Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Deal Summary and Cash Flow Model

A real estate development model usually consists of two sections: the Deal Summary and the Cash Flow Model. Within the Deal Summary, all important assumptions – including the schedule (which lays out the timeline), property stats, development costs, financing assumptions, and sales assumptions – are listed and used to calculate the economics and profitability of the project.

The Cash Flow Model begins with the revenue build up, monthly expenses, financing, and finally levered free cash flows, NPV (net present value), and IRR (internal rate of return) of the project. In the following sections, we will go through the key steps to building a well-organized real estate development model.

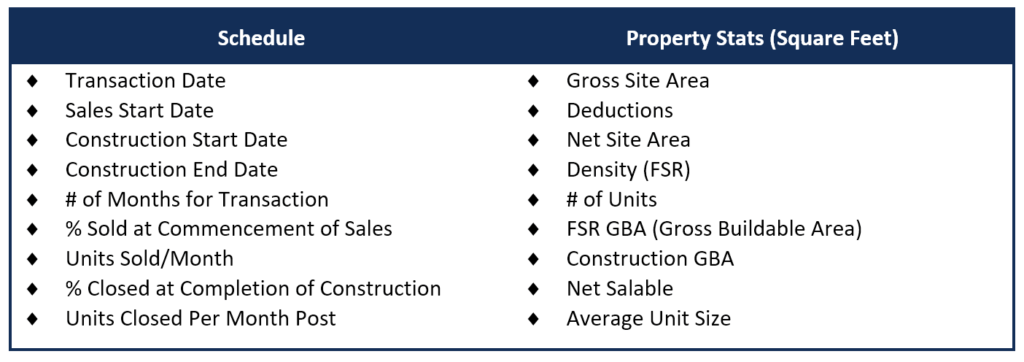

The first step in building a real estate development model is to fill in the assumptions for schedule and property stats. Here is a list of items that should be included:

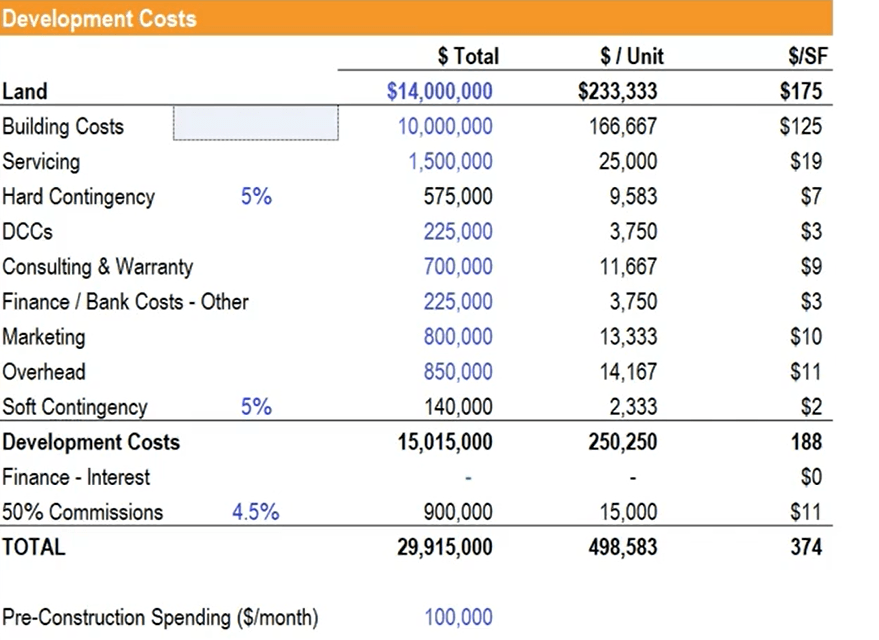

For the next step in creating a real estate development model, we will input the assumptions for development costs in terms of the total amount, cost per unit, and cost per square foot. Development costs might include land cost, building costs, servicing, hard and soft contingency, marketing, etc. Using the property stats filled in earlier, we can calculate all the numbers and complete the development costs section. The section should look something like this:

Image Source: CFI’s Real Estate Financial Modeling Course.

In sales assumptions, we will calculate the total revenue from this project. Suppose market research is done and based on comparables, we believe that $500 per square foot is a realistic starting point for the sales price. We will then use this as the driver for revenue. After calculating sales (total, $/unit, $/SF), sales commissions (e.g., 50%), and warranty, we can figure out the net proceeds from this project.

For financing, there are three critical assumptions: loan-to-cost percentage, interest rate, and land loan.

Before calculating the total loan amount, we need to figure out the total development cost amount. Since we have not yet calculated the interest expense, we can link the cell to the cash flow model for now and obtain the value once the cash flow model is filled in. The commissions are the same as the sales commissions in the sales assumptions section. The total development costs can be calculated as:

Now we can fill in the rest of the financing assumptions.

Image Source: CFI’s Real Estate Development Model Course.

The figures above will be the assumptions from the Deal Summary section. Once we complete the Cash Flow Model, we will come back and complete the Development Pro Forma section and add a sensitivity analysis.

The first step in calculating revenues is to find out the townhome absorption and closings. Absorption is the number of available homes being sold during a given time period, while closings are the number of homes closed once the construction is complete.

Now we can build up the revenue using the absorption and closings information.

(*Note that commissions and warranty are in negative amounts.)

Now we’ll find out the development expenses, which include land acquisition cost, pre-construction spending, and construction spending. The numbers can be found in the development costs assumption section from the Deal Summary.

The Cost to Fund is the shortfall in the project cash flow that needs to be financed. When the total net revenue is less than the total development costs, there is a negative cash flow that we need to cover.

When total net revenue becomes greater than the total development costs, there will be positive proceeds that we can use to pay back borrowed capital. We can use the following formulas to calculate the two numbers:

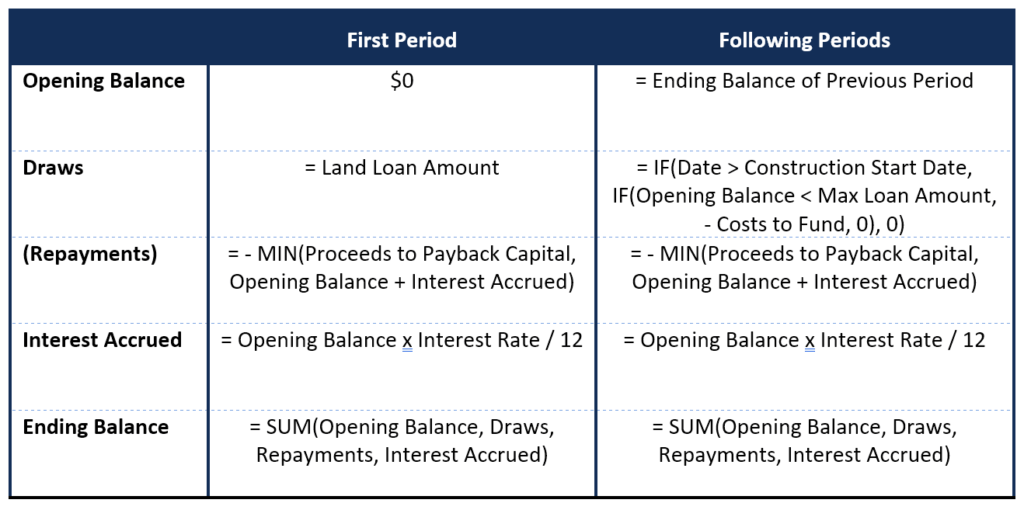

Next, we calculate the loan balances, draws, repayments, and interest accrued. The table below summarizes the calculations for the first period and the following periods:

We should also perform a quick sanity check to ensure none of the ending balances exceeds the max loan amount.

We can now calculate the levered free cash flows and resulting IRR of this project.

Equity Balance is simply the cumulative FCF:

Finally, using the XIRR formula, we can calculate the Levered IRR for this project:

Image Source: CFI’s Real Estate Financial Modeling Course.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Real Estate Development Model. To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below: