Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Accounts that represent ownership of a company

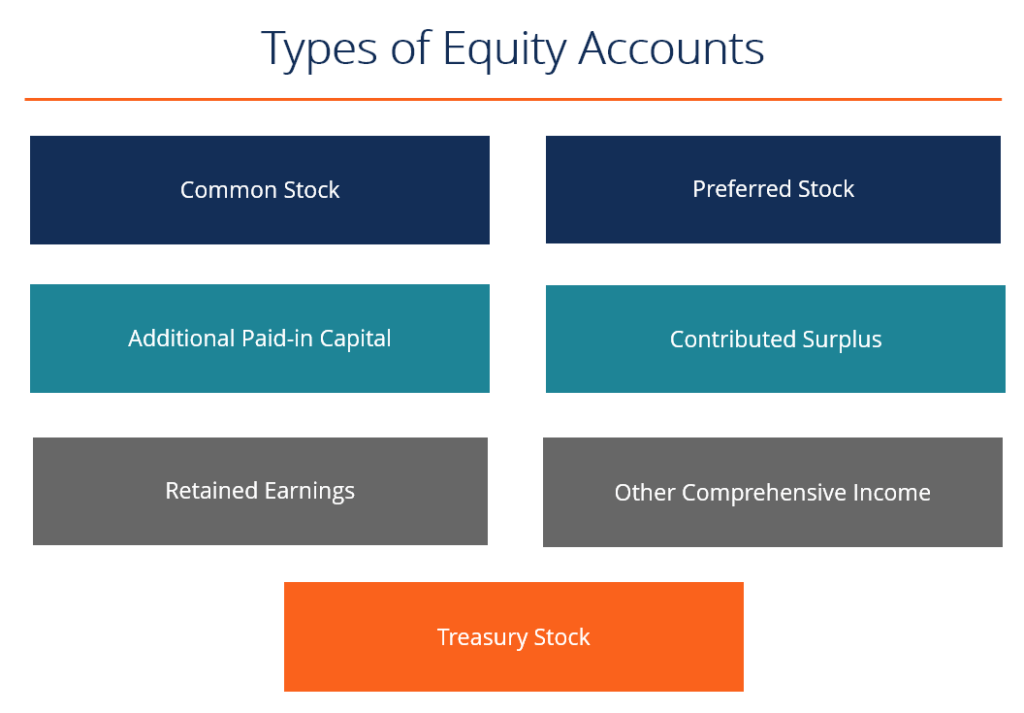

There are several types of equity accounts that combine to make up total shareholders’ equity. These accounts include common stock, preferred stock, contributed surplus, additional paid-in capital, retained earnings, other comprehensive earnings, and treasury stock.

Equity is the amount funded by the owners or shareholders of a company for the initial start-up and continuous operation of a business. Total equity also represents the residual value left in assets after all liabilities have been paid off, and is recorded on the company’s balance sheet. To calculate total equity, simply deduct total liabilities from total assets.

Learn more in CFI’s Free Accounting Fundamentals Course!

The seven main equity accounts are:

Common stock represents the owners’ or shareholder’s investment in the business as a capital contribution. This account represents the shares that entitle the shareowners to vote and their residual claim on the company’s assets. The value of common stock is equal to the par value of the shares times the number of shares outstanding. For example, 1 million shares with $1 of par value would result in $1 million of common share capital on the balance sheet.

Preferred stock is quite similar to common stock. The preferred stock is a type of share that often has no voting rights, but is guaranteed a cumulative dividend. If the dividend is not paid in one year, then it will accumulate until paid off.

Example: A preferred share of a company is entitled to $5 in cumulative dividends in a year. The company has declared a dividend this year but has not paid dividends for the past two years. The shareholder will receive $15 ($5/year x 3 years) in dividends this year.

Contributed Surplus represents any amount paid over the par value paid by investors for stocks purchases that have a par value. This account also holds different types of gains and losses resulting in the sale of shares or other complex financial instruments.

Example: The company issues 100,000 $1 par value shares for $10 per share. $100,000 (100,000 shares x $1/share) goes to common stock, and the excess $900,000 (100,000 shares x ($10-$1)) goes to Contributed Surplus.

Additional Paid-In Capital is another term for contributed surplus, the same as described above.

Retained Earnings is the portion of net income that is not paid out as dividends to shareholders. It is instead retained for reinvesting in the business or to pay off future obligations.

Other comprehensive income is excluded from net income on the income statement because it consists of income that has not been realized yet. For example, unrealized gains or losses on securities that have not yet been sold are reflected in other comprehensive income. Once the securities are sold, then the realized gain/loss is moved into net income on the income statement.

Treasury stock is a contra-equity account. It represents the amount of common stock that the company has purchased back from investors. This is reflected in the books as a deduction from total equity.

Thank you for reading this guide to the various types of equity accounts on a company’s balance sheet. To help you on your path to becoming a certified financial analyst, CFI has many additional resources to help you on your way:

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: