Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

The difference between the yield (return) of two different debt instruments with the same maturity but different credit rating

Credit spread is the difference between the yield (return) of two different debt instruments with the same maturity but different credit ratings. In other words, the spread is the difference in returns due to different credit qualities.

For example, if a 5-year Treasury note is trading at a yield of 3% and a 5-year corporate bond is trading at a yield of 5%, the credit spread is 2% (5% – 3%).

The spread is used to reflect the additional yield required by an investor for taking on additional credit risk. Credit spreads commonly use the difference in yield between a same-maturity Treasury bond and a corporate bond. As Treasury bonds are considered risk-free due to their being backed by the U.S. government, the spread can be used to determine the riskiness of a corporate bond.

For example, if the credit spread between a Treasury note or bond and a corporate bond were 0%, it would imply that the corporate bond offers the same yield as the Treasury bond and is risk-free. The higher the spread, the riskier the corporate bond.

![]()

Note: The maturity dates of both the corporate bond and Treasury bond must be the same.

In addition, it is not uncommon for investors to substitute the Treasury bond yield with a benchmark bond yield of their choice. As such, the formula would look as follows:

![]()

For example, an investor may choose to use an AAA-rated corporate bond yield as the benchmark bond yield.

Credit spreads are not static – they can tighten and narrow over time. The change is generally attributed to economic conditions.

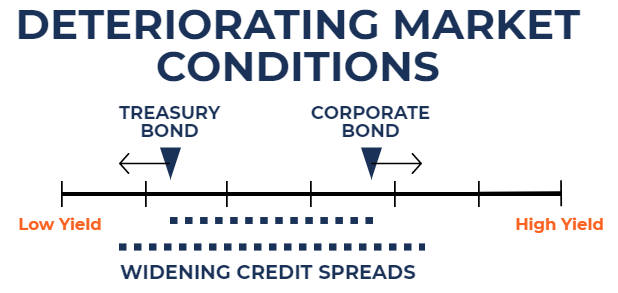

For example, investors tend to purchase U.S. Treasuries during deteriorating market conditions and sell their holdings in corporate bonds. Capital inflows to U.S. Treasuries would increase the price of the treasuries and decrease their yield.

On the other hand, capital outflows from corporate bonds would decrease the price and increase the yield on the bonds. In such a scenario, credit spreads between U.S. Treasuries and corporate bonds would widen. The fact is illustrated below:

On the other hand, in improving market conditions, investors tend to purchase corporate bonds and sell U.S. Treasuries. It is because in improving market conditions, there is lower credit risk in corporate bonds. Capital inflows to corporate bonds would increase the price of the bonds and decrease their yield.

On the other hand, capital outflows from U.S. Treasuries would decrease the price and increase the yield on the treasuries. In such a scenario, credit spreads between U.S. Treasuries and corporate bonds would narrow. The fact is illustrated below:

An investor is looking to determine the condition of the U.S. economy. Historically, the average credit spread between 2-year BBB-rated corporate bonds and 2-year U.S. Treasuries is 2%. The current yield on a 2-year BBB-rated corporate bond is 5%, while the current yield on a 2-year U.S. Treasury is 2%. What is the current credit spread, and what insight is an investor able to gain from looking at the change in credit spreads?

The current spread is 3% (5% – 2%). With credit spreads historically averaging 2%, this may provide an indication that the U.S. economy is showing signs of economic weakness.

Thank you for reading CFI’s guide on Credit Spread. To keep learning and advancing your career, the following CFI resources will be helpful: