Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

Credit score

A FICO score, more commonly known as a credit score, is a three-digit number that is used to assess how likely a person is to repay the credit if the individual is given a credit card or if a lender loans them money.

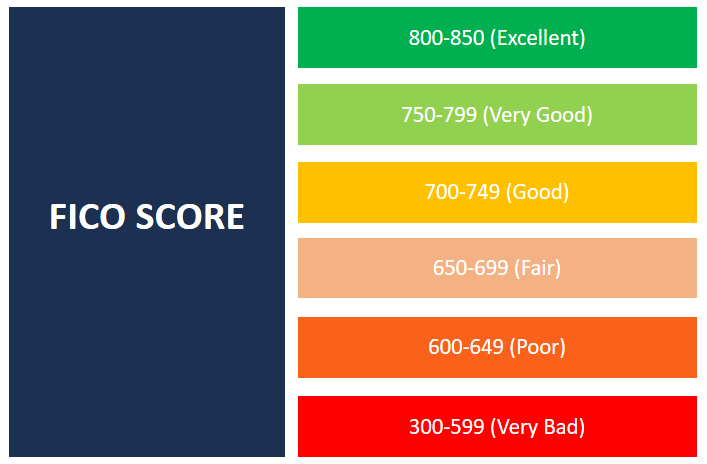

FICO scores are also used to help determine the interest rate on any credit extended to an individual. FICO scores range from 300 to 850 (worst to best).

The acronym FICO comes from the company that originally introduced such scores. Almost three decades ago, Fair Isaac Corporation established what is known today as the FICO score or credit score.

Ultimately, the score reflects a person’s worthiness to be given credit. The higher the credit score, the more likely the person is to repay their debts, and the lower the interest rate typically charged on any money lent to the individual.

FICO uses a formula they own the rights to, applying it to credit reports from three reporting agencies: Experian, TransUnion, and Equifax. The three credit bureaus monitor any loans or credit a person has received. They note how quickly the loans are repaid and take note of any issues with collecting payment.

In most cases, each bureau has varying information that is used to compile a FICO score. Using online sites to check for a FICO score typically involves compiling different scores to create one basic score.

There are a few things to consider when looking at a FICO score. Understanding what affects a credit score can help an individual borrow, spend, and repay debts more wisely.

The list of things that can and affect a credit score varies, however, there are a few basic aspects to pay close attention to. They include:

The record of your credit and how quickly you’ve paid loans off comprises about 35% of a FICO score. Late payments always cause a FICO score to go down. The longer it takes to make a payment, the bigger the impact on the score. Accounts sent to a collection agency or a filing for bankruptcy also significantly affect your score.

The length of time a person has had credit and the general age of each credit issuance account for about 15% of a FICO score.

The amount of available credit that a person uses makes up about 30% of the FICO score. A rule of thumb is to use no more than 30% of your available credit. Using less credit more often and repaying it quickly is a good way to boost your FICO score.

Having more than one line of credit that is consistently paid off is good. Having different types of credit – revolving credit such as a credit card and installment loans such as a mortgage or car loan – helps to improve your credit score.

Scores range from 300 (worst) to 850 (best).

An individual with a FICO score of 800 or above has an exceptional credit history. A person with a high credit score has likely had multiple lines of credit for many years. They haven’t exceeded any of their credit limits and have paid off all their debts in a timely manner.

FICO scores in the mid- to upper 700s are good scores. Individuals with a score in this range borrow and spend wisely and make timely payments. These individuals, like those in the 800+ range, tend to have an easier time getting credit and typically pay significantly lower interest rates.

The most common scores sit somewhere between 650 and 750. While the individual with a score in this range has fairly good credit, they might have had some late payments. These individuals typically don’t have a difficult time getting loans. However, they may have to pay slightly higher interest rates.

The last real range to consider is a score of 599 or lower. They are considered poor credit scores and usually result from multiple late payments, failure to pay off debts, or debts that have gone to collections agencies. Individuals with such FICO scores often find it difficult – if not impossible – to get any form of credit.

The key for any individual looking for a good FICO score is to establish lines of credit, use them in small or measured amounts, and pay them off quickly. Having a good score is important, especially for individuals looking to take out major loans such as an auto loan a home mortgage.

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA®) certification program, designed to help anyone become a world-class financial analyst. To learn more, check out the following CFI resources: