Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

The predicted amount of loss a bank may face in the event of, and at the time of, the borrower's default

Exposure at Default (EAD) is the predicted amount of loss a bank may face in the event of, and at the time of, the borrower’s default. The loss is dependent upon the amount to which the bank was exposed to the borrower at the time of default, as the default occurs at an unknown future date. It is obtained by adding the risk already drawn on the operation to a percentage of undrawn risk.

Banks often calculate an EAD value for each loan and then use the figures to determine their overall default risk. It is a dynamic number that changes as a borrower repays a lender.

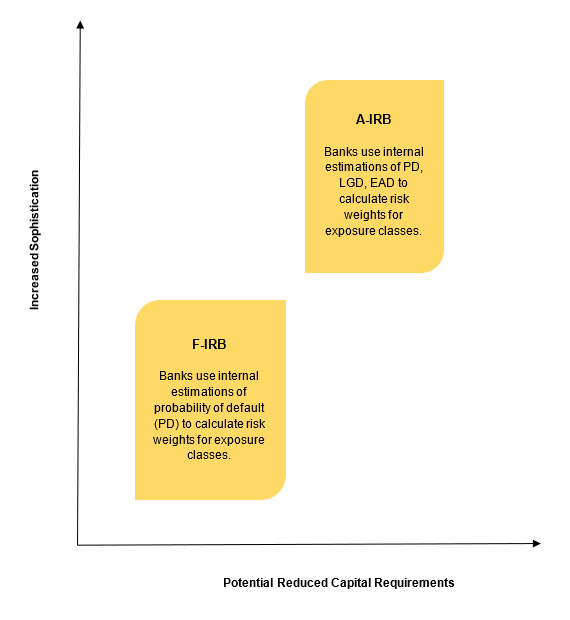

While under the foundation internal ratings-based approach (F-IRB), calculation of EAD is guided by regulators, under the advanced approach (A-IRB), banks enjoy greater flexibility on how they calculate EAD.

Under the foundation approach, Exposure at Default is calculated, taking account of the underlying asset, forward valuation, facility type, and commitment details. The value does not take account of collateral, guarantees, or security (ignores Credit Risk Mitigation Techniques with the exception of on-balance sheet netting where the effect of netting is included in EAD).

EAD is similar to the nominal amount of exposure for on-balance sheet transactions. Under certain conditions, the on-balance sheet netting of loans and deposits of a bank to a corporate counterparty is allowed to reduce the estimate of Exposure at Default.

For off-balance sheet items, there are two broad types that the foundation approach needs to address: transactions with uncertain future drawdown, such as commitments and revolving credits, and OTC foreign exchange, interest rate, and equity derivative contracts.

Under the advanced approach, the bank itself determines how the appropriate EAD is to be applied to each exposure and streamlines its capital requirements by isolating the specific risk factors that are most serious and downplaying others. A bank using internal EAD estimates for capital purposes might be able to differentiate EAD values based on a wider set of transaction characteristics and borrower characteristics.

The values (as with PD and LGD estimates) would be expected to represent a conservative view of long-term averages, though banks would be free to use more conservative estimates.

A bank wanting to use its own estimates of EAD will need to demonstrate to its supervisor that it can meet additional minimum requirements pertaining to the reliability and integrity of the estimates. All estimates of EAD should be computed net of any specific provisions a bank might have raised against an exposure.

Banks can help reduce their capital charge by using an advanced IRB approach.

PD (Probability of Default) analysis is a method generally used by larger institutions to calculate their expected loss. A PD is assigned to a specific risk measure and represents the likelihood of default as a percentage. It is usually measured by assessing past-due loans and is calculated by running a migration analysis of similarly rated loans. The calculation pertains to a specific time horizon and measures the percentage of loans that default.

LGD (Loss Given Default), which is unique to the banking industry or segment, measures the expected loss. It represents the amount unrecovered by the lender after selling the underlying asset if a borrower defaults on a loan.

An accurate LGD variable may be difficult to determine if portfolio losses are different from what was expected, or if the segment is statistically small. Industry LGDs are available from third-party lenders.

PD and LGD values are generally valid throughout an economic cycle. However, lenders will re-evaluate with changes to the market or portfolio composition. Economic recovery, recession, and mergers may call for reevaluation.

A bank may calculate its expected loss by taking the product of EAD, PD, and LGD.

In response to the Global Financial Crisis of 2007-2008, the banking sector adopted international regulations to lessen its exposure to default. EAD (Exposure at Default) and LGD (Loss Given Default) estimates are key inputs in the measurement of the expected and unexpected credit losses and, hence, credit risk capital (regulatory and economic).

The regulatory framework (Basel III) put forth by the Basel Committee on Bank Supervision (BCBS) following the financial crisis aims to improve the banking sector’s ability to deal with shocks arising from financial and economic stress. By improving risk management, disclosure standards, and bank transparency, the international accord hopes to avoid a domino effect of failing financial institutions.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI offers the Commercial Banking & Credit Analyst (CBCA)™ certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant resources below: