Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

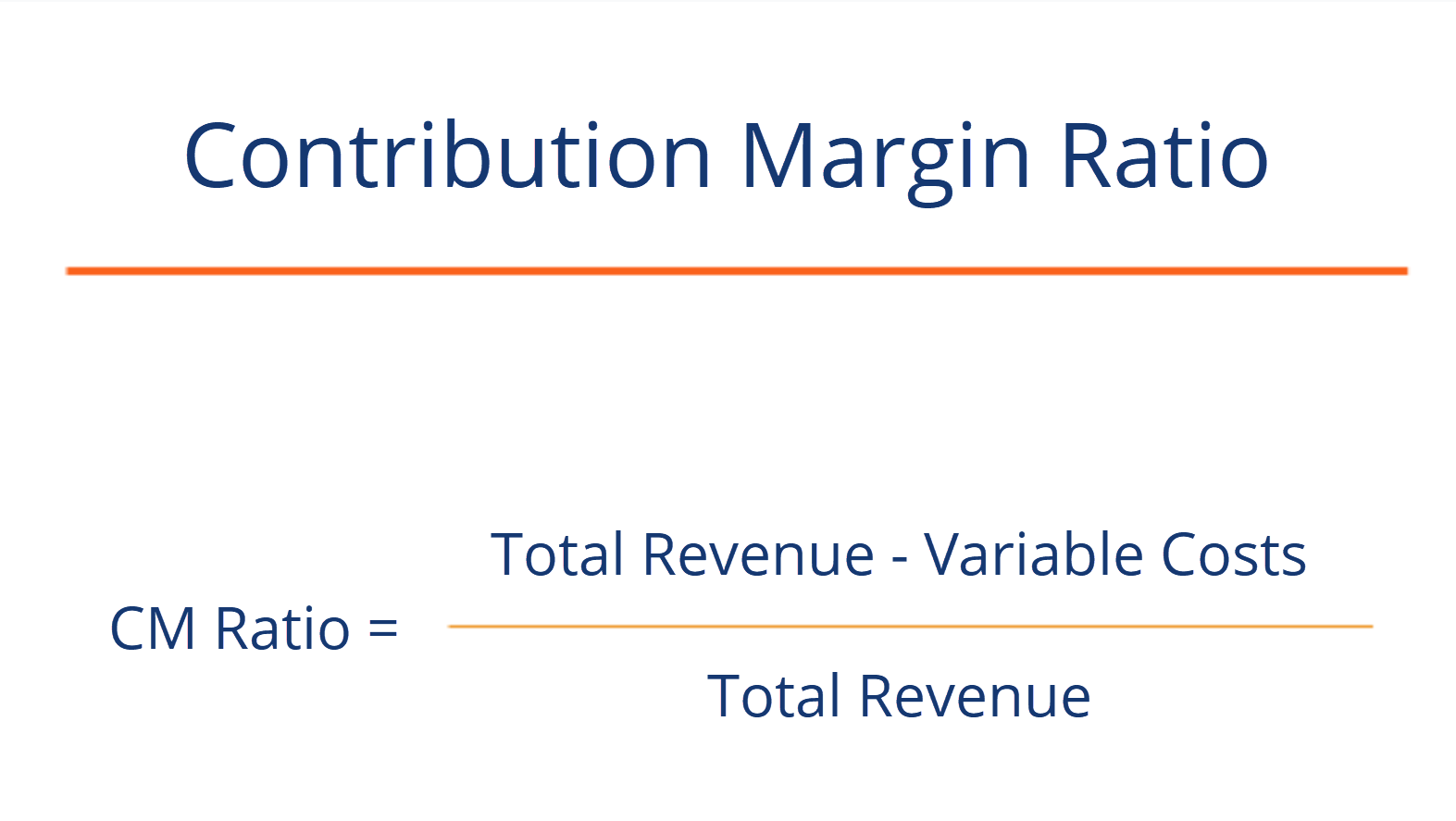

The formula to determine the contribution margin of a business

The contribution margin ratio (CM ratio) of a business is equal to its revenue less all variable costs, divided by its revenue. It represents the marginal benefit of producing one more unit. Here is the formula for the contribution margin ratio (CM ratio):

See an example in Excel here.

CM Ratio = (Total Revenue – Cost of Goods Sold – Any Other Variable Expenses) / Total Revenue

A company has revenues of $50 million, the cost of goods sold is $20 million, marketing is $5 million, product delivery fees are $5 million, and fixed costs are $10 million.

Contribution margin dollars = $50M – $20M – $5M – $5M = $20 million

Contribution margin ratio = $20M / $50M = 40%

The fixed costs of $10 million are not included in the formula; however, it is important to make sure the CM dollars are greater than the fixed costs, otherwise, the company is not profitable.

The contribution margin is not necessarily a good indication of economic benefit. Companies may have high fixed costs that need to be factored in.

It can be important to perform a breakeven analysis to determine how many units need to be sold, and at what price, in order for a company to break even. To learn more, check out our Financial Analysis course.

In order to perform this analysis, calculate the contribution margin per unit, then divide the fixed costs by this number, and you will know how many units you have to sell to break even.

Building on the above example, suppose that the company sold 1 million units. That means the CM per unit is $20. Fixed costs are $10 million, so the company has to sell 500,000 units to break even ($10 million / $20 per unit = 500,000).

Click the button below to download CFI’s free Contribution Margin Ratio Template!

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Contribution Margin Ratio. To learn more about other types of financial analysis, you may want to check out these additional CFI resources:

To find out more about finance careers, try out our interactive Career Map.