Risk Rating Models

Tools used to assess the probability of default

What are Risk Rating Models?

Risk rating models are tools used to assess the probability of default. The concept of a risk rating model is deeply interconnected with the concept of default risk and a key tool in areas such as risk management, underwriting, capital allocation, and portfolio management.

Risk rating models use several factors and implement a set of rules to assess the default probability of a borrower or debt security. The models generally use these factors and rules to generate a numerical or symbol-based rating that summarizes the level of default risk of the borrower or debt security involved.

How Risk Rating Models are Used

A risk rating model is a key tool for lending decisions and portfolio management/portfolio construction. They give creditors, analysts, and portfolio managers a rather objective way of ranking borrowers or specific securities based on their creditworthiness and default risk.

They also allow a bank to set and monitor the level of risk in their credit portfolio and assess whether specific adjustments are needed.

Factors Used in Risk Rating Models

Risk rating models generally use a variety of factors as inputs. Some risk rating models may be purely based on statistical evidence, while others may rely on more subjective elements. Generally, most of the factors used in the models are quantitative. However, financial institutions often combine quantitative factors and qualitative components that may involve judgment and subjective assessments.

The factors used in risk rating models generally look at a borrower’s health, industry characteristics and conditions, and macroeconomic factors, to name a few.

Other factors may involve a subjective assessment of a company’s competitive strengths, management’s reliability, political risks, and environmental risks. For these factors, it’s often necessary to use discretion when ranking the related risks, as it’s difficult, if not impossible, to quantify or rank them in an objective way.

1. Judgment vs. Data

The methodology used to develop the risk rating model can give more weight to judgment or statistics. It will depend on the availability of relevant data, the integrity and accuracy of the data, and the ease of storage and access to such data.

2. Borrower’s Financial Health

The factors that assess a borrower’s financial health generally include a variety of ratios:

- Liquidity, to determine whether a borrower is able to pay off their current obligations. Such ratios include the cash ratio, the current ratio, and the acid ratio.

- Leverage ratios, also called solvency ratios, to assess a company’s ability to meet its long-term financial obligations. These ratios look at a company’s capital structure and include the equity ratio or the debt ratio.

- Profitability ratios, to determine whether the company generates profits in its ordinary business activities. Such ratios include the operating margin, the EBITDA margin, and the return on invested capital, to name a few.

- Cash flow ratios, which compare cash flow metrics to other financial KPIs or leverage indicators, to assess a company’s ability to generate cash flows that can be used to pay off its obligations. For example, such ratios include the cash flow coverage ratio or the cash flow to net income ratio.

3. Industry Characteristics

A borrower’s ability to pay off their obligations may not just depend on company-specific factors. Industry characteristics and macroeconomic factors can affect a company’s creditworthiness. For example:

- In an industry with low barriers to entry, a company’s ability to generate cash flows may be less predictable or subject to more significant risks.

- In a cyclical or commoditized industry, a company’s cash-flow generation may be significantly more volatile than in a defensive industry or natural monopoly.

- For any industry, the current phase of the industry or business cycle can affect a company’s creditworthiness. For example, in the recession phase of the macroeconomic cycle or in the decline phase of the industry cycle, even companies that are financially healthy may face a deterioration in creditworthiness.

4. Management’s Quality and Reliability

Many risk rating models give a score to a company’s management based on a combination of objective and subjective factors:

- Assessment of the management’s tenure and experience, which comprise rather objective elements, such as the management’s seniority and years of experience, and more subjective ones, such as the relevance of the experience and qualifications.

- A deeper analysis of a management’s history of value creation, clarity of communication, quality and frequency of information disclosed, and capital allocation decisions.

5. Political and Environmental Risks

Risk rating models also use additional categories of risk factors:

- Political risks, which consider aspects such as the risks of war, the rule of law, and the reliability of the institutions, to name a few.

- Environmental risks related to the potential consequences of pollution or destruction of the natural environment due to the company’s activity. It can cause financial consequences and even adverse regulations that can limit or disrupt a company’s operations.

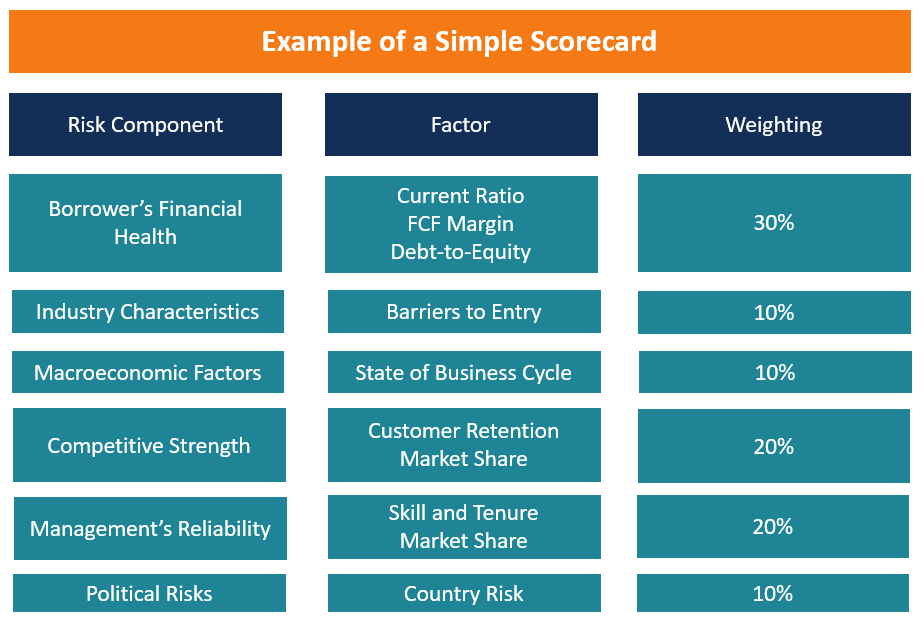

Example of a Scorecard-based Risk Rating Model

Validation of a Risk Rating Model

A risk rating model should only be used if it is accurate enough. Validating the model means assessing whether the risk rating generated by the model is consistent enough with the actual outcomes.

A good risk rating model should not:

- Underestimate the risks, as this would generate unexpected losses and costs of recovery;

- Overestimate the risks, as this would lead to noncompetitive bidding and loss of potential profits.

More Resources

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful: