Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

Demonstrates the Relationship Between European Put and Call Options

Put-call parity is an important concept in options pricing which shows how the prices of puts, calls, and the underlying asset must be consistent with one another. This equation establishes a relationship between the price of a call and put option which have the same underlying asset. For this relationship to work, the call and put option must have an identical expiration date and strike price.

The put-call parity relationship shows that a portfolio consisting of a long call option and a short put option should be equal to a forward contract with the same underlying asset, expiration, and strike price. This equation can be rearranged to show several alternative ways of viewing this relationship.

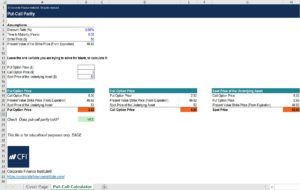

Below, we will go through an example question involving the put-call parity relationship. This can easily be done with Excel.

To better understand the put-call parity theory, let us consider a hypothetical situation where you buy a call option for $10 with a strike price of $100 and maturity date of one year, as well as sell a put option for $10 with an identical strike price and expiration. According to the put-call parity, that would be equivalent to buying the underlying asset and borrowing an amount equal to the strike price discounted to today. The spot price of the asset is $100 and we make the assumption that at the end of the year the price is $110 – so, does the put-call parity hold?

If the price goes up to $110, you would exercise the call option. You paid $10 for it but you can buy the asset at the strike price of $100 and sell it for $110, so you net $0. You have also sold the put option. Since the asset has increased in market value, the put option will not be exercised by the buyer and you pocket the $10. That leaves you with $10 from this portfolio.

What is the portfolio consisting of the underlying asset and short position on the strike price worth at the expiration date? Well, if you had invested in the asset at the spot price of $100 and it ended at $110, and you had to pay back the strike price at maturity from the amount you borrowed which would be $100, the net amount would be $10. We see that these two portfolios both net to positive $10 and the put-call parity holds.

The put-call parity theory is important to understand because this relationship must hold in theory. With European put and calls, if this relationship does not hold, then that leaves an opportunity for arbitrage. Rearranging this formula, we can solve for any of the components of the equation. This allows us to create a synthetic call or put option. If a portfolio of the synthetic option costs less than the actual option, based on put-call parity, a trader could employ an arbitrage strategy to profit.

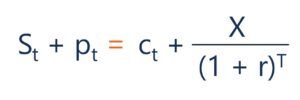

As mentioned above, the put-call parity equation can be written a number of different ways and rearranged to make varying inferences. A couple of common ways it is expressed are as follows:

St + pt = ct + X/(1 + r)^T

The above equation shown in this combination can be interpreted as a portfolio holding a long position in the underlying asset and a put option should equal a portfolio holding a long position in the call option and the strike price. According to the put-call parity this relationship should hold or else an opportunity for arbitrage would exist.

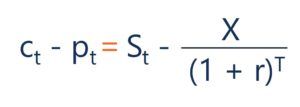

ct – pt = St – X/(1 + r)^T

In this version of the put-call parity, a portfolio that holds a long position in the call, and a short position in the put should equal a portfolio consisting of a long position in the underlying asset and a short position of the strike price.

For the above equations, the variables can be interpreted as:

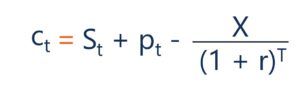

The equation can also be rearranged and solved for a specific component. For example, based on the put-call parity, a synthetic call option can be created. The following shows a synthetic call option:

ct = St + pt – X/(1 + r)^T

Here we can see that the call option should be equal to a portfolio with a long position on the underlying asset, a long position on the put option and a short position on the strike price. This portfolio can be thought of as a synthetic call option. If this relationship doesn’t hold, then an arbitrage opportunity exists. If the synthetic call was less than the call option, then you could buy the synthetic call and sell the actual call option to profit.

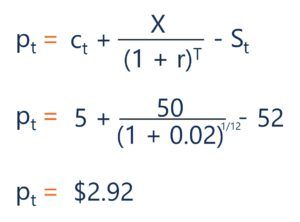

Let us now consider a question involving the put-call parity. Suppose a European call option on a barrel of crude oil with a strike price of $50 and a maturity of one-month, trades for $5. What is the price of the put premium with identical strike price and time until expiration, if the one-month risk-free rate is 2% and the spot price of the underlying asset is $52?

Here we can see the calculation that would be used to find the put premium:

These calculations can also be done in Excel. The following shows the solution to the above question done in excel:

If you would like to learn more about financial modeling, check out CFI’s Financial Modeling Courses!

Thank you for reading CFI’s guide on Put-Call Parity. To keep advancing your career, the additional CFI resources below will be useful: