Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

The cash required to pay back interest and principal on debt obligations

Debt service refers to the total cash required by a company or individual to pay back all debt obligations. To service debt, the interest and principal on loans and bonds must be paid on time. Businesses may need to repay bonds, term loans, or working capital loans.

In some cases, lenders may require companies to hold a debt service reserve account (DSRA). The DSRA can act as a safety measure for lenders to ensure that the company’s future payments will be met. Individuals may need to service debts such as mortgage, credit card debt, or student loans. The ability to service debt for both companies and individuals will impact their options to receive additional debt in the future.

Funding is critical for any business venture. A popular way to acquire such funding is through borrowing money, but obtaining debt is not always an easy task. The lender – whether it be a bank, lending institution, or investor – must have faith that the borrower will be able to repay the loan before extending one. Hence, debt servicing capacity is a key indicator of the trustworthiness of a company.

A company that consistently services its debts will have a good credit score, which will boost its reputation for other lenders. It will be important for future ventures that require additional funding. Therefore, a finance manager should ensure a company maintains its debt servicing capability.

Individuals must also focus on debt servicing by managing their personal finances. By consistently servicing their debts, they can also build a good credit score. Ultimately, a good credit score will improve their chances of getting a mortgage or car loan, or increasing a credit card limit.

Debt service is determined by calculating the periodic interest and principal payments due on a loan. Doing so requires knowledge of the loan’s interest rate and repayment schedule. Calculating debt service is important to determine the cash flow required to cover payments. Hence, it is useful to calculate annual debt service, which can then be compared against a company’s annual net operating income.

For example, a company sells a bond with a face value of $500,000 at an interest rate of 5%. Suppose the company agreed to pay interest at the end of every year, and at the end of seven years, it will pay back the face value of the bond. In such a case, the annual debt service for the first year will be:

$500,000 x 0.05 = $25,000

At the end of the seventh year, the annual debt service will equal:

($500,000 x 0.05) + $500,000 = $525,000

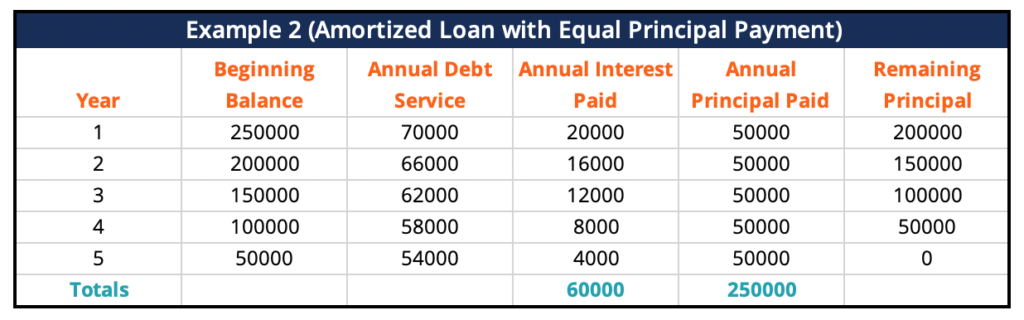

In a second example, a company takes on a $250,000 loan at an interest rate of 8% for a term of five years. Suppose it is an amortized loan with equal principal payments. It means that the company will repay an equal amount of principal each period, plus 8% interest on the outstanding principal.

At the end of the five-year period, it will have repaid all the principal in addition to the interest. If the terms of payment were one installment a year, the first year’s debt servicing amount would be $70,000. The second year’s debt servicing amount would be $66,000, then $62,000, $58,000, and finally $54,000 in the final year.

A business needs to compute its debt service coverage ratio (DSCR) before it begins borrowing. The DSCR is critical to measuring the company’s ability to make debt payments on time. The ratio divides the company’s net income with the total amount of interest and principal it must pay. The higher the ratio, the easier for the company to obtain a loan.

The formula for calculating the DSCR is as follows:

DSCR = Annual Net Operating Income / Annual Debt Payments

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful: