Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

An estimate of the total income generated for one year

Annualized income refers to an estimate of the total income generated for one year. It is calculated using partial data, and therefore, the income generated represents an estimate of the amount a business or an individual would have earned in one year.

The annualized income helps taxpayers avoid incurring penalties and interest on tax payments due to fluctuating incomes. It is useful in estimating taxes due for a given period and creating budget estimates based on the previous period’s actual figures.

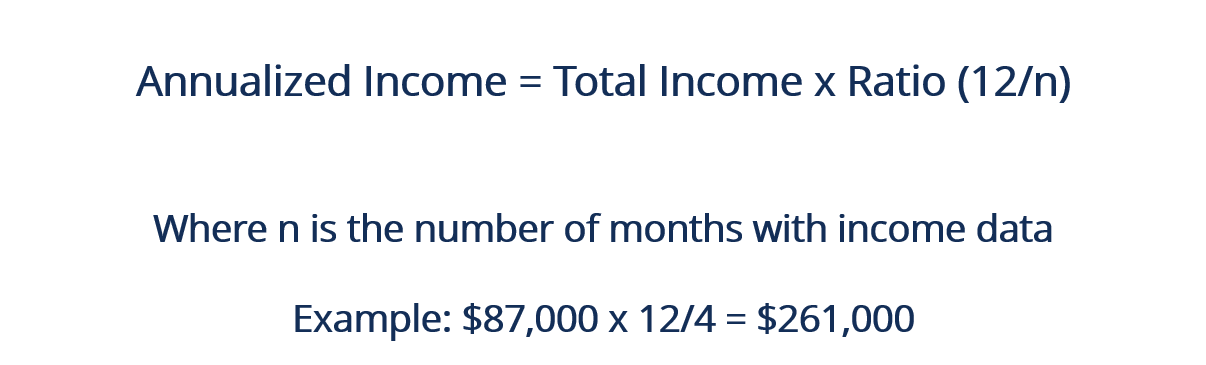

Various methods are used to calculate annualized income, and each method is adapted to the situation. However, the conventional approach entails finding the product between the earned income value by the ratio of twelve months, divided by the given number of months with income data.

For example, consider the hypothetical scenario where the total earnings of a merchant were $20,000 in August, $23,000 in September, $25,000 in October, and $19,000 in November. The four months gives a total earnings of $87,000. The merchant’s income can be annualized by multiplying $87,000 by (12/4) to give $261,000.

Annual tax burdens are remitted either through the withholding of tax or by paying an estimated tax value quarterly. Various sources of income are exempt from tax withholding, including interest from dividends, earnings from self-employment, capital gains, and or other sources that taxpayers indicate on Form 1099. The estimated tax for payment must be at par with total withholding tax and equal to the lesser of 90% of the total unpaid tax.

If a taxpayer’s sources of income fluctuate during a tax year, computing the estimated tax owed is a challenge. Self-employment can be used to illustrate the concept. Income from self-employment varies from one month to another, and it is not consistent.

For example, consider that in the first quarter of a year, a sole proprietor earned a total of $30,000, and in the second quarter, his earnings totaled $45,000. The increased earnings in the second quarter imply a similar increase in income level for the year.

The estimated tax owed is also based on the low level of income. For that reason, the taxpayer may incur the underpayment penalty for the first quarter of the tax year.

Internal Revenue Service (IRS) Form 2210 permits taxpayers to annualize their income quarterly and estimate the amount of tax depending on the level of income. The schedule of IRS Form 2210 can be used to record the taxpayer’s annualized income for each quarter. The taxpayer can estimate the total tax owed relative to the annualized estimate.

For example, consider a self-employed business proprietor who, in the first quarter, earned $30,000, while in the second quarter, his earnings totaled $45,000. IRS Form 2210 allows the proprietor to record and annualize the two incomes for different quarters, independently.

The technique is called an annualized income installment method since it aims to minimize the penalties and underpayments that the taxpayer incurred because of fluctuating incomes.

The annualized income installment method divides the yearly estimates of tax into four equal portions. The estimated value can be used to settle the estimated taxes, provided that the flow of income is steady. The technique, however, does not work well for individuals with fluctuating income.

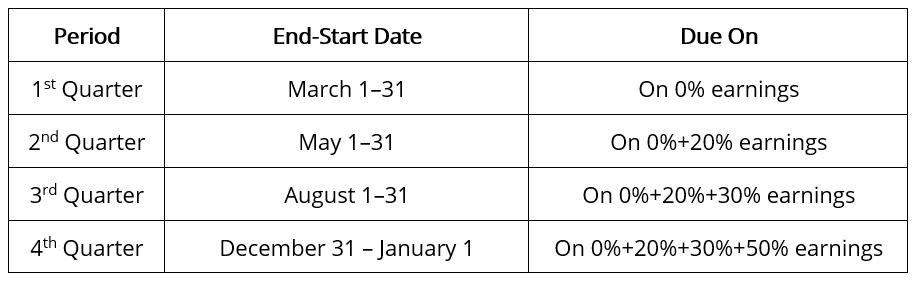

To illustrate, consider two taxpayers, A and B, with each owing a total of $100,000 in annual estimated tax. In addition, each taxpayer makes $25,000 in estimated payments over four installments. Taxpayer A reported a steady income, so the quarterly estimates settled her tax obligations in full. Taxpayer B reported uneven income, with each quarter having 0%, 20%, 30%, and 50%, respectively.

The first two payments resulted in tax overpayment by $25,000 and $5,000, while the last two installments resulted in an underpayment of $25,000 and $5,000. Taxpayer B was subject to four underpayment penalties because, in the first two quarters, he did not pay in full. The last two penalties came from missing the maturity periods.

Taxpayer B can, fortunately, earn penalty relief. He is in a better position to figure out his quarterly installments, so they match with the earnings. Such a correlation is attainable by annualizing the installments over four overlapping periods, where January 1 is the beginning of each period.

The first quarter closes on March 31, the second ends on May 31, the subsequent on August 31, and the final cycle ends on December 31. Note that all previous periods are included in each period, and the last period covers the entire year.

The amounts for the four installments are different. The sum of the installments is equal to Taxpayer B’s estimated annual tax. The new installments are not only paid fully but also lessened.

CFI offers the Financial Modeling & Valuation Analyst (FMVA®) certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following resources will be helpful:

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: