Net Interest Margin

The difference between the interest income generated and the amount of interest paid out to lenders

What is Net Interest Margin?

Financial intermediaries in the economy deal extensively with borrowing and lending, and the net interest margin is the net benefit of lending.

Net interest margin is the difference between the interest income generated and the amount of interest paid out to lenders. It is an industry-specific profitability ratio for banks and other financial institutions that lend out interest-earning assets.

Summary

- Net interest margin is a measure of profitability for banks and financial institutions. It refers to the difference between interest received and interest paid.

- Interest rates in the economy significantly affect the financial net interest margin.

- A positive net interest margin indicates that the bank is efficiently investing, whereas a negative net interest margin implies inefficient investing.

Net Interest Margin Formula

Interest Revenue

Interest revenue is generated through interest payments the bank receives on outstanding loans. It is made up of credit lines and loans on the financial institution’s balance sheet.

Interest Expense

Interest expense is the price the lender charges the borrower in a financing transaction. It is the cost of borrowing money. It is the interest that accumulates on outstanding liabilities. Common examples include customer deposits and wholesale financing.

Average Earning Assets

A company’s earning assets are investments that produce income without any significant effort on its owner’s part. Some popular earning assets are stocks, bonds, certificates of deposits, notes, etc.

To calculate the average earning assets, simply take the average of the beginning and ending asset balance.

Negative Net Interest Margin Example

Over the fiscal year, Bank A collected $4 million in interest from its clients. In the same period, Bank A needed to pay $8 million in interest to a reinsurance company. Bank A’s average earning assets in the fiscal year was $20 million.

A net interest margin of -20% indicates that Bank A is losing more money than it is making on its own investments. Therefore, Bank A’s capital was used inefficiently.

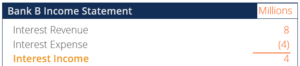

Positive Net Interest Margin Example

Over the fiscal year, Bank B collected $8 million in interest from its clients. In the same period, Bank B needed to pay $4 million in interest to a reinsurance company. Bank B’s average earning assets in the fiscal year was $20 million.

A net interest margin of 20% indicates that Bank B is earning more money from receiving interest payments than paying interest. Therefore, Bank B’s capital was used efficiently.

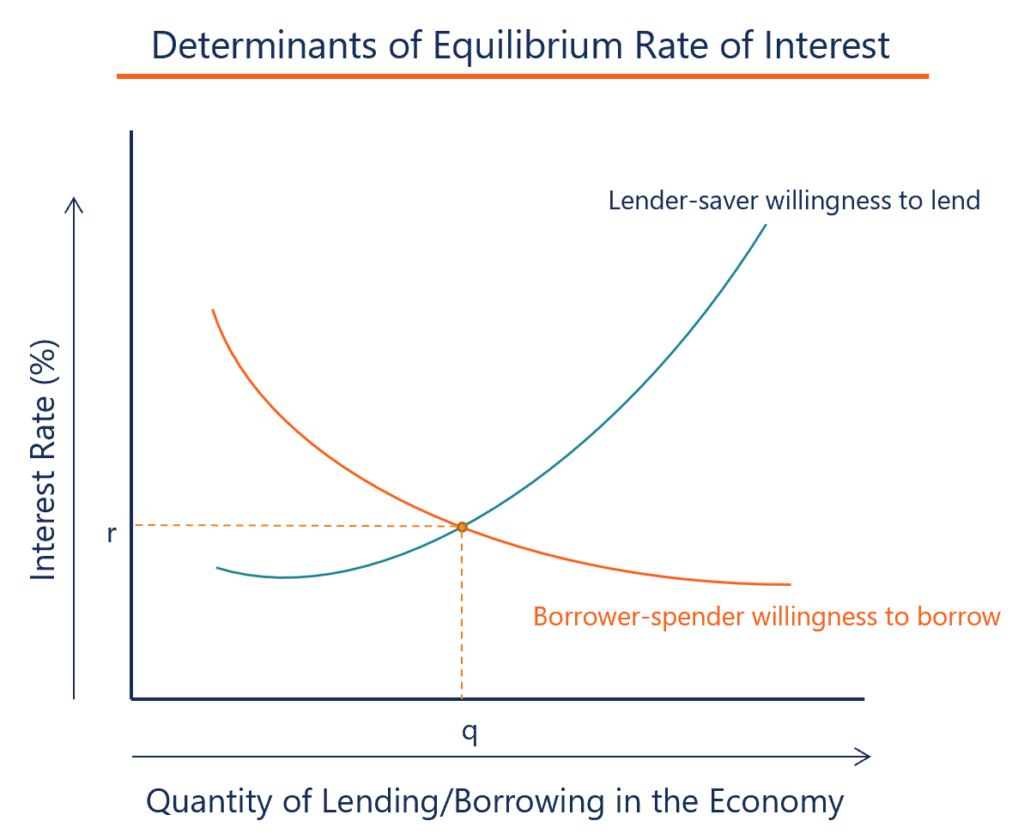

Interest Rates in the Economy and the Net Interest Margin

The net interest margin of financial intermediaries is directly related to interest rates in the economy. Interest rates in the economy move according to the economy’s business cycle. A major factor in the net interest margin is whether there is a greater demand for borrowing or saving.

Low Interest Rates

Low interest rates in the economy lead to greater net interest margins for financial intermediaries. When market interest rates fall, the funding costs of banks rapidly fall relative to their interest income, and ultimately, net interest income increases.

When interest rates fall, the demand for loans increases, and the supply of deposits decreases. It drives the volume of larger lending amounts and lower deposit volumes, therefore improving interest income. Ultimately, net interest margins will drastically increase and gradually decline over time.

High Interest Rates

High interest rates in the economy lead to smaller net interest margins for financial intermediaries. When market interest rates increase, the banks’ funding costs rapidly increase relative to their interest income and will reduce net interest income.

When interest rates rise, the demand for savings accounts increases relative to loans, and the net interest margin decreases. It is because the bank will have greater interest payments than interest receivable.

Net Interest Spread vs. Net Interest Margin

Net interest spread is the nominal average between borrowing and lending rates. However, it fails to consider that earning assets and the funds borrowed may be different in terms of instrument composition and volume. Alternatively, the net interest margin is a profitability metric that contrasts a bank’s interest earnings with its payments to customers.

More Resources

CFI is the official provider of the Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below:

Analyst Certification FMVA® Program

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

Additional Questions & Answers

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover:

- What is Financial Modeling?

- How Do You Build a DCF Model?

- What is Sensitivity Analysis?

- How Do You Value a Business?

Accounting Crash Courses

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.