Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The type of expense that is recognized when incurred but not yet paid

Accrued expense is a concept in accrual accounting that refers to expenses that are recognized when incurred but not yet paid.

In some transactions, cash is not paid or earned until the revenues or expenses are incurred. For example, a company pays its February utility bill in March, or delivers its products to customers in May, and receives the payment in June. Accrual accounting requires revenues and expenses to be recorded in the accounting period in which they are incurred.

Since accrued expenses are incurred before they are paid, they become a company liability for future cash payments. Therefore, accrued expenses are also known as accrued liabilities.

There are two types of accounting methods: the accrual method and the cash method. The major difference between the two methods is the timing of recording revenues and expenses. In the cash method of accounting, revenues and expenses are recorded in the reporting period that the cash payment is made. This makes it a simpler method of accounting.

The accrual method of accounting requires revenues and expenses to be recorded in the period that they are incurred, regardless of the time of payment or receiving cash. Since the accrued expenses or revenues recorded in that period may differ from the actual cash amount paid or received in the later period, the records are merely an estimate. The accrual method requires appropriate anticipation of revenues and expenses.

Although the cash method of accounting is easier to use, the accrual method can more accurately reflect a company’s financial health. It allows companies to record their sales and credit purchases in the same reporting period when the transactions occur.

Therefore, the accrual method of accounting is more commonly used, especially by public companies. International Financial Reporting Standards (IFRS) and Generally Accepted Accounting Principles (GAAP) both require companies to implement the accrual method.

Accrued expenses or liabilities occur when expenses take place before the cash is paid. The expenses are recorded on an income statement, with a corresponding liability on the balance sheet. Accrued expenses are usually current liabilities since the payments are generally due within one year from the transaction date.

Some typical cases of accrued expenses include:

At the end of each recording period, a company should properly estimate the dollar amount for each of its accrued expenses, and then record it as an expense account with a corresponding payable/accrued expense liability.

The format of the journal entry is shown below:

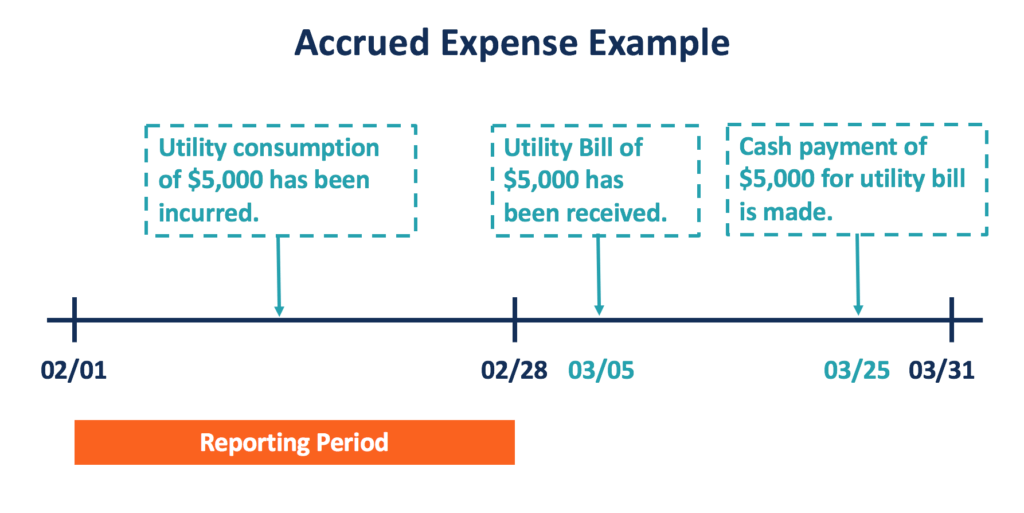

For example, a company consumes $5,000 in utility in February. The expense for the utility consumed remains unpaid on the balance day (February 28). The company then receives its bill for the utility consumption on March 05 and makes the payment on March 25.

Under the accrual method of accounting, the entry for the transaction should be recorded in the reporting period of February, as shown below:

On the balance day, the accrued expense of utility is treated as a current liability (accrued expense or accounts payable) owed to the utility company, and an expense (Utility Expense) incurred by the company in February.

In the reporting period of March, the company should record its cash payment on March 25 for its utility bill. This entry removes the liability since the utility bill is paid in cash.

Because accrued expenses are often confused with trade payables, it’s important to also understand accrued expenses vs accounts payable and how each is recorded.

A related concept under accrual accounting is prepaid expenses. Accrued expenses represent expenditures incurred before cash is paid, but there are also cases in which cash is paid before the expenditures are incurred. Such expenditures are known as prepaid expenses.

Prepaid expenses are an asset on the balance sheet, as the goods or services will be received in the future. Like accrued expenses, prepaid expenses are also recorded in the reporting period when they are incurred under the accrual accounting method. Typical examples of prepaid expenses include prepaid insurance premiums and rent.

In the reporting period that the cash is paid, the company records a debit in the prepaid asset account and a credit in cash. In the later reporting period when the service is used or consumed, the firm will record a debit in expense and a credit to the prepaid asset.

Watch the short video below to quickly understand how accrued expenses work.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.