Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

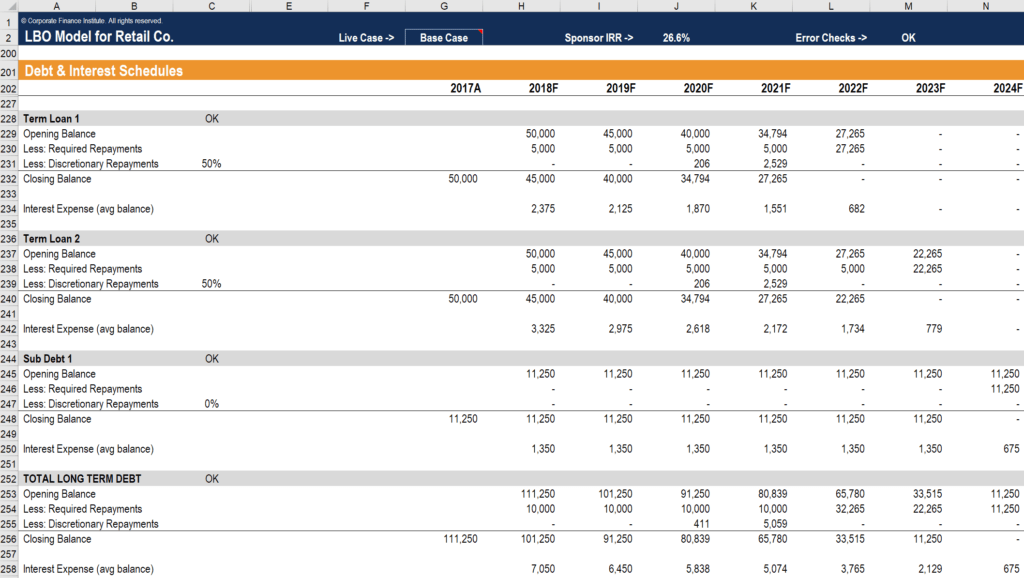

A repayment schedule of debt in Excel

A debt schedule lays out all of the debt a business has in a schedule based on its maturity. It is typically used by businesses to construct a cash flow analysis. As shown in the graphic below, interest expense in the debt schedule flows into the income statement, the closing debt balance flows onto the balance sheet, and principal repayments flow through the cash flow statement (financing activities).

The debt schedule is one of the supporting schedules that ties together the three financial statements.

The interest expense calculated above (row 258) flows onto the income statement as interest expense. The closing balance (row 256) flows onto the balance sheet as the total debt value, under liabilities. In this example, interest expense is based on a fixed interest rate multiplied by the average debt balance for the period (opening plus closing, divided by two). The example above is from CFI’s LBO Financial Modeling Course.

When building a financial model, an analyst will almost always have to build a supporting schedule in Excel that outlines debt and interest.

Components of this schedule include:

The above items allow the debt to be tracked until maturity. The closing balance from the schedule flows back to the balance sheet, and the interest expense flows to the income statement.

To construct a debt schedule, analysts need to list all debt currently outstanding by the business. The types of debt include:

Before committing to borrow money, a company needs to carefully consider its ability to repay debt and the real cost of the debt. Here is a list of the factors a company needs to consider:

The ability to estimate the total amount a company needs to pay once a debt matures is the main reason a debt schedule is made. Another reason for using a debt schedule includes the company’s ability to monitor the maturity of the debt and make decisions based on it, such as the possibility of refinancing the debt through a different institution/ source when the interest rate declines.

The debt schedule report can be used as an instrument to negotiate a new line of credit for the company. Lenders will use the report and consider the risk/reward before granting new credit.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: