior, but instead, validators’ incentive should be to preserve the stability, reliability, and integrity of the Ripple network.

This has also led to fewer validators, as there isn’t a financial incentive to run a Ripple validator unless you are an active user of the ecosystem.

XRP is neither mined nor minted, but rather 100 billion XRP was pre-mined at the launch. 80 billion of the tokens went to the Ripple Labs foundation, which oversees the Ripple network and sells XRP periodically at market prices to fund the ecosystem (Presently, 44.3 billion XRP remains in the so-called Ripple Escrow).

The remaining 20 billion was kept by the three co-founders of the network. Although each transaction on the XRPL burns a little bit of XRP, supply is hard to forecast because of regular sales by the Foundation (currently, 1 billion XRP a month is released) and unscheduled and unannounced sales from the co-founders.

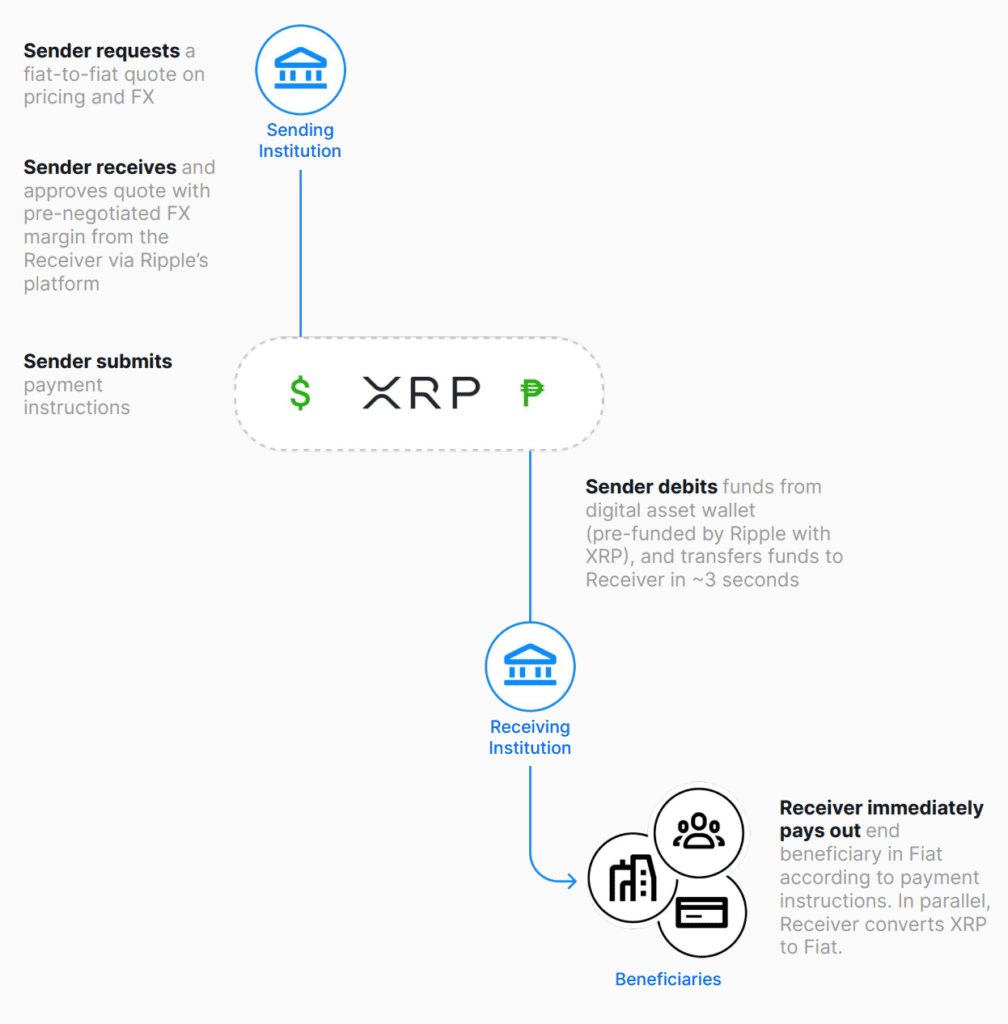

One interesting difference for Ripple is that the customer base that uses it network, called RippleNet, is less individual consumers, but rather financial institutions. As a matter of fact, RippleNet’s customers include hundreds of banks, from small institutions to large multinational organizations like Bank of America and Santander.

That’s because Ripple touts its RippleNet as a fast, cheap, and reliable global payments network, which doesn’t require users, such as banks and other money transfer companies, to “pre-fund” accounts with cash like they would with a traditional wire transfer.

Since there is no mining involved in Ripple, there isn’t the same environmental impact as a Proof-of-Work system like Bitcoin. Also, the transaction cost of XRP is extremely low. The current minimum transaction cost required by the network for a standard transaction is 0.00001 XRP (or 10 ‘drops’, the smallest unit of XRP).

Additionally, whereas it takes 10 minutes for a block to be solved in Bitcoin and up to 60 minutes for probabilistic finality, Ripple takes 3 to 6 seconds for transactions to be sorted, agreed, and added to the blockchain, even for payments internationally.

It also is meant to be much more scalable, with 1,500 transactions per second, compared with Bitcoin’s 7-10 transactions per second. The goal is to eventually match Visa’s scale of 65,000 transactions per second.

Unlike other digital currency protocols, the XRP Ledger allows users to denominate their transactions with any currency they prefer, including fiat currencies, digital currencies, and other forms of value, in addition to XRP.

This is very important for foreign exchange transactions, as someone looking to move money across the world won’t need to conduct foreign exchange but will instead send and receive in local currency on either side of the transaction. Ripple also offers autobridging, which finds the best exchange rate should the parties want to exchange currencies.

This also means that money can reach markets that normally might take longer or cost a lot more to reach.

Source: XRPL.org

Since tokens other than XRP can be created on the XRP Ledger, called IOUS, there can be digital assets that use the XRP Ledger, such as stablecoins, NFTs, and even Central Bank Digital Coins.

Although the XRP cryptocurrency is decentralized, it’s still tied to a private company in Ripple, and Ripple makes money by selling XRP, payment fees, profits from investments, as well as interest fees on loans.

As Ripple sells XRP from its escrow accounts, they realize a profit that is paid to the Ripple Foundation. Additionally, the transaction fees are paid to Ripple, so although the fee is only 10 drops, since there is no incentive paid out to validators, the fee goes to Ripple.

They also came out with a loan product in 2020 to access ODL (On-Demand Liquidity) that can be collateralized with XRP.

Lastly, Ripple has been busy acquiring other companies, such as Tranglo, most recently, an Asian global payments company.

As a private company, Ripple does not need to disclose any financials, so revenues are not known. Based on some estimates, the company was worth as much as USD10 billion in December 2019.

In 2015, Ripple was fined[1] by the United States Department of Justice for violating regulations under the Bank Secrecy Act and not registering with their Financial Crimes Enforcement Network.

The US Securities and Exchange Commission, a government regulator, sued[2] Ripple Laps and its founders in December 2020 as it sees XRP as an unregistered securities offering since the proceeds of the sale were used by the company and founders to fund operations, resembling a stock sale. The lawsuit is still being battled in court between the regulator and Ripple, and the outcome is far from certain.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Ripple. To keep advancing your career, the additional CFI resources below will be useful:

See all Cryptocurrency resources