Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A dividend that is paid out ahead of a change in the way the dividends are treated

An accelerated dividend is a dividend that is paid out ahead of a change in the way the dividends are treated, such as a change in the tax rate of dividends. The dividend payments are made early in order to protect shareholders and mitigate the negative impact that a change in dividend policy brings about.

Consider the following example:

On April 6, 2016, the UK Treasury introduced a new rate of tax on dividends. Under the new policy, the first £5,000 of dividend income is not taxed. Above that amount, the basic taxpayer needs to pay 7.5%, the high-rate taxpayer needs to pay 32.5%, and the additional rate taxpayer needs to pay 38.1% in tax. The new tax structure raises the marginal tax rate by around 6% for most shareholders.

The above example is a case where company owners would consider paying out an accelerated dividend. (Paying taxes before April 6 would save shareholders a lot of money in tax payments).

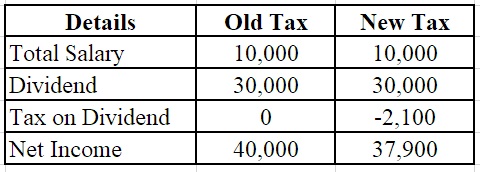

Sam’s distributable reserve after subtracting salary and corporate tax is £30,000. He takes a salary of £10,000 a year and a personal allowance of £7,000.

New tax dividend calculation:

(10,000 + 30,000) – 7,000 = 33,000 – 5,000 = 28,000 * 0.075 = £2,100

In Sam’s case, an accelerated dividend is not the best option. One reason is that an early dividend payment could put him in the higher tax bracket. Alternatively, a tax self-assessment might be required due to the accelerated dividend, and Sam might end up paying a tax that is greater than £2,000.

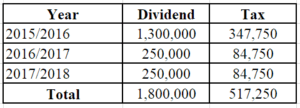

Zack, a large business owner, draws out £600,000 as dividends. The distributable reserves are £1,300,000.

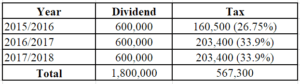

Zack’s total taxes due are £567,300. If Zack chose to pay the entire distributable reserve of £1,300,000 as a dividend reserve before April 2016, below is what the tax breakup will look like:

While such large tax savings are unlikely to occur in the real world, by paying the total dividend reserve of 1,300,000 before April 6, 2016, Zack can save £50,050 in total tax payments (567,300 – 517,250).

In the case of a big business where a large dividend is paid out, an accelerated dividend payment to help mitigate the effects of changes in the treatment of dividends can prove to be beneficial.

One way to avoid the tax liabilities caused by paying an accelerated dividend is to make pension contributions. Many people find pension contributions an attractive alternative when there are high tax rates on dividends because it allows an individual to divert a large part of their income into a tax-free account. The taxes imposed on pension income when it is paid out will be based on the old tax rates.

Another option to avoid high tax rates is a gift aid payment. Gift payments help extend the income tax basic rate band for individuals. The only stipulation is that the payments need to be made in the year before the dividend is declared. Since the new tax rate would take effect in April 2016, all gift payments should have been made before the due date in order to gain tax relief and extend the basic rate band.

Although an accelerated dividend seems advantageous for some as it helps avoid large tax payments on dividends, it is not always the best option. As seen in the example with the small business owner, declaring an accelerated dividend may actually lead to higher tax payments in the future due to the self-assessment tax. The size of the business and its financial standing must be taken into consideration before paying out an accelerated dividend.

CFI offers the Capital Markets & Securities Analyst (CMSA®) certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following CFI resources will be helpful: