Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The theoretical cost of a company financing itself, assuming no debt

The unlevered cost of capital is the implied rate of return a company expects to earn on its assets, without the effect of debt.

A company that wants to undertake a project will have to allocate capital or money for it. Theoretically, the capital could be generated either through debt or through equity. The weighted average cost of capital (WACC) assumes the company’s current capital structure is used for the analysis, while the unlevered cost of capital assumes the company is 100% equity financed.

A hypothetical calculation is performed to determine the required rate of return on all-equity capital. This numerical figure or capital is the equity returns an investor expects the company to generate to justify the investment, given its risk profile. In reality, however, this number is just an assumption. Real figures cannot be given.

The theoretical cost is calculated using a formula. This gives an approximate of the likely requirement of the market.

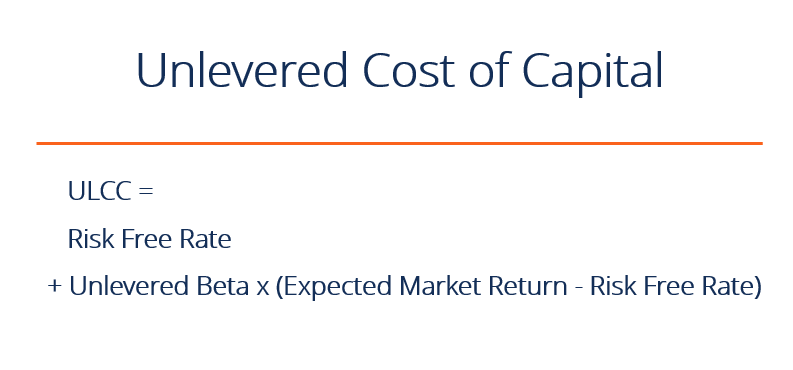

To calculate a company’s unlevered cost of capital the following information is required:

The market risk premium is calculated by subtracting the expected market return and the risk free rate of return. Calculation of the firm’s risk premium is done by multiplying the company’s unlevered beta with the market risk premium.

Beta is the volatility of the stock versus the market, and the volatility of a stock is impacted by the amount of leverage the company has. The unlevered beta removes the effects of leverage from the company’s beta. Learn more.

This points to the theory that a company will have a higher unlevered cost of capital if investors perceive the stock as being higher risk.

Ignoring the debt component and its cost is essential to calculate the company’s unlevered cost of capital, even though the company may actually have debt.

Now, if the unlevered cost of capital is found to be 10% and a company has debt at a cost of just 5%, then its actual cost of capital (WACC) will be lower than the 10% unlevered cost. This unlevered cost is still informative, but if the company fails to achieve the 10% unlevered returns that investors in this market require, then investor capital may move to alternative investments. This will lead to a fall in the company’s stock price.

Enter your name and email in the form below and download the free template now!

Download the free Excel template now to advance your finance knowledge!

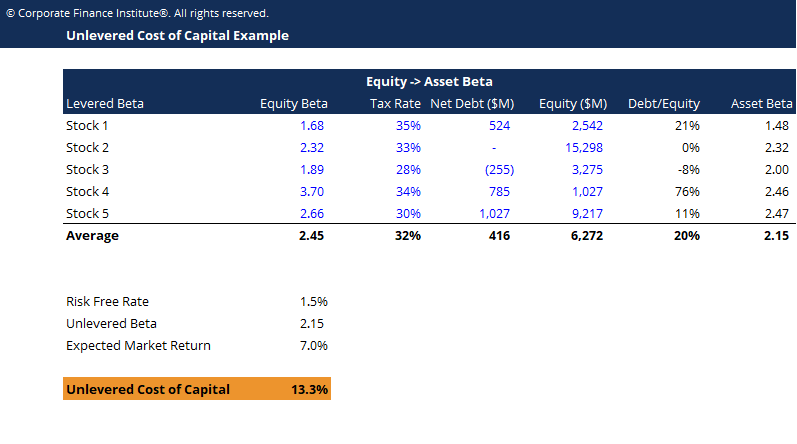

As you can see in the example above, in order to calculate the unlevered cost of capital you need to determine the asset beta (the unlevered beta). Learn how to calculate it in CFI’s Guide to Calculating Unlevered Beta.

Thank you for reading CFI’s guide to Unlevered Cost of Capital. To help you advance your career, check out the additional resources below:

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: