Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

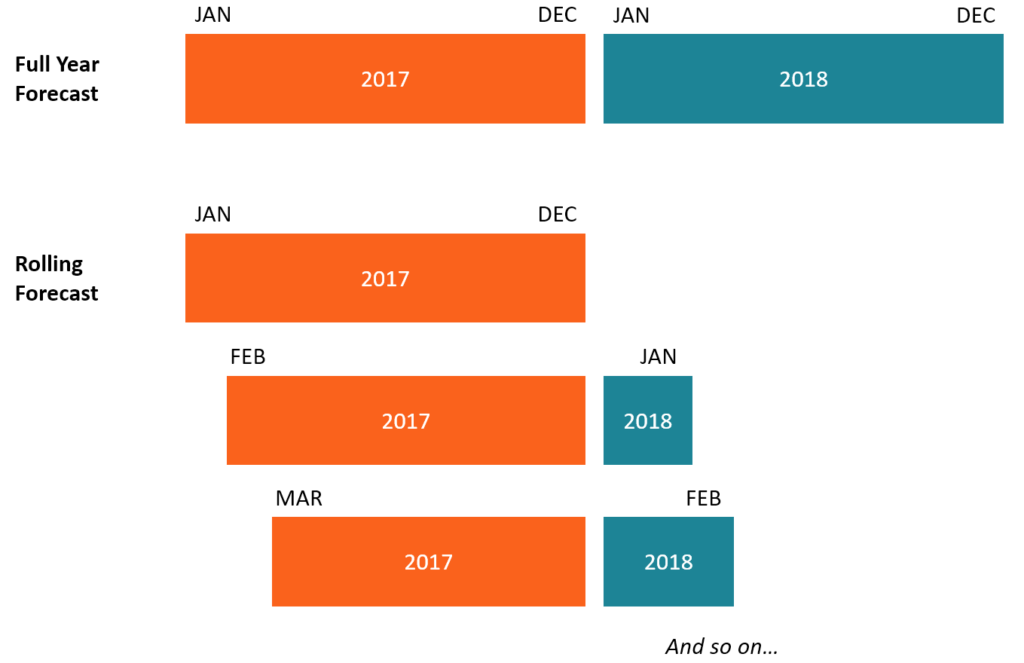

A financial model that moves forward one month at a time

A rolling forecast is a type of financial model that predicts the future performance of a business over a continuous period, based on historical data. Unlike static budgets that forecast the future for a fixed time frame, e.g., January to December, a rolling forecast is regularly updated throughout the year to reflect any changes.

That is, it relies on an add/drop approach to forecasting that drops a month/period as it passes and adds a new month/period automatically. This enables companies to project future performance based on the most recent numbers and time frame, which offers an advantage when operating in a fluid and ever-changing business environment.

Learn more in CFI’s Rolling Cash Flow Forecast Course.

While most traditional businesses use static budgets to assess past performance, a rolling forecast is used to try to predict future performance. With static budgets, the budget remains fixed and does not change as the business evolves. As a result, even if revenues exceed budget estimates, the static budget will remain unchanged until the predetermined time frame has expired.

With rolling forecasts, businesses establish a set of periods after which to update the forecast. For example, if the company sets the period to a month, the budget is automatically updated one month after every month is complete. This allows businesses to be more efficiently responsive by regularly adapting their budgets to reflect recent trends and changes in the marketplace.

The process of creating a rolling forecast should be done in a sequential order to avoid missing some steps. The process to create forecasts is as follows:

The team tasked with creating the rolling forecast should keep the end goal in mind when building the projections. Setting the objectives also involves identifying the usability of the forecasts and the persons who will rely on the forecasts to make decisions. Failure to set clear goals from the start will inhibit the effectiveness of creating rolling forecasts.

A business must keep the time frame of rolling forecasts in mind to help in planning. This involves deciding on how far into the future the forecast will go. The business should determine the forecast increments in advance.

For example, a company may choose the increment period to be weekly, monthly, or quarterly. If management chooses monthly increments for 12 months, after one month expires, it drops out of the forecast and an extra month is added to the end of the forecast. This means that the business is continually forecasting 12 monthly periods into the future, as shown in Figure 1 below.

The length of the forecast period may partially determine how much detail should be included in the forecast. Longer forecasts will typically be less detailed. Also, in a situation where the consequences of a bad decision are potentially very substantial, the creators of the rolling forecast should spend more time and effort to increase the accuracy of the forecasts.

A company must identify the key contributors to the process of creating rolling forecasts. The participants need to be persons who are objective, unbiased, and insightful in order to make meaningful contributions to the process. They should be rewarded when the company achieves set targets and held accountable when the company fails to meet targeted performance.

Rather than focus on all aspects of the business, the company should identify the value drivers most likely to contribute to achieving success. Focusing on too many goals may obstruct the company from achieving the objectives that are most important to its success. The value drivers may be identified from past company successes and from the industry in which the business operates.

The data that the company relies on when creating the rolling forecasts should be reliable and credible to give objective targets. Management must verify that the quality of data is above par and that the source of the data is trustworthy.

An essential step in creating rolling forecasts is assessing possible financial outcomes using certain assumptions and drivers. This gives the company a glimpse of the possible scenarios that it may have to adapt to, depending on the drivers that the company uses.

As new information becomes available or new trends appear, the forecast can be updated and new possible outcomes ascertained. Having advanced knowledge of possible or likely scenarios or outcomes helps company management make better decisions.

Once the rolling forecast has been implemented, it should be tracked to see if there are any variances between the actual performance and the set targets. If there are any variances, the participants in the process should find out what led to the variances and plan courses of action to remedy the situation.

Learn more in CFI’s Rolling Forecast Modeling Course.

A company that uses a rolling forecast as opposed to a static budget enjoys the following benefits:

Businesses operate in an ever-changing environment, which translates to increased risks. By using a rolling forecast, a business can continually adapt to changing economic and industry conditions, which helps reduce the amount of risk exposure. Additionally, the company can identify areas that need more attention and allocate more time and resources to them.

When preparing annual budgets, large businesses often need to consider a number of variables that keep changing from day to day or month to month. For example, the implementation of a government policy that directly affects the business will require the company to adjust its financials to accommodate and reflect the changes.

If the business relies on a static budget, it will need to wait until the next budgeting period to reflect the changes. However, the practice of using a rolling forecast enables a company to respond more quickly to such marketplace changes.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to the Rolling Forecast. To learn more and advance your career, explore the additional relevant CFI resources below: