Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

Bonds with no maturity date

Perpetual bonds – which are also referred to as perpetuals or just “perps” for short – are bonds with no maturity date. They pay interest to investors in the form of coupon payments, just as with most bonds, but the bond’s principal amount does not come with a set date for redemption (repayment). The coupon payments on perpetual bonds will, theoretically, be paid forever – in perpetuity – hence the name, perpetual bonds.

Perpetual bonds are, effectively, a debt obligation, but an obligation in name only, as the issuer is not required to repay the debt as long as they continue making the interest (coupon) payments due to bondholders.

Some economists liken perpetuals to equity investments that pay a dividend amount. However, the similarity between perpetual bonds and dividend stocks is an extremely limited one and, at best, only superficial in nature.

Dividend payments to stock shareholders are typically not a fixed amount but vary over time, based on the company’s performance; whereas, the coupon payments on perpetual bonds are fixed and do not change. Furthermore, investments in perpetual bonds do not carry anything comparable to the voting rights of stock shareholders.

Perpetuals may more closely resemble annuities. An annuity refers to an investment that provides a theoretically perpetual stream of income payments to the investor. In the same way, the coupon payments on perpetual bonds also offer ongoing income payments to investors for an indefinite period of the future.

Many people wonder if the coupon payments on perpetuals are really made “forever” in the event that the bond is never redeemed by the issuer. The short answer is, “Yes.” As an example of this, the holder of a perpetual bond issued in 1648 by the Water Board of the Dutch city of Lekdijk Bovendams was still receiving coupon payments as of 2015.

In practice, the issuer of a perpetual bond usually holds the option to call, or redeem, the bond at any point after a specified time, such as five years from the date of issue. Therefore, some issuers of perpetual bonds eventually redeem their bonds. The issuer still benefits from the fact that perpetuals do not come with a fixed redemption date.

Therefore, the time of redemption is flexible at the issuer’s discretion. They can wait to redeem the bonds at a time when they can most easily afford to do so. The flexibility on repaying the bond’s principal amount may be the main reason that an issuer chooses to go with issuing perpetual bonds.

However, it’s important to keep in mind that the most salient characteristic of perpetual bonds is that their issuer is not obligated to return the investor’s principal.

Perpetuals make up only a very small portion of the total bond market. The primary issuers of perpetual bonds are government entities and banks. Banks issue such bonds as a means of helping them meet their capital requirements – the money received from investors for the bonds qualifies as Tier 1 capital.

Some economists argue that perpetual bonds are an excellent vehicle that financially-stressed governments can use to raise money. However, most classical economists do not approve of governments creating debt that they have no obligation to repay, nor do they consider it sound fiscal policy for a government to take on the contractual responsibility of making payments, to anyone, in perpetuity.

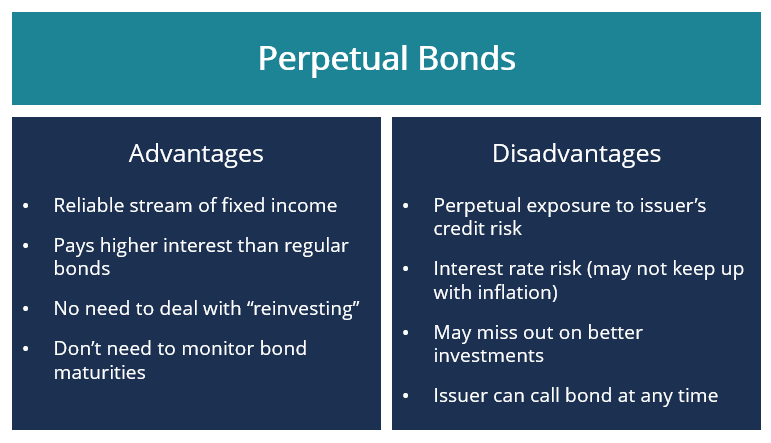

Perpetual bonds are most commonly sought by retirees who are interested in securing a solid stream of regular fixed income payments that they can rely on receiving indefinitely.

Also, to compensate investors for the “no scheduled redemption date” feature of perpetuals, issuers typically offer higher coupon payment rates with perpetual bonds, compared to similar regular bonds with a fixed maturity date.

Another advantage of investing in perpetual bonds is that doing so enables the investor to avoid the need to spend the time and effort required to find a suitable new bond investment when their current bonds mature.

One drawback for investors in perpetual bonds is the fact that they are exposed to the credit risk of the issuer. The credit risk exposure is just as perpetual as the bonds themselves.

Investors may also be exposed to interest rate risk – the risk that their investment will lose value if interest rates rise above their perpetual bond’s coupon rate. To help mitigate the interest rate risk, the issuer of a perpetual bond may offer a step-up feature that periodically increases the coupon rate according to a set schedule.

For example, the coupon rate may be increased by a fixed percentage amount once every 10 or 15 years. Alternatively, the issuer may set up the bond so that the coupon rate, rather than remaining fixed, becomes a floating interest rate – tied to a benchmark interest rate such as the prime rate in the United States – at some designated future point in time.

Investors need to be aware, though, that the issuer may choose to call the bond prior to any interest rate adjustment, to avoid paying the higher coupon rate.

Investors can calculate the yield return they can expect to realize from investing in a perpetual bond as follows:

The current yield on a perpetual bond is equal to the total amount of coupon payments received annually, divided by the market price of the bond, times 100 (to provide the interest rate/yield percentage figure).

So, for example, assume that you invested in a perpetual bond with a par value of $1,000 by purchasing the bond at a discounted price of $950. You receive a total of $80 per year in coupon payments.

Current Yield = [80 / 950] * 100 = 0.0842 * 100 = 8.42%

The current yield from the bond is 8.42%.

Thank you for reading CFI’s guide on Perpetual Bonds. To learn more and continue advancing your career, see the following CFI resources: