Cliff Vesting

An employee's right to full (retirement) benefits after a specified period

What is Cliff Vesting?

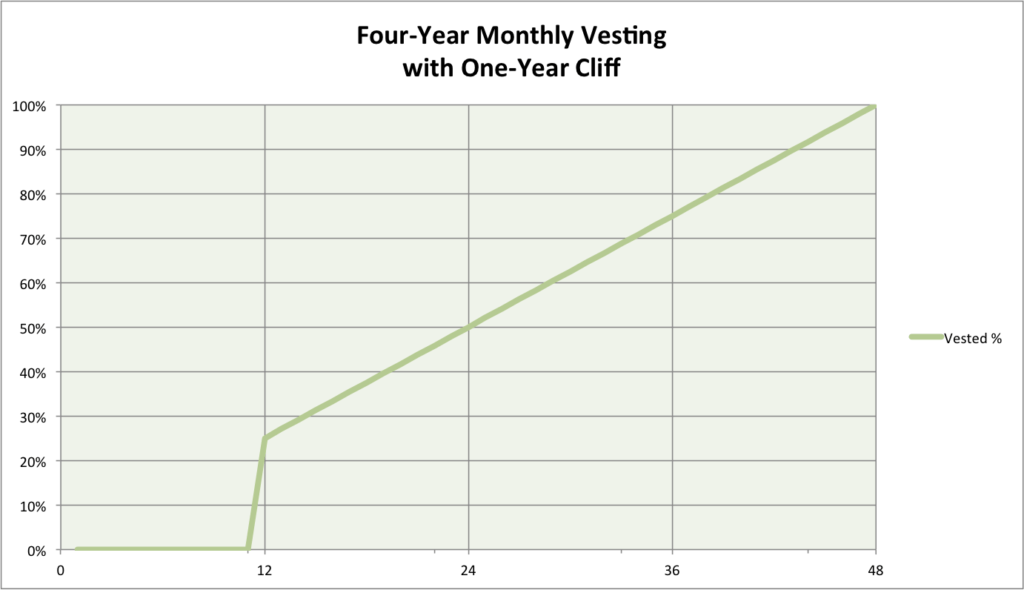

Cliff Vesting is a process where employees are entitled to the full benefits from their firm’s qualified retirement plans and pension policies on a given date, as opposed to retirement plans where the employee’s ownership of the funds vests gradually. In most cases, there is usually a four-year vesting schedule plan with a one-year cliff. Upon completing the cliff period, the employee receives full benefits, compared to a vesting schedule plan where the amount is released over a scheduled period.

Company Benefits and Cliff Vesting

A company that engages an employee can provide various benefits to the employee. The benefits range from pensions to retirement plans such as a 401(k) or 403(b), assets, or any other specified benefit. A vesting plan must meet the minimum vesting standards that the IRS stipulates.

An acceptable agreement enables the employer to maintain a cordial relationship with the employee while rewarding loyalty. Such a scenario creates a win-win situation for both the employee and the employer. The employee gets a promise of getting some incentives after a given period, while the employer’s targets are met and graded on a quantifiable scale. To achieve such high standards, the staff must demonstrate a genuine commitment, and the company, in return, must show constant support of employees.

Example (Cliff Vesting)

Suppose Joe enters into a cliff vesting plan with his employer. He, therefore, accepts a four-year contract with the company. In return, the company promises him 2,400 units on successful completion of the first year. Then, the rest of the units will follow the vesting schedule plan of 50 units per year. Joe is satisfied, signs the contract, and sweats through the first year. However, on the 11th month – almost through – the management decides, well, Joe is a hardworking employee but it seems he is not channeling enough energy toward the organization’s vision. So, they fire Joe on Friday evening – one week before his first-year anniversary. The result is that Joe loses all benefits he is entitled to because the cliff vesting period is incomplete.

How Vesting Schedules Work

The process of vesting schedules is locked inside the bubble of irrevocable rights over employer incentives during the duration of the employee’s tenure with the company. Vesting rights may include stock or contributions made by the employer to the employee’s retirement plan account or pension plan on a scheduled basis.

Example (Vesting Schedules)

Company A employs a high-valued worker named Joe, and the company plans to retain him. To achieve this, the company must offer him an incentive to continue to provide his undeniably valuable contributions to the company’s success. The company may decide to give Joe 2,400 restricted stock units on sign-up. Joe will also receive 1/48th of his principal for the next four years as gratitude for his continuous support. Therefore, he will receive 50 units in the second, third, and fourth years. However, if Joe decides to retire from the company in the wake of his third year, he will only get the accumulated second’s year 50 units. The company will retain the remaining 100 units.

This arrangement doesn’t mean that when Joe is fully vested, he will withdraw his amount immediately. The contract is subject to regulations regarding withdrawals and other factors.

Importance of Cliff Vesting

For a startup company, cliff vesting provides a provision to offer vested benefits to its valuable employees. At the same time, the system allows time to vet staff before fully committing them into the system. It represents a gesture showing that the company is attaching value to its employees by giving back a token of the profits they’ve labored hard for – a substantial retirement benefit to start a new life or a pension plan to shine a bright sun ray to old age. Such a scenario offers irrefutable value to both stakeholders – the company and the employee.

In the event of stock ownership, however, litigation processes can pose significant challenges in the long run. This is true when it comes to a company’s liquidation, compensation, or the retirement of some high-value employees.

Why Cliff Vesting Sometimes Faces Rejection

To a new employee, unfortunately, cliff vesting can sometimes seem to pose a threat. In the event one enters into an arrangement of cliff vesting, there are two possibilities. Either a contract termination just before the anniversary, which means lost energy, a lost investment, or a lost dream, or an auspicious anniversary, which means energy well spent, a profitable venture, or a dream realized.

In other circumstances, such as in the event there is a transition of management either due to hostile takeovers or a company buyout, the cliff may not be applicable. New management may come in with a new agreement, replacing the original deal or abolishing it altogether.

Difference Between Defined Benefit and Defined Contributions Plans

Once the employee becomes vested, the policies may differ, depending on the employer, because different companies have different retirement plan offers for their employees. They include:

1. Defined Benefit Plan

A defined benefit plan, such as a pension, is one where the employer provides all the money for the plan. The employer must pay a former employee a specific amount of benefit each year. The amount depends on the employee’s final year salary, the employee’s period of service to the company, and possibly other factors that must be stated in the original arrangement.

2. Defined Contributions Plan

In this type of plan, such as a 401(k), the employee contributes a set amount of money to the plan while working, such as 10% of their weekly salary. The employer may or may not provide matching contributions. The payout varies based on the performance of the investments that the employee chooses, usually one or more of a number of mutual funds offered through the plan.

Other Resources

Thank you for reading CFI’s guide to cliff vesting. To learn more, see the following resources and check out CFI’s official global Financial Modeling & Valuation Analyst certification program, designed to help anyone become a world-class financial analyst.

Analyst Certification FMVA® Program

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

Additional Questions & Answers

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover:

- What is Financial Modeling?

- How Do You Build a DCF Model?

- What is Sensitivity Analysis?

- How Do You Value a Business?

Accounting Crash Courses

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.