Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Guide to a successful capital raising

This article is intended to provide readers with a deeper understanding of how the capital raising process works and happens in the industry today. For more information on capital raising and different types of commitments made by the underwriter, please see our underwriting overview.

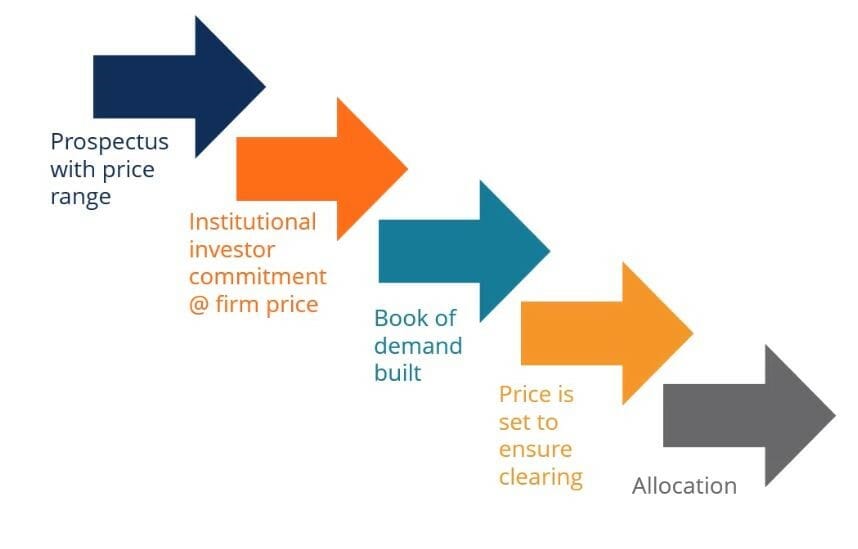

During the second phase of underwriting advisory services, investment bankers must estimate the expected investor demand. This includes an evaluation of current market conditions, investor appetite and experience, news flow, and benchmark offerings. Based on all the conditions, investment bankers or underwriters will draft a prospectus with a price range they believe reflects expected investor demand. Then, combined with institutional investors’ commitment, the underwriter will narrow the offering to a firmer price.

As investment bankers receive orders at certain prices from institutional investors, they create a list of the orders, called the book of demand. From this list, investment bankers will justify and set a clearing price to ensure the entire offering is sold. Finally, the allocation of stocks or bonds will occur based on the subscription to the offering. In the case of an oversubscribed book, some investors may not receive the full order they requested.

The roadshow is often included as a part of the capital raising process. This is when the management of the company going public goes on the road with investment bankers to meet institutional investors who are – hopefully – going to be investing in their company. The roadshow is a great opportunity for management to convince investors of the strength of their business during the capital raising process.

These are some critical factors for a successful roadshow:

Investors are adamant that management structure and governance must be conducive in order to create profitable returns. For a successful roadshow, management must convey efficient oversight controls that exhibit streamlined business procedures and good governance.

Although risks aren’t positive, management must highlight and be upfront about the risks involved. Failure to report any key risks will only portray their inability to identify risks, hence demonstrating bad management. However, management should emphasize their hedging and risk management controls in place to address and mitigate the risks involved in carrying out their business.

Informing investors about the management’s tactical and strategic plans is crucial for investors to understand the company’s future growth trajectory. Will management be able to create sustainable growth? What are the growth strategies? Are they aggressive or conservative?

Again, although competition isn’t a positive factor, management must clearly address the issue with investors. When discussing key competitors, management should lead the conversation on how their competitive advantage is, or will be, superior to that of their competitors.

Why does the management need more cash? How, specifically, will the money be used?

Investors want to not only understand this company, but also the industry. Is it an emerging market? What is this company’s projected growth compared to that of the overall industry? Are the barriers to entry high or low?

Even though investment bankers devote substantial amounts of thought and time to pricing the issue, it is extremely challenging to predict the “right” price. Here are some key issues to consider in pricing.

After the offering is completed, investors do not want a lot of volatility. High levels of volatility will represent that the security was valued incorrectly or unreflective of the market’s demand or intrinsic value.

If there is to be any price volatility after the issue, hopefully, it will be to the upside. A strong post-issue performance indicates an underpriced offering.

If an offering attracts only a few highly concentrated investors, the probability of price volatility will be high. The deeper the investor base, the larger the investor pool, the more stable prices are likely to be.

Choosing the “right” price requires a tradeoff between achieving a strong aftermarket price performance and underpricing. Therefore, an investment banker should price the offering just low enough to support strong aftermarket performance, but not so low that the issuer feels it is substantially undervalued.

Underpricing an issue reduces the risk of an equity overhang and ensures a buoyant aftermarket. Then why wouldn’t underwriters want to underprice every time? In short, underpricing an offering is simply a transfer of surplus from the issuer to investors. The issuer will incur an opportunity cost from selling below its value, while investors will gain from buying an undervalued offering.

As banks are hired by the issuers, the underwriters must in good faith make the best decisions and returns for the issuer by correctly balancing the tradeoff.

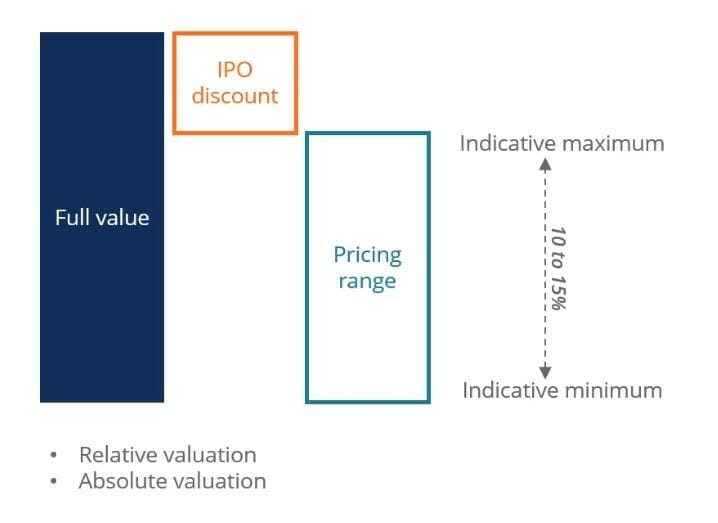

In order to price an IPO, banks must first determine the full value of the company. Valuation is done by a combination of Discounted Cash Flow (DCF), comparable companies, and precedent transactions analysis. For more information on business valuation and financial modeling, please see our financial modeling guide and financial modeling course.

Once investment bankers determine the value of the business through these financial models, they deduct an IPO discount. Hence, in IPOs, there is usually a discount on the intrinsic or full value of the business to price the offering. The full value minus the IPO discount gives a price range that investment bankers believe will attract institutional investors. Typically, 10%-15% is a normal range for the discount.

However, exceptions always exist. In the case of a heavily oversubscribed offering, the excess demand may offset the IPO discount. On the other hand, if the demand is lower than expected, it may be re-priced below the expected price range.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to the capital raising process. To learn more about corporate finance, check out the following free CFI resources: