Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

An economic theory that combines the cost of production theory from classical economics and the concepts of utility maximization and marginalism

Neoclassical economics is a broad approach that attempts to explain the production, pricing, consumption of goods and services, and income distribution through supply and demand. It integrates the cost-of-production theory from classical economics with the concept of utility maximization and marginalism. Neoclassical economics includes the work of Stanley Jevons, Maria Edgeworth, Leon Walras, Vilfredo Pareto, and other economists.

Neoclassical economics emerged in the 1900s. In 1933, imperfect competition models were introduced into neoclassical economics. Some new tools, such as indifference curves and marginal revenue curves, were used. The new tools were instrumental in improving the sophistication of its mathematical approaches, boosting the development of neoclassical economics.

In the 1950s, Keynesian macroeconomic theories and neoclassical microeconomic theories were combined. The combination led to the neoclassical synthesis, which has dominated economic reasoning since then.

There are many branches that use different approaches under neoclassical economics. All of the approaches are based on three central assumptions:

With the fundamental assumptions above, various studies and approaches have been developed. For example, utility maximization can explain the demand for a product or service. The interaction of demand and supply explains the pricing and thus the distribution of production factors.

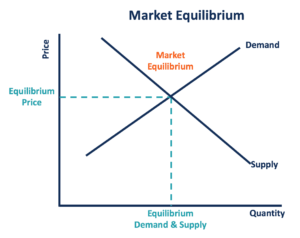

Neoclassical economics is primarily concerned with the efficient allocation of limited productive resources. It also considers the growth of the resources in the long term. The growth will allow for expanding the production of goods and services. It emphasizes that market equilibrium is the key to an efficient allocation of resources. Thus, market equilibrium should be one of the primary economic priorities of a government.

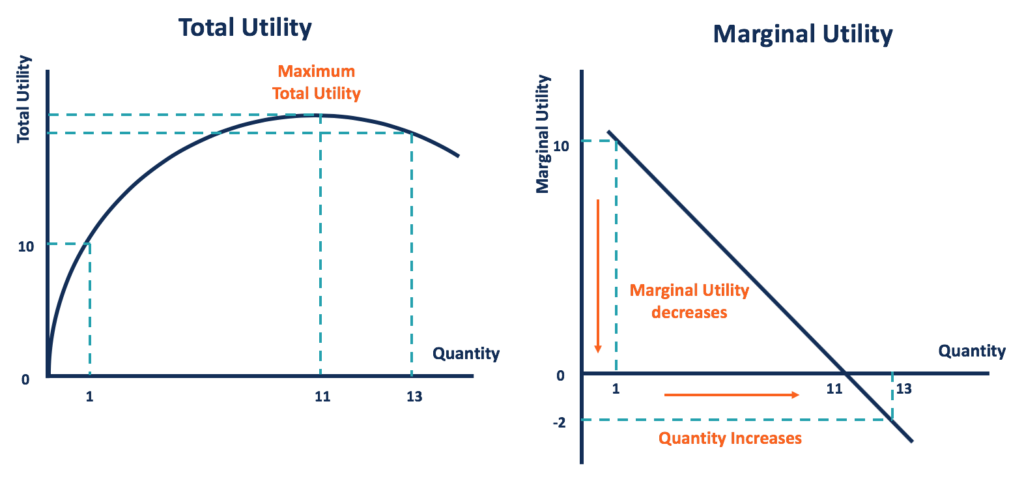

Neoclassical economics also developed studies about utility and marginalism. Utility measures the satisfaction received by consuming goods and services. It states that people’s decision-making over consumption depends on their evaluation of utility. People allocate their incomes to maximize their levels of utility. Thus, utility is a key factor driving the value of a product or service.

Marginalism explains the change in the value of a product or service with an additional amount. Combining the two concepts brings us to the “marginal utility.” Marginal utility refers to the change in utility as a result of an increase in consumption.

The law of diminishing marginal utility states that as the quantity consumed increases, the marginal utility decreases. The marginal utility can even turn negative beyond a certain level of quantity. Thus, the total utility maximizes at the quantity where the marginal utility equals zero.

Classical economics emerged in the 18th century. It includes the work of Adam Smith, David Ricardo, and many other economists. The value and distribution theory of classical economics states that the value of a product or service depends on its cost of production. The cost of production is determined by the factors of production, which include labor, capital, land, and entrepreneurship.

Neoclassical economics is derived from classical economics with the introduction of marginalism. It is stated that people make decisions based on margins (for example, marginal utility, marginal cost, and marginal rate of substitution). The process is known as the “marginal revolution.”

There are several major differences between classical economics and neoclassical economics. In terms of their theories, classical economics states that the price of a product is independent of its demand. The production and other factors that impact the supply of that product are the key drivers.

Neoclassical economics emphasizes the choices (demand) of consumers. Personal preferences, allocation of resources, and some other factors can influence consumer demand. Thus, in neoclassical economics, the value of products and services are above their costs of production.

In terms of their approaches, the study of classical economics is more empirical. It focuses on explaining the capitalist mode of production through social and historical analyses. The study of neoclassical economics depends on mathematical models. It implements a mathematical approach instead of a historical concept.

One of the most common criticisms of neoclassical economics is its unrealistic assumptions. The assumption of rational behaviors ignores the vulnerability and irrationality in human nature.

Behavioral economics focuses on studying irrational behaviors in economic decision-making. The study provides empirical evidence of human behaviors in an economy. It is also argued whether utility or profit maximization is the only goal of an individual or company.

Neoclassical economics is criticized for its over-dependence on its mathematical approaches. Empirical science is missing in the study. The study, overly based on theoretical models, is not adequate to explain the actual economy, especially on the interdependence of an individual with the system. It can also lead to normative bias.

Neoclassical economics is also considered overly dependent on complex, unrealistic mathematical models. The complex models are not applicable to describe the real economy. In response to the criticism, American educator and economist Milton Friedman claimed that a theory should be judged by its ability to predict. The complexity of the model or realism of the assumptions is not a standard to judge a theory.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide on Neoclassical Economics. To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below: