Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

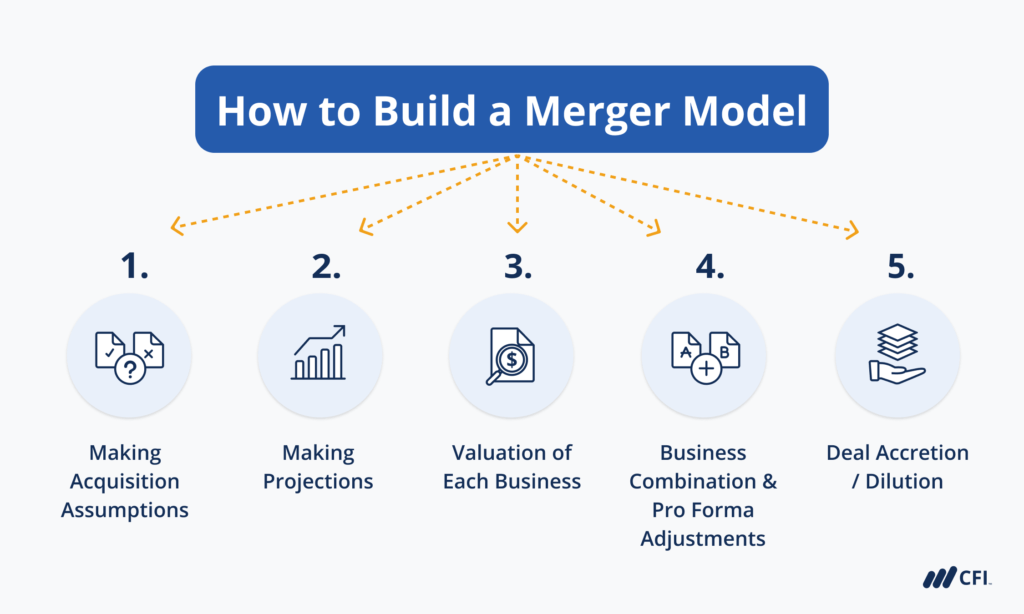

The key steps to building a merger model

A merger model is an analysis representing the combination of two companies that come together through an M&A process. A merger is the “combination” of two companies, under a mutual agreement, to form a consolidated entity. An acquisition occurs when one company proposes to offer cash or its shares to acquire another company.

In both cases, both companies merge to form one company, subject to the approval of the shareholders of both companies. Below are the steps of how to build a merger model.

To learn more, check out our Merger Modeling Course.

The main steps for building a merger model are:

Each of these steps will be explored in more detail below.

Where the buyer’s stock is undervalued, the buyer may decide to use cash instead of equity consideration since they would be forced to give up a significant number of shares to the target company.

In contrast, the target company may want to receive equity because it might be more valuable than cash. Finding a consideration agreeable to both parties is a crucial part of striking a deal.

In contrast, the target company may want to receive equity because it might be perceived as more valuable than cash. Finding a consideration agreeable to both parties is a crucial part of striking a deal.

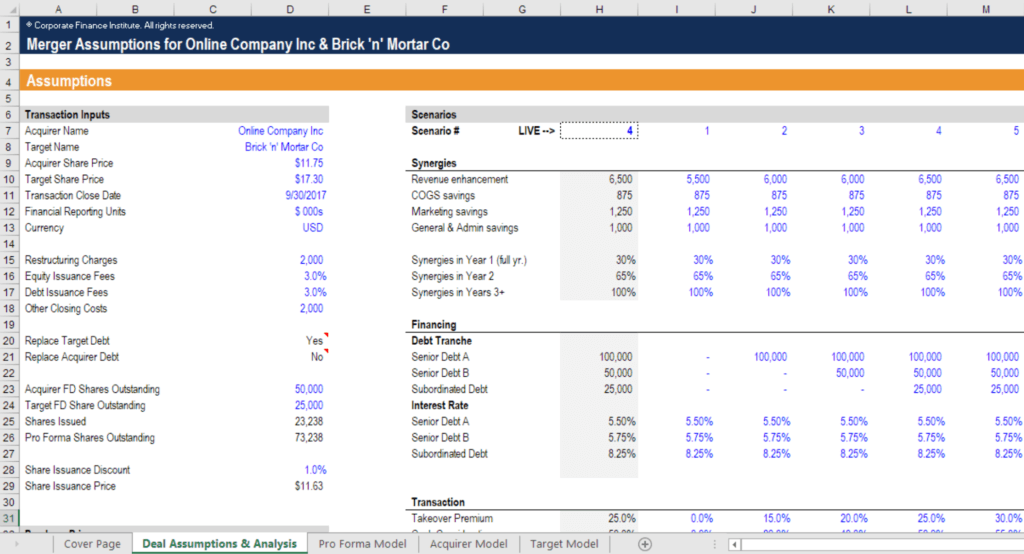

Key assumptions include:

Screenshot from CFI’s M&A Modeling Course.

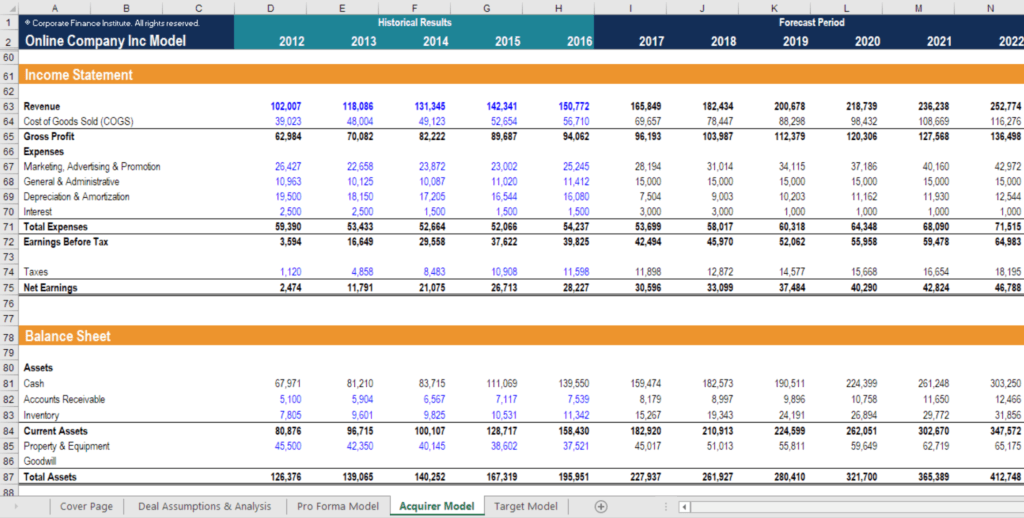

Making projections in a merger model is the same as in a regular DCF model or any other type of financial model. In order to forecast, an analyst will make assumptions about revenue growth, margins, fixed costs, variable costs, capital structure, capital expenditures, and all other accounts on the company’s financial statements.

This process is known as building a 3-statement model and requires linking the income statement, balance sheet, and cash flow statement. Build this section just as you do with any other model, and repeat it twice: once for the target and once for the acquirer.

To learn more, launch CFI’s online financial modeling courses now!

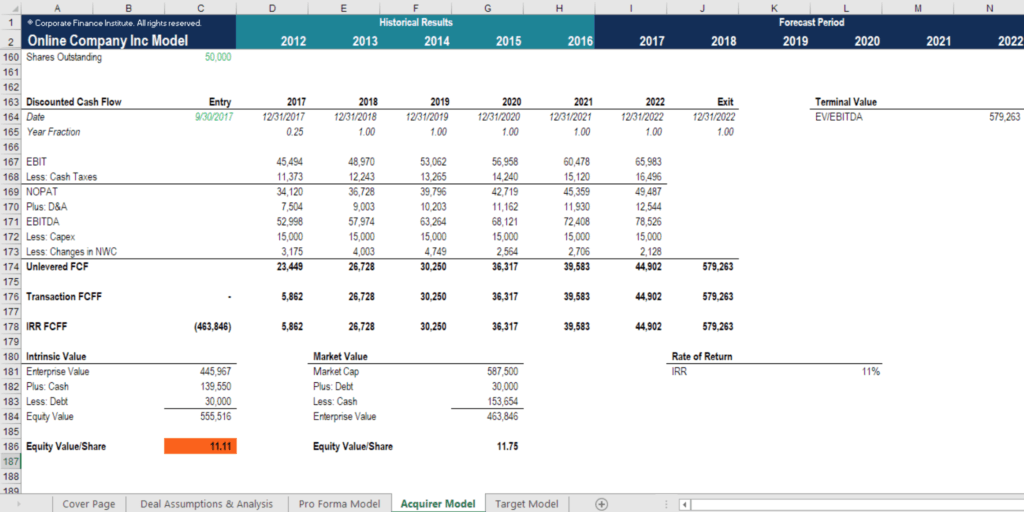

Step 3 of how to build a merger model is a DCF analysis of each business. Once the forecast is complete, it’s time to perform a valuation of each business. The valuation will be based on a discounted cash flow (DCF) model, which will also be compared and contrasted with comparable company analysis and precedent transactions.

There will be many assumptions involved in this step, and it is probably the most subjective. Therefore, this is an area where a highly skilled financial analyst can really make a difference by producing extremely accurate and reliable numbers.

The steps in performing the valuation include:

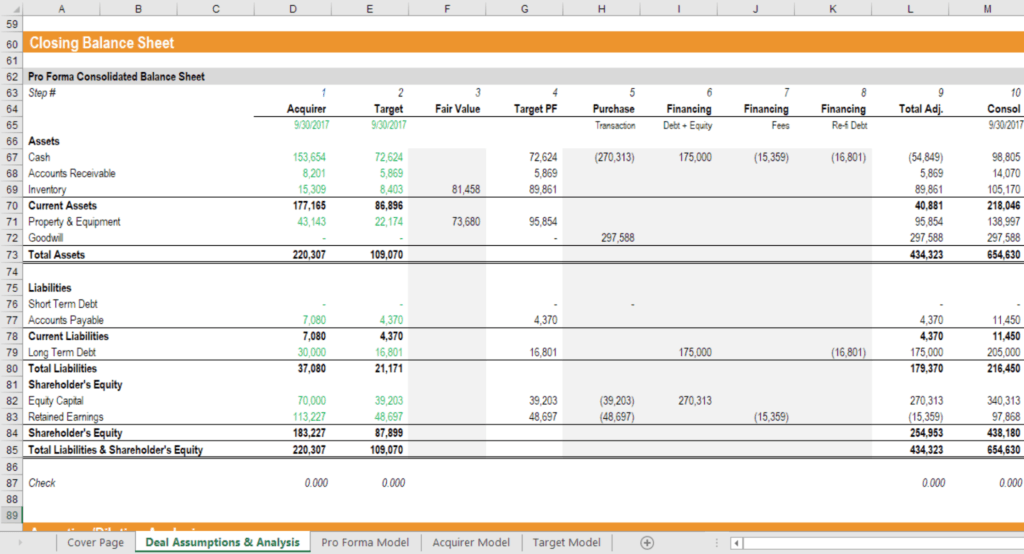

Screenshot from CFI’s M&A Financial Modeling Course.

When Company A acquires Company B, the balance sheet items of Company B will be added to the balance sheet of Company A. Combining the two companies’ financials will require several accounting adjustments, such as determining the value of goodwill, value of stock shares, and options, and cash equivalents. This section is also where various types of synergies come into play.

Key assumptions include:

An important step in building the merger model is determining the goodwill resulting from the acquisition of the assets of the target company. Goodwill arises when the buyer acquires the target for a price that is greater than the Fair Market Value of Net Tangible Assets on the seller’s balance sheet. If the book value of the acquired entity is lower than what the acquirer paid, then an impairment charge will arise. As a result, the acquired net assets will be written down in value equal to the consideration paid.

Read more: Merger Factors and Complexity

Learn more in CFI’s Mergers and Acquisitions Course.

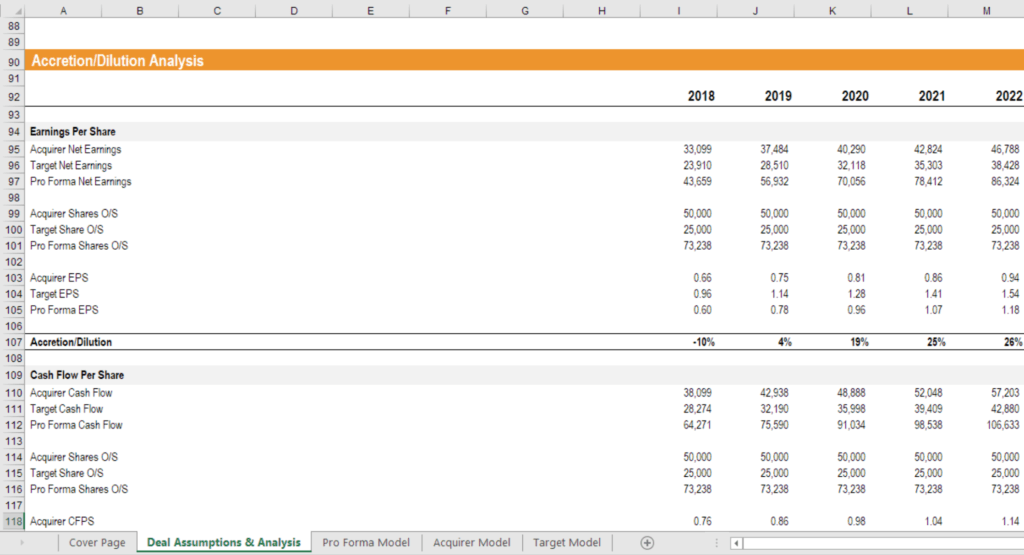

The purpose of accretion/dilution analysis is to determine the effect of the acquisition on the buyer’s Pro Forma Earnings per Share (EPS). A transaction is deemed accretive if the buyer’s EPS increases after acquiring the target company. Conversely, a transaction is viewed as dilutive if the buyer’s EPS declines as a result of the merger. The buyer should estimate the effect of the target’s financial performance on the company’s EPS before closing a deal.

Key assumptions include:

Image from CFI’s Merger Modeling Course.

As you see in the example above, this deal is dilutive for the acquirer, meaning their Earnings Per Share is lower, as a result of doing the transaction, than their Earnings Per Share were before the deal. Such a situation – in isolation – would argue against the acquisition being a good deal for the acquirer but, of course, many other considerations factor into the final decision on whether or not to pursue a merger deal.

Read more: Accretion Dilution Analysis

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Building A Merger Model. To continue learning and advancing your career, these additional free CFI resources will be helpful: