Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

A type of debt instrument that is provided to individuals with a low credit score

A subprime mortgage is a type of debt instrument that is provided to individuals with a low credit score and whose chances of paying back the loan are lower than other individuals. The bank charges a higher rate of interest for taking such an additional risk.

A credit score is a number that represents the creditworthiness of an individual. The credit score is used mostly by financial institutions when they want to lend money to a borrower. One can attain a good credit score by paying the full current balance on their credit card on time each month.

Also, making timely payment of utilities and monthly loan payments can help towards maintaining a good credit score. A score between 670 and 740 is generally considered a good score.

Subprime mortgages help individuals with low credit scores to fulfill their dream of owning a house.

Since subprime mortgages only require the borrower to pay the interest, it gives them the opportunity to increase their credit score by paying off other debts and then plan for paying off the principal amount.

Subprime mortgages allow the borrower to pay off the interest on the mortgage for the first few years. The borrower’s plan is to refinance the mortgage or sell off the property at a profit when it’s time to pay the principal amount.

The downside is that if property prices go down, the borrower will not be able to refinance the mortgage, nor will they be able to sell the property at a loss. In such a case, they will default on the mortgage, which was the main reason behind the subprime crisis of 2008.

Subprime mortgages are advertised as an affordable way to buy a house with a low credit score. The downside here is that after a few years, the monthly payments will increase with the payment of the principal amount, which will make it difficult for the borrower to pay the mortgage. It often leads to default.

Also, the costs associated with borrowing the subprime mortgage are very high due to the added risk that the lender takes.

Financial institutions and hedge funds were under pressure to outperform the stock market. On one side, banks and other lenders were trying to ease the regulations for borrowers to obtain subprime mortgages. On the other hand, they were selling the mortgages as a bundle – called mortgage-backed securities – to large banks and financial institutions, which, in turn, sold them to investors through investment products.

It was done so that they could transfer the risk and obtain cash. The products were also highly rated by the credit rating agencies, which made them very attractive to investors all around the world.

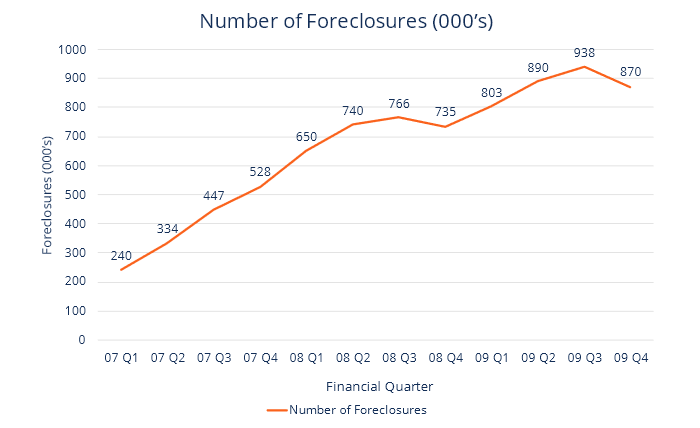

The diagram below illustrates the number of foreclosures that took place between 2007 and 2009:

The mortgage-backed securities were providing good returns to the investors, as the real estate market was doing extremely well in 2005 and accounted for one-third of the total mortgage market. Borrowers of the subprime mortgages were also able to refinance their mortgages or sell their houses comfortably due to the increase in real estate prices.

The downfall of the pretty mortgage market came in 2007 when housing prices started to fall, and the Federal Reserve started to increase interest rates. The lenders were forced to increase the interest rate on the subprime mortgages, making it difficult for the borrowers to pay the monthly installment and also refinance the mortgage. The move led to a huge number of mortgages defaulting.

The above scenario led to a decrease in the interest rates on the mortgage-backed securities, and the investors holding MBS products found it difficult to sell these securities off, as there was no buyer in the market for such products. Hence in 2008, it led a lot of investors, including big banks and financial institutions, to file for bankruptcy.

Many big names like American Life Insurance (AIG), Citi Group, Bank of America, and others invested the money they received from savings and other accounts held by investors to purchase the mortgage-backed securities.

When the financial crisis took place, these companies defaulted on paying their investors, and because they were considered systemically important financial institutions – i.e., companies whose failure can impact the world’s economy and can lead to a crisis – it led to the Global Financial Crisis of 2008. It resulted in the closure of many businesses, and also nearly 2.6 million people lost their jobs in the United States alone.

The U.S. government was forced to bail out a lot of companies that were systemically important financial institutions and imposed strict rules on where these companies should invest the people’s money going forward.

CFI is the official provider of the Certified Banking & Credit Analyst (CBCA)® certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below: