Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Policies and procedures to ensure the reliability of financial statements

Internal controls are policies and procedures put in place by management to ensure that, among other things, the company’s financial statements are reliable. Some internal controls relevant to an audit include bank reconciliations, password control systems for accounting software, and inventory observations.

The objective of the auditor is to identify and assess the risk of material misstatement, whether due to fraud or error, at the financial statement and assertion levels. It includes understanding the entity and its environment and the entity’s internal controls in order to design the proper audit procedures to achieve the desired level of assurance.

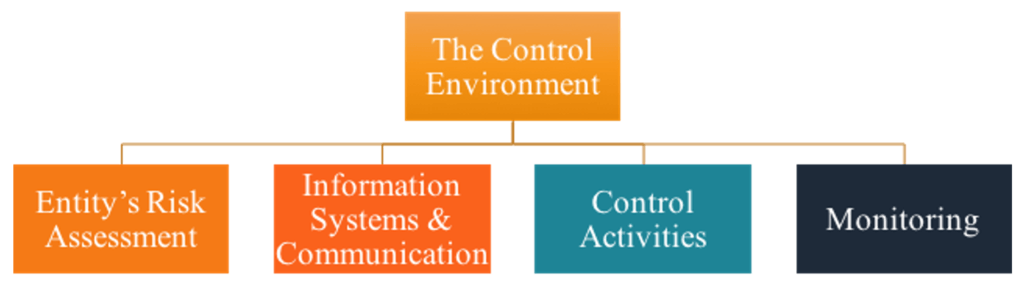

A company’s internal controls framework generally consists of five different aspects, as shown below:

The control environment at the top refers to the attitudes, awareness, and actions of management and those charged with governance towards internal controls. A simpler way to describe this is to call it the “tone at the top.” It is highly important because it filters down to other employees and to all other components of control and can, therefore, have a huge impact on the company.

For example, with a less committed and more relaxed tone, lower-level employees are less likely to follow the internal controls properly.

The entity’s risk assessment relates to how the client identifies and responds to business risks, such as new personnel and new accounting pronouncements. Is the proper training given to employees? Are the new pronouncements fully prepared for and implemented effectively?

The information systems component refers to how the company captures, processes, reports, and communicates transaction information. For example, does the company use distributed processing? How does it deal with system changeovers? Is it using well-recognized accounting software or just something that was cheap to obtain?

Control activities refer to the specific detailed policies and procedures, such as review of company performance through variance analysis, physical and logical controls, and segregation of duties. Segregation of duties is an important internal control that helps prevent a lot of problems, one of which is fraud. By having different employees count inventory and have access to the ledger records, this helps prevent employees from stealing inventory and writing it off on the sub-ledger.

Finally, monitoring controls involve management’s ongoing and periodic assessment of the quality of internal controls to determine which need modification. A common example of this in larger companies is the work done by internal auditors.

Once the auditor understands the client’s internal control system, the auditor must assess control risk. Control risk is the risk that the client’s system will fail to prevent, detect, or correct an error. Ratings range from low to high to maximum. Low means that the client’s internal controls are strong, and maximum means that the controls are virtually useless.

If a client’s internal control system is assessed below maximum, the auditor must test the controls to ensure they are functioning in accordance with the auditor’s understanding.

Testing of internal controls includes making inquiries to management and employees, inspecting source documents, observing inventory counts, and actually re-performing client procedures. Finally, the auditor will perform additional substantive procedures to assess the overall risk level in accordance with the audit strategy.

There are two types of audit strategy:

Although management puts in place internal controls to ensure that the financial statements are more reliable and less prone to error, there are still limitations, such as the possibility of collusion. Even if certain transactions require supervisor approval, if a lower-level staff member and his/her supervisor work together to authorize the transaction, the internal control is not very effective at preventing such a fraudulent act.

Similarly, another limitation is management override. No matter what internal control is in place, if management overrides it and decides to input something else, there is no way to stop the practice. Also, internal controls are designed to address normal transactions and not unusual transactions. Therefore, if numerous unusual transactions occur outside of the ordinary controls, that can threaten the validity of the company’s financial data.

Finally, there is the risk of human error due to employees making ordinary mistakes, such as during busy periods when transaction volumes are significantly higher. Mistakes can also arise as a result of staff turnover.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)® certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below: