Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

When companies merge or acquire others, they need to pay for the transaction somehow. This payment method is called the form of consideration. Think of this term as what the target company’s shareholders receive in exchange for selling their ownership to an acquirer.

Forms of consideration represent one of the most critical aspects of any M&A transaction structure. Will the acquiring company pay in cash, hand over shares of its own stock, or use some combination of both? This seemingly straightforward choice dramatically impacts everything from financing requirements to how the deal’s value appears in an M&A model.

Understanding forms of consideration is crucial to properly assess transaction economics and perform accurate accretion/dilution analysis. This guide explores the different forms of consideration and how they influence the way an M&A transaction is evaluated.

M&A transactions typically utilize three main forms of consideration: cash, stock, or a combination of cash and stock. Each option creates distinct financial implications that analysts must carefully model and interpret.

Cash consideration is the portion of the purchase price given to the target company’s shareholders in cash. It’s straightforward but requires the acquirer to have sufficient funds available — either from existing cash reserves, new debt, or both.

Stock consideration refers to the portion of the purchase price paid in shares of the acquiring company. This approach doesn’t require immediate cash but dilutes existing shareholders’ ownership as new shares are issued to target shareholders.

Mixed consideration combines both cash and stock in varying proportions. This approach gives acquirers flexibility to balance various objectives. In practice, many real-world transactions use this structure, with common splits like 50/50 cash and stock or other proportions depending on the specific circumstances.

When analyzing forms of consideration, it’s critical to examine not just which option is chosen, but also the percentage split between cash and stock in mixed approaches. This seemingly technical detail profoundly influences how the transaction impacts key financial metrics.

Before diving into the modeling process, analysts need to understand two key concepts that directly affect consideration calculations:

The share exchange ratio is used when there is stock consideration. The exchange ratio is defined as the offer price for target shares divided by the acquirer’s share price. This ratio determines how many acquirer shares each target shareholder receives.

Takeover premium is the difference between the market price of a company and the actual price paid to acquire it, expressed as a percentage. This premium incentivizes target shareholders to approve the deal but increases the total consideration required.

Modeling different forms of consideration starts with understanding the purchase price and how it’ll be funded. Whether it’s a 100% stock deal, all cash, or a combination of both, each scenario demands careful calculation.

For cash portions, you’ll need to determine exactly how much money is required. This calculation is straightforward:

This amount then feeds into your sources and uses of cash schedule to ensure sufficient funding.

For stock components, the math gets more interesting.

This figure directly impacts the pro forma shares outstanding, which becomes crucial for per-share metrics later.

Remember that consideration structure significantly impacts how the transaction is financed, affecting the closing balance sheet and all subsequent financial projections.

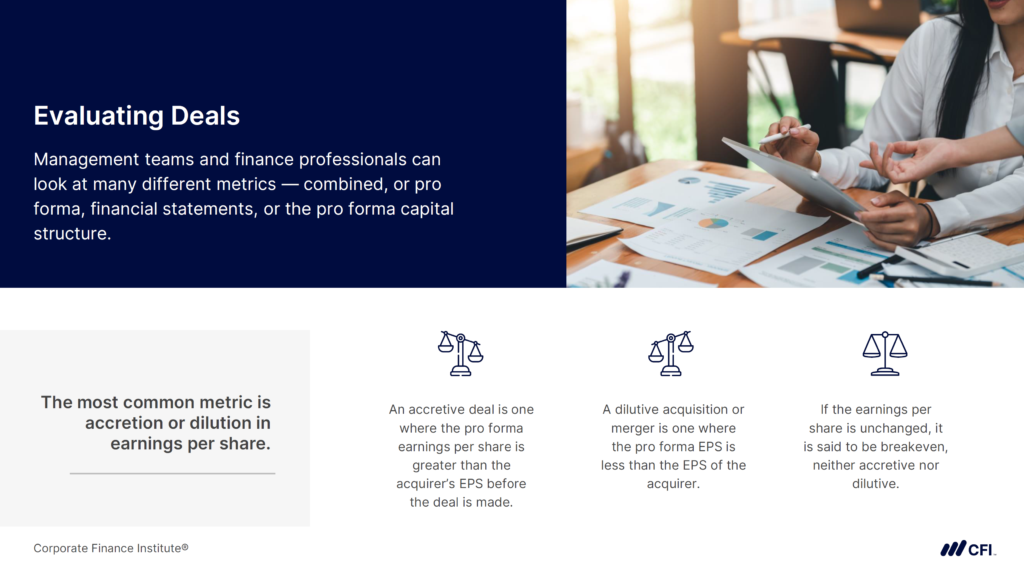

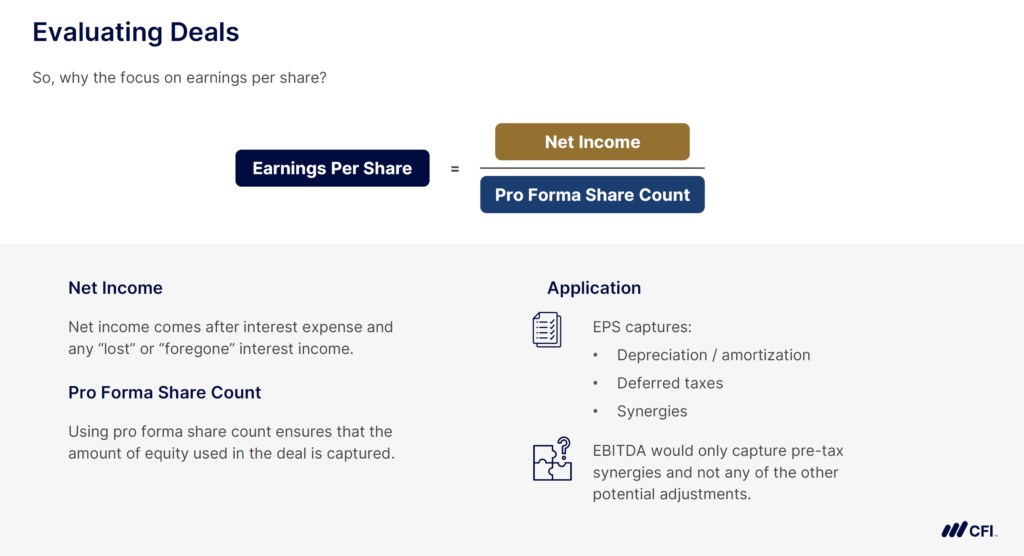

One of the most counterintuitive aspects of M&A analysis is how different forms of consideration affect accretion and dilution metrics. This phenomenon often surprises even experienced financial analysts.

Accretion occurs when the acquirer’s earnings per share (EPS) increases after a transaction. Dilution happens when EPS decreases. While these metrics seem straightforward, the form of consideration dramatically influences them — sometimes in misleading ways.

Here’s the surprising reality: all-cash deals typically appear more accretive than all-stock deals, even when paying identical prices for the same target.

In a stock deal, the acquiring company issues new shares, which increases the denominator when calculating EPS. In contrast, with cash deals (often funded by debt), principal debt repayments don’t flow through the income statement.

Testing different consideration scenarios in your model might reveal a surprising insight. A transaction could swing from 10% dilutive to highly accretive simply by adjusting the cash-stock ratio — without changing the purchase price or any synergy assumptions.

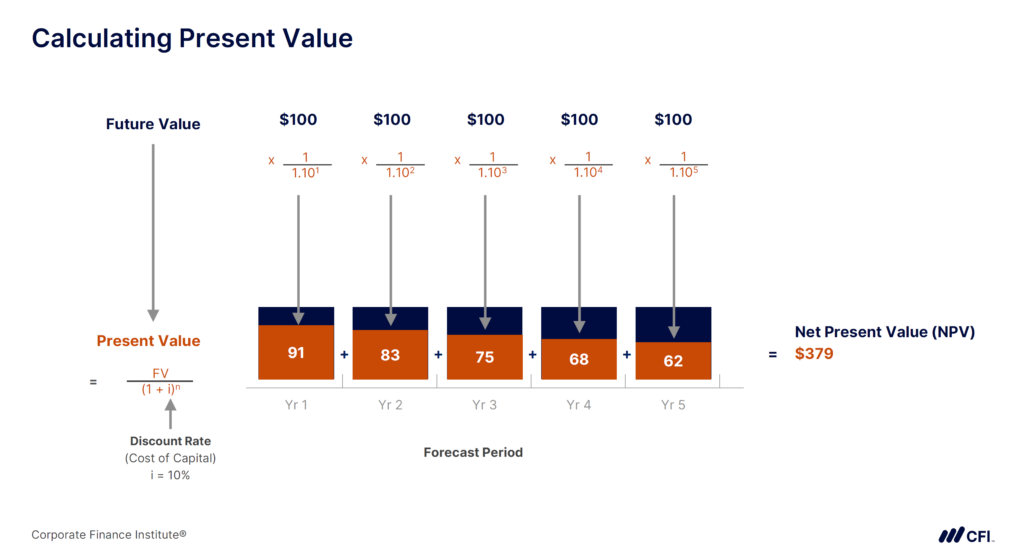

Since accretion/dilution metrics can be misleading, financial analysts must look beyond EPS impacts to truly understand a transaction’s economic merit. This requires examining how different forms of consideration affect intrinsic value per share, or the price a rational investor is willing to pay per share, given the level of risk.

When analyzing various consideration structures, focus on the net present value (NPV) impact to shareholders. NPV represents the current value of expected future cash flows minus the investment’s costs (cash outflows).

A helpful approach is comparing the acquirer’s intrinsic value per share before the transaction to the pro forma intrinsic value afterward.

A transaction with positive NPV impact should increase intrinsic value per share, regardless of whether it’s funded with cash or stock. A negative NPV indicates the transaction could destroy value. Unlike EPS metrics, this NPV comparison better reflects true value creation.

Remember that cash-heavy deals typically increase leverage, while stock-heavy deals dilute ownership. Both have long-term implications that simple accretion/dilution analysis might miss.

Want hands-on practice calculating intrinsic value? Download our free intrinsic value template, which demonstrates two different methods to determine the intrinsic value of businesses.

When analyzing M&A transactions, forms of consideration often reveal more about financial engineering than economic fundamentals. As a financial analyst, your ability to look beyond superficial metrics sets you apart in this field.

Instead of focusing solely on whether a deal is “accretive” or “dilutive,” ask critical questions: Does the combined entity create genuine economic value regardless of financing? How much apparent accretion stems from consideration structure rather than actual synergies? Are EPS impacts masking an overpriced deal?

Understanding forms of consideration is a critical differentiator that can accelerate your career progression. Mastering these nuanced concepts positions you for strategic roles where you’re shaping transactions, not just processing them.

If you’re looking to sharpen your M&A modeling skills and apply this kind of analysis with confidence, specialized training can help you get there.

Ready to level up your M&A modeling expertise? CFI’s Investment Banking & Private Equity Modeling Specialization equips you with job-ready skills in advanced financial modeling (DCF, LBO, and M&A), valuation, forecasting, and transactional decision-making. Learn the techniques used by finance professionals at JPMorgan, BlackRock, KKR, and more!

Sources and Uses of Cash Schedule

M&A Financing: Cash, Debt, or Equity?