Get In-Demand Finance Certifications

The practice in which the acquirer allocates the purchase price into the assets and liabilities of the target company

In acquisition accounting, purchase price allocation is a practice in which an acquirer allocates the purchase price into the assets and liabilities of the target company acquired in the transaction. Purchase price allocation is an important step in accounting reporting after the completion of a merger or acquisition.

The currently accepted accounting standards, such as the International Financial Reporting Standards (IFRS), require employing the purchase price allocation method for any type of business combination deal, including both mergers and acquisitions. Note that past accounting standards required purchase price allocation only in acquisition deals.

Purchase price allocation primarily consists of the following components:

Net identifiable assets refer to the total value of assets of an acquired company, less the total amount of its liabilities. Note that the “identifiable assets” are those with a certain value at a given point in time and whose benefits can be recognized and reasonably quantified.

Essentially, the net identifiable assets represent the book value of assets on the balance sheet of the acquired company. It is important to understand that identifiable assets may include both tangible and intangible assets.

A write-up is an adjusting increase to the book value of an asset that is made if the asset’s carrying value is less than its fair market value. The write-up amount is determined when an independent business valuation specialist completes the assessment of the fair market value of assets of a target company.

Essentially, goodwill is the amount paid in excess of the target company’s net value of its assets minus its liabilities. Goodwill is calculated as a difference between the purchase price and the total fair market value of assets and liabilities of an acquired company.

From an acquirer’s perspective, goodwill is critical in its accounting reporting because both US GAAP and IFRS require a company to re-evaluate all recorded goodwill at least once a year and record impairment adjustments if necessary. Goodwill is not depreciated but is sometimes amortized over time.

Note that acquisition-related costs – including, but not limited to, various legal, advisory, or consulting fees – are not considered in purchase price allocation. According to accounting standards, an acquirer must expense the costs whenever they have been charged while the corresponding services have been provided.

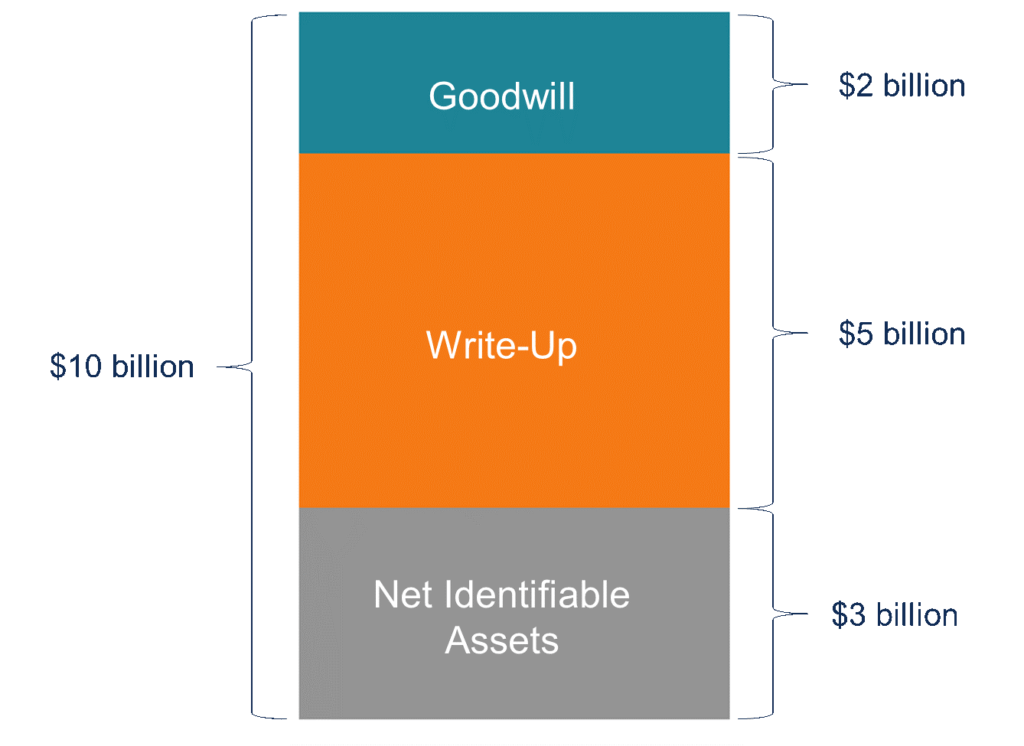

Company A recently acquired Company B for $10 billion. Following the completion of the deal, Company A, as the acquirer, must perform purchase price allocation according to existing accounting standards.

The book value of Company B’s assets is $7 billion, while the book value of the company’s liabilities is $4 billion. Therefore, the value of the net identifiable assets of Company B is $3 billion ($7 billion – $4 billion).

The assessment of an independent business valuation specialist determined that the fair value of both assets and liabilities of Company B is $8 billion. This finding implies that Company A must recognize a $5 billion write-up ($8 billion – $3 billion) to adjust the book value of the company’s assets to its fair market value.

Finally, Company A must record goodwill since the actual price paid for the acquisition ($10 billion) exceeds the sum of the net identifiable assets and write-up ($3 billion + $5 billion = $8 billion). Therefore, Company A must recognize $2 billion ($10 billion – $8 billion) as goodwill.

Thank you for reading CFI’s guide to Purchase Price Allocation. To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover:

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.