Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Proposed M&A deals that go through due diligence but fail to close

Dead deals refer to merger and acquisition deals that go through due diligence but do not close, due to various reasons related to either the seller or the buyer. When deals fail to close, various costs are incurred, both direct and indirect. These are referred to as dead deal costs. The costs are those related to facilitating the transaction and may be incurred acting on behalf of the buyer or the seller.

Learn more about M&A Financial Modeling with CFI’s M&A Modeling Course.

When both the seller and the buyer work together to make a transaction go through to the end, they incur various costs to facilitate the transaction. The majority of the costs from dead deals are incurred during due diligence, when the parties spend a lot of time and resources in verifying the other party’s proposed transaction and financial information.

On the buy side, the buyer is interested in knowing if the financial reports presented by the seller represent the actual state of affairs at the target business. The buyer will attempt to find out the performance of the company over recent financial periods and seek explanations for revenue increases and decreases.

The buyer will also be interested in knowing any liabilities attached to undisclosed assets, and any other information that may affect the transaction. The costs incurred in conducting due diligence are considered dead deal costs if the transaction fails to close.

On the other side, the seller conducts due diligence on the buyer to know their history of closing deals. The seller wants to transact with a buyer with solid financing and a positive history of closing deals. For example, if several buyers expressed interest in acquiring the seller ’s business, the seller would perform due diligence to weed out buyers with a questionable past. The costs that the seller incurs in conducting background checks are counted as dead deal costs if the seller fails to close a deal with one of the buyers.

The following are some of the third-party deal costs that sellers and buyers may incur during merger and acquisition transactions that fail to close:

During an M&A transaction, both the seller and the buyer pay attorneys to draft legal documents for them, as well as to handle any legal matters that the parties are required to clear before proceeding with the transaction. Some of the legal documents that may be prepared by an attorney include non-compete agreements, purchase and sale agreements, a letter of intent, or an employment contract.

When the seller is disposing of property or equipment, it will invite a valuation specialist to provide the latest valuation of the property or equipment. The assessment helps in determining the price that the seller is willing to accept as a payment for the purchase of an asset.

When selling certain types of assets, such as factories and manufacturing facilities, the law requires the parties to conduct an environmental assessment of the plan to determine potential consequences on the environment.

When undertaking a capital-intensive acquisition or merger, the buyer will invite tax practitioners to provide them with the most efficient purchase plan for minimizing tax liability. The buyer will want to go with the plan that saves them the most money while still complying with the tax laws.

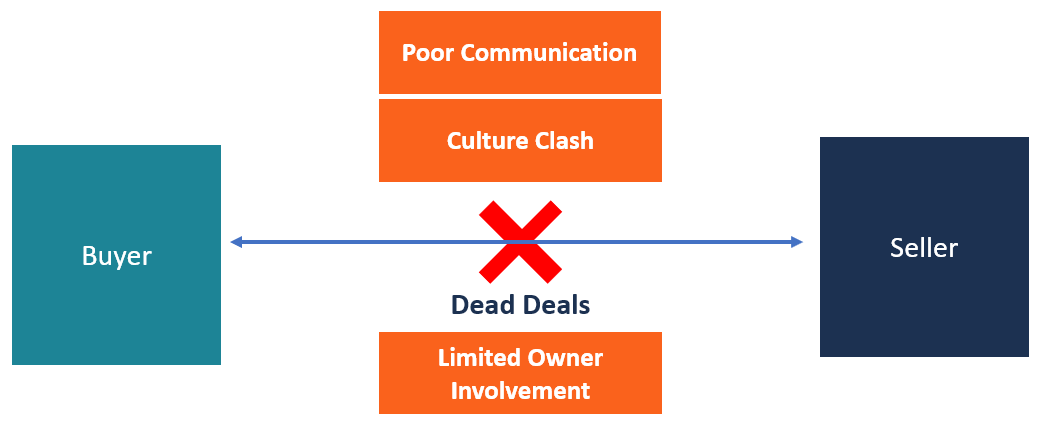

There are several reasons why M&A deals may collapse midway during negotiations between the seller and the buyer. They include the following:

One of the leading causes of M&A deal failures is a culture clash between the seller’s and buyer’s businesses. While the buyer may have expressed interest in acquiring the target company, it might not be privy to the company’s culture before the purchase negotiations. If the buyer discovers that the target company has a markedly different corporate culture than its own, it may pull out of the deal to avoid possible conflicts post-acquisition.

Another reason for deal failure is limited or no involvement of the actual owners of the business. The buyer’s side, for example, may hire M&A advisors to oversee the transaction on their behalf. However, the M&A advisors can only do what is within their powers and cannot take over the functions of the actual buyer. This means that when the actual buyer is absent from the negotiations, it will usually derail the transaction.

The buyer may also become bankrupt or simply experience financial problems during the acquisition process, especially when it involves a high-value transaction. The buyer may be unable to meet all the acquisition costs, or financial institutions may be reluctant to advance credit to the buyer.

CFI offers the Financial Modeling & Valuation Analyst (FMVA)™ certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following CFI resources will be helpful: