Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Selling, General & Administrative Expenses

SG&A includes all non-production expenses incurred by a company in any given period. It includes expenses such as rent, advertising, marketing, accounting, litigation, travel, meals, management salaries, bonuses, and more. On occasion, it may also include depreciation expense, depending on what it’s related to.

In an income statement, gross profit less SG&A (and depreciation expense) equals the operating profit, also known as earnings before interest and tax (EBIT).

Image Source: CFI’s Reading Financial Statements course.

Some firms classify both depreciation expense and interest expense under SG&A. If this is the case, then gross profit less SG&A equals pre-tax profit, also known as earnings before taxes (EBT).

The selling component of this expense line is related to the direct and indirect costs of generating revenue (from selling products or services).

Direct expenses are those incurred at the exact point-of-sale for a product or service. Examples of direct selling expenses include transaction costs and commissions paid on a sale.

Indirect selling expenses are incurred either before or after the sale is made, and examples include salaries, benefits, and wages for salespeople, travel, and accommodation expenses.

G&A expenses are the overhead costs of a business, many of which are fixed or semi-fixed. These costs don’t relate directly to selling products or services but rather to the general ongoing operation of the business.

The most common examples are rent, insurance, utilities, supplies, and expenses related to company management, such as salaries of executives, admin staff, and non-salespeople.

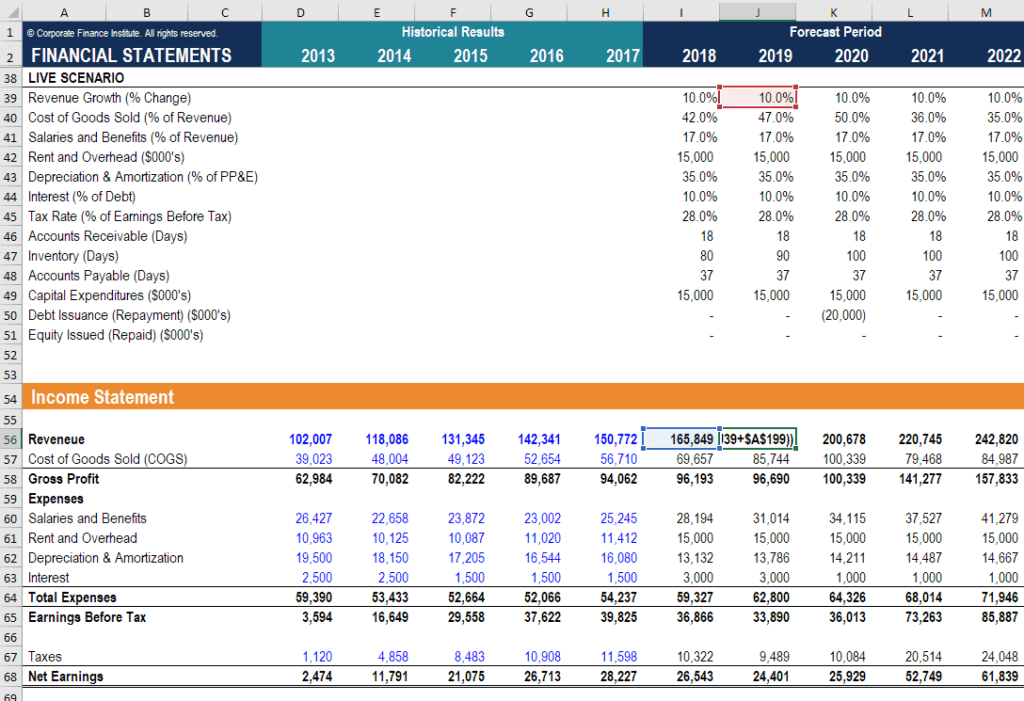

SG&A can be forecasted through any of the following methods: as a percentage of sales revenue, a growth rate over the last period, or as a fixed dollar value.

If SG&A is a consolidated, one-line item, the analyst must use discretion to select one of these (or other) methods to account for all the various expenses baked into that one line item.

Sometimes, SG&A will be a section, with items broken out in individual lines. If this is the case, then different line items will have differing forecast methods. For example, rent most likely will be a fixed dollar value every period. On the other hand, advertising expenses will vary with the strategic decisions a company makes during the given period.

The screenshot above is taken from CFI’s financial modeling courses, which cover forecasting SG&A expenses.

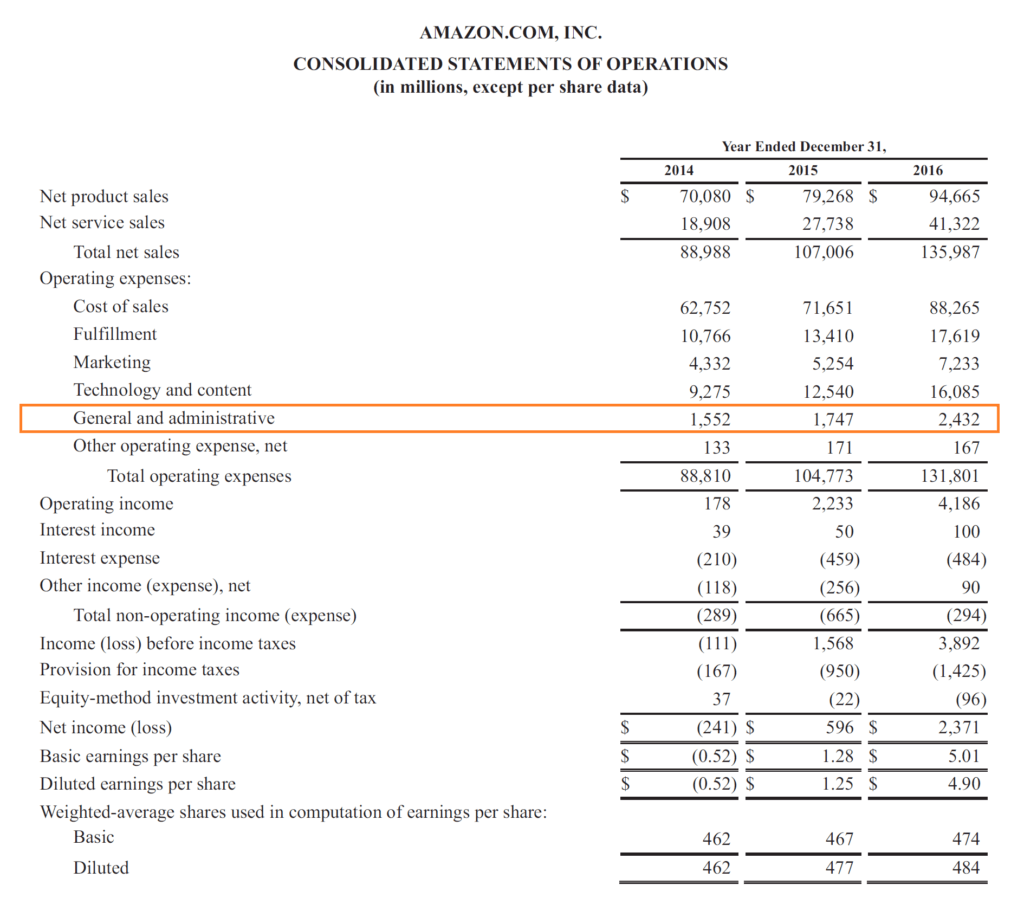

Let’s use Amazon as an example of what’s included in this income statement line item. Below is a quote from Amazon’s 2016 annual report.

“General and administrative expenses primarily consist of payroll and related expenses; facilities and equipment, such as depreciation expense and rent; professional fees and litigation costs; and other general corporate costs for corporate functions, including accounting, finance, tax, legal, and human resources, among others.”

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading this guide to SG&A. To keep advancing your career, the additional CFI resources below may be useful to you: