Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The value of all sales of goods and services recognized by a company in a period

Revenue is the value of all sales of goods and services recognized by a company in a period. Revenue (also known as sales) forms the beginning of a company’s income statement and is often considered the “Top Line” of a business. Expenses are deducted from a company’s revenue to arrive at its profit or net income.

Under the revenue recognition principle in accounting, revenue is recorded when a company has satisfied its performance obligation to the customer. In practice, this means revenue is recognized when the customer obtains control of the good or service.

For products, customers gain control when the item is delivered. For services, it happens when the promised work has been completed or as the service is performed, depending on the contract terms.

Notice the revenue recognition principle doesn’t include anything about payment for goods/services actually being received. Revenue is recorded when the company has fulfilled its performance obligation, whether or not payment has been received yet.

For example, a customer paying with a credit card effectively provides immediate payment to the retailer. However, a business customer who receives an invoice for services might not have to pay for several weeks.

When a company delivers goods or services and allows the customer to pay later, it records revenue at the time of delivery and records the unpaid amount as accounts receivable on the balance sheet.

When the customer eventually pays, no additional revenue is recorded — cash increases and accounts receivable decrease, but the revenue was recognized at the time of the sale.

Revenue is a key indicator of a company’s financial health and potential for growth. It helps with:

Revenue is one of the first numbers that executives, analysts, and investors alike analyze.

In simple terms, revenue is calculated by multiplying the quantity of a product or service sold by its selling price. The revenue formula a company uses can be simple or complicated, depending on whether the business sells products or services.

For a product-based business:

or

For a service-based business:

or

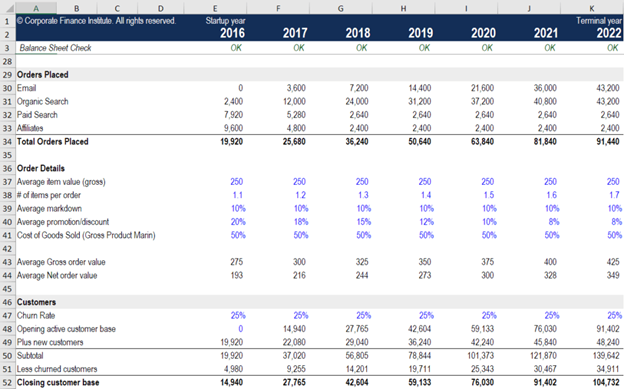

The formulas above can be significantly expanded to include more detail. For example, many finance teams build revenue forecasts all the way down to the individual product level or individual customer level.

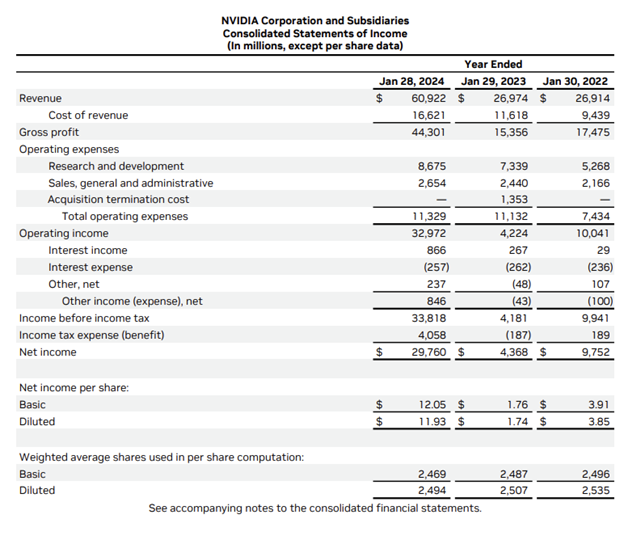

Below is an example of NVIDIA’s 2024 income statement. Let’s take a closer look at revenue for a large public company.

In 2024, NVIDIA recorded $60.9 billion in total revenue. Note how revenue forms the top line of the income statement.

NVIDIA then deducts all operating expenses from total revenue to arrive at an Operating Income of $33.0 billion. Operating Income is also referred to as Earnings Before Interest and Taxes (EBIT).

Finally, interest and taxes are deducted to reach the bottom line of the income statement, $30.0 billion of net income (profit).

Revenue forecasting is essential for budgeting, planning, and valuation. Effective revenue models may include:

Revenue forecasts help guide executives and managers on key decisions such as hiring, production scheduling, and capital investments.

As you can see in the example above, there is much more that can be included in a forecast other than just No. of Units x Average Price.

CFI’s e-Commerce Financial Modeling Course provides a detailed breakdown of how to build this type of model, which is extremely important for forecasting and business valuation.

Sales are the lifeblood of a company, as they allow the company to pay its employees, purchase inventory, pay suppliers, invest in research and development, build new property, plant, and equipment (PP&E), and be self-sustaining.

If a company doesn’t have sufficient revenue to cover the above items, it will need to use an existing cash balance on its balance sheet. The cash can come from financing, meaning that the company borrowed the money (in the case of debt), or raised it (in the case of equity).

In order to perform a comprehensive analysis of a business, it’s important to know how the three financial statements are linked and see how a company either uses its sales to fund the business or must turn to financing alternatives to fund the business.

To learn more, watch CFI’s free webinar on how to link the 3 financial statements in Excel.

Revenue can look different depending on the sector. As you will see, it can be composed of many different things and varies widely in terms of what the most common examples are, by sector.

The three main areas that typically make up the finance industry are public finance, personal finance, and corporate finance. As we demonstrated above, the various sources of income in each type can be quite different. While the above lists are not exhaustive, they do provide a general sense of the most common types of income you’ll encounter.

In accounting, revenue refers to the total amount a company earns from its normal business activities before subtracting any expenses. It represents the inflow of money or value from selling goods, providing services, or performing other core operations.

No. Revenue is not profit or income. Profit (or net income) is what remains after subtracting costs and expenses from revenue.

Here are a few clear examples of revenue, or money a company earns from its normal business activities before deducting any expenses:

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Thank you for reading CFI’s guide to Revenue. To help you advance your career, check out the additional CFI resources below: