Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The difference between interest revenues and interest expenses

Net interest income is the difference between interest revenue and interest expense.

For financial institutions, interest revenues represent the interest payments the bank receives on their interest-bearing assets, while interest expenses are the cost of servicing interest payments to customers on their deposits.

Interest is defined as the difference between the purchase price and the sale price. If interest rates in the economy drop and Treasury bills are sold before maturity, a capital gain will arise.

Indexed securities offer an interest rate at a discount to the market rate, and the payable balance is adjusted at maturity for inflation.

At maturity, if the adjustment is positive, it is included in interest income. If the adjustment is negative, it will be deductible, given the satisfaction of the criterion for interest rate deductibility.

Hybrid financial products offer a guaranteed return on a pre-determined date based on the movement of a pre-specified market index, paid at maturity. Often, there are covenants, such as maximum interest, minimum interest, and exercise period, attached to the financial products.

For many financial institutions, the net interest margin is a primary source of income. The banks’ net interest margin can be interpreted as the cost of financial intermediation. Therefore, it is the difference between what borrowers pay for their loans and what they receive from lending.

Simply put, banks are risk-averse middlemen between depositors and borrowers of funds. Banks offer the following common financial products:

Interest revenue is generated through interest payments that the bank receives on outstanding loans. It is made up of credit lines and loans that the institution has on its balance sheet.

Interest revenue is calculated through the application of the effective interest rate to the gross carrying amount of the financial assets. There are only two exceptions in this calculation:

Where:

Interest expense is the price that the lender charges the borrower in a financing transaction or the cost of borrowing money. It is the interest that accumulates on outstanding liabilities. Common examples include customer deposits and wholesale financing.

To calculate the interest expense, multiply the effective interest rate by the gross carrying amount of financial liabilities.

Net interest margin refers to the difference between the interest income generated and the amount of interest paid out to lenders. It is an industry-specific profitability ratio for banks and other financial institutions that lend out interest-earning assets.

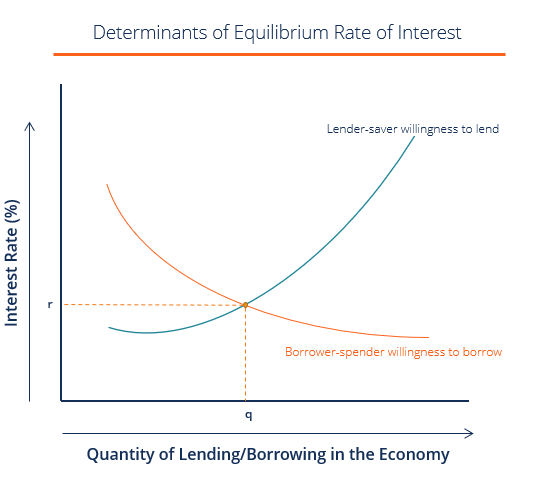

The equilibrium interest rate is primarily impacted by the demand for borrowing capital and the supply of capital that is being lent. Increasing interest rates benefit banks by increasing their net interest income.

Therefore, in periods of low interest rates, banks have lower net interest margins. Generally, a positive net interest margin is indicative of a bank that efficiently invests its capital, whereas a negative net interest margin signifies inefficiency.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA®) certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: