Get Certified for

Business Intelligence (BIDA®)

Join over one million professionals who work for global institutions such as Citi, TD, BoA, CBRE, Savills, and more.

A normalized operating profit metric used to understand the economic value of a commercial or industrial investment property

NOI is, arguably, the most foundational component of real estate valuation.

Dividing a property’s NOI by the prevailing CAP rate (Capitalization Rate) for a certain property class in a given geography will provide an estimate of that property’s fair market value, sometimes referred to as FMV., e.g.

$500,000 (NOI) / 5% (CAP rate) = $10,000,000 (property value)

NOI is an important comparable figure and profitability metric used exclusively for income-producing commercial real estate assets. NOI is not the same as net profit or actual profitability by accounting standards. In that sense, think of NOI as being (to commercial real estate finance) very similar to what EBITDA is to corporate finance.

It’s critical to understand just how different these two figures can be, even for the exact same property.

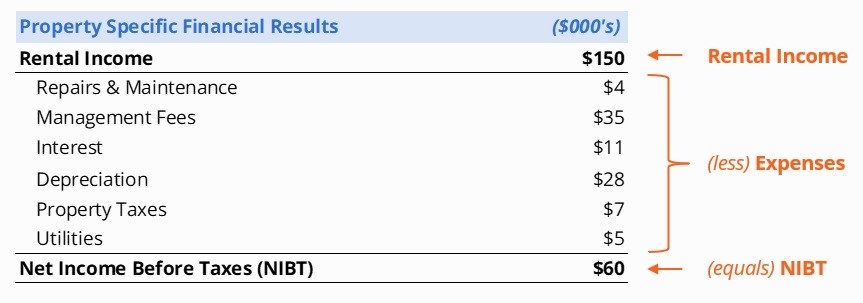

NIBT is an accounting figure, whether we’re talking about an operating business or an investment property. It’s the total revenue minus the total expenses. For real estate, revenue is (largely) rental income:

Total Rental Income – Total Expenses = NIBT

Because passive income tax rates tend to be high in many jurisdictions, it’s a common strategy for real estate investors to try and actively inflate expenses in order to drive down their income tax bills.

Further, where an investor owns multiple properties, net income (or NIBT) may be calculated or presented at the portfolio level. This also makes understanding each individual property’s profitability (or ability to generate cash flow) difficult to understand.

NOI is a metric used to measure the operating profitability of a specific property. NOI, like EBITDA, is often used as a proxy for operating cash flow when calculating debt service coverage ratios or when comparing properties to calculate estimated market values (since it ignores tax rates and capital structure decisions).

The best way to think about NOI is that a number of add-backs and normalizations are required to understand the property’s potential return for an investor.

Consider the following scenarios to help illustrate:

As a general rule, analysts will often see investors and accountants look to understate income for accounting purposes (since it means a lower tax bill), but they will often seek to overstate NOI (since it implies a higher property valuation).

When looking to calculate a property’s NOI, there are four main categories of expenses that must be understood. These are:

Examples include property taxes, utilities, insurance, maybe snow removal, security, or concierge services (where applicable). These are considered “non-controllable” since, if they aren’t paid, it’s likely a breach of contract between the landlord and the tenant(s).

Non-controllable expenses are cash expenses and are never added back to NIBT when calculating NOI.

NOI and NIBT are impacted by three important controllable expense categories. These are repairs & maintenance, management fees, and interest.

They’re controllable in the sense that landlords can “defer” maintenance to overstate NIBT (if looking to sell, for example); they can also complete spurious repairs or maintenance to overstate expenses and pay less tax. Additionally, property owners can pay themselves as much or as little as they want in management fees. And finally, using debt as a funding source is optional, so interest (while an actual cash expense) is one that may or may not appear on all income statements depending on the owner’s preference for high- or low-debt capital structures.

Some controllable expenses are either added back to NIBT (or normalized) to arrive at NOI – we’ll look at an example shortly.

The big one is depreciation expense. Like with EBITDA (for corporate finance), depreciation is a non-cash expense and is therefore added back to NIBT when calculating NOI.

An important example is what’s called a “vacancy allowance.” While many commercial properties may be fully tenanted at the time of financing or acquisition, most commercial real estate professionals and lenders will assign a vacancy allowance to the property.

Vacancy allowances are expressed as a percentage of rental income, and they simulate hypothetical “downtime” where the property may sit vacant for a period of time without any rental income. Vacancy allowances are a function of the geography and the property type, with smaller communities and higher risk property classes usually commanding a higher “hypothetical” vacancy rate.

The simplest way to calculate NOI is to start with NIBT, add back non-cash and controllable expenses, then deduct normalized controllable expenses and “hypothetical” expenses.

Below is our earlier example, but adjusted accordingly:

You’ll notice in this example that the NOI figure of $119,000 is quite different from the NIBT figure of $60,000; it’s fairly common to see some discrepancy, even large ones like this, depending on the various circumstances we covered earlier.

But you can see that the NOI calculation is much more standardized and, therefore, comparable across property classes and geographies (like EBITDA).

Thank you for reading CFI’s guide to NOI (Net Operating Income). To keep advancing your career, the additional resources below will be useful:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: