Get Certified for

Business Intelligence (BIDA®)

Develop analytical superpowers by learning how to use programming and data analytics tools such as VBA, Python, Tableau, Power BI, Power Query, and more.

A measure of the deviation of a random variable’s given distribution from the normal distribution

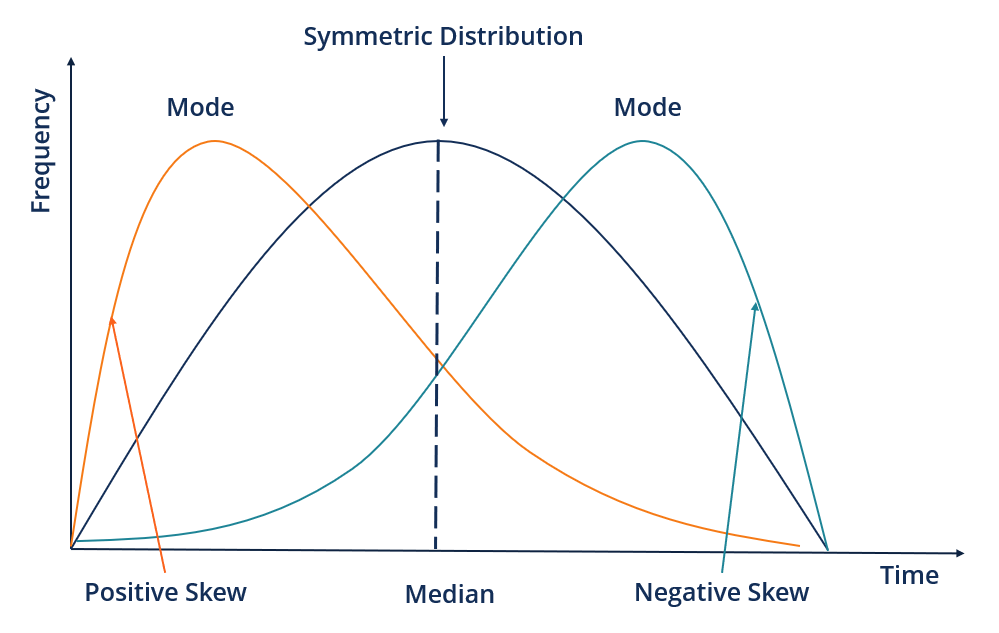

Skewness is a measure of asymmetry or distortion of symmetric distribution. It measures the deviation of the given distribution of a random variable from a symmetric distribution, such as normal distribution. A normal distribution is without any skewness, as it is symmetrical on both sides. Hence, a curve is regarded as skewed if it is shifted towards the right or the left.

If the given distribution is shifted to the left and with its tail on the right side, it is a positively skewed distribution. It is also called the right-skewed distribution. A tail is referred to as the tapering of the curve differently from the data points on the other side.

As the name suggests, a positively skewed distribution assumes a skewness value of more than zero. Since the skewness of the given distribution is on the right, the mean value is greater than the median and moves towards the right, and the mode occurs at the highest frequency of the distribution.

If the given distribution is shifted to the right and with its tail on the left side, it is a negatively skewed distribution. It is also called a left-skewed distribution. The skewness value of any distribution showing a negative skew is always less than zero. The skewness of the given distribution is on the left; hence, the mean value is less than the median and moves towards the left, and the mode occurs at the highest frequency of the distribution.

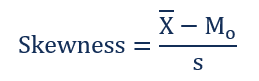

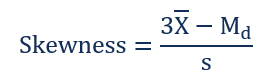

Skewness can be measured using several methods; however, Pearson mode skewness and Pearson median skewness are the two frequently used methods. The Pearson mode skewness is used when a strong mode is exhibited by the sample data. If the data includes multiple modes or a weak mode, Pearson’s median skewness is used.

The formula for Pearson mode skewness:

Where:

The formula for Person median skewness:

Where:

Additional Resources

Thank you for reading CFI’s guide to Skewness. To keep advancing your career, the additional CFI resources below will be useful: