Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

The analysis of fixed income security price fluctuations to changes to the market interest rate

Interest rate sensitivity is the analysis of fixed income security price fluctuations to changes in the market interest rate. The higher the security’s interest rate sensitivity, the greater the price fluctuations.

Fixed income is one of the major asset classes available to investors. Investors profit from fixed income through the interest (coupon) rate and price appreciation. Fixed income coupon payments are fixed over the life of the security, while price fluctuations are a direct outcome of market interest rate changes.

Fixed income securities are created and initially sold on the primary market. Next, investors can choose to hold the fixed income security until maturity or resell it on the secondary market. Fixed income price is negatively correlated with the market interest rate – this is known as interest rate risk.

At issuance, coupon bonds are sold at par value based on the prevailing market interest rate. Once the bond is issued, the coupon payments are fixed over the life of the loan, but the market interest rate fluctuates continuously.

When the market interest rate increases, the outstanding fixed-income security prices depreciate because newly issued fixed-income securities will pay higher coupon payments. Vice versa, if the market interest rate decreases, the outstanding fixed income prices appreciate because its coupon payments are higher than newly issued fixed income securities.

Therefore, understanding interest rate sensitivity becomes an important consideration in selecting fixed-income securities. Certain characteristics affect a security’s interest rate sensitivity, such as:

The longer the maturity is, the higher the security’s interest rate sensitivity. This is because longer-term securities have higher exposure to interest rate risk.

The lower the coupon rate, the higher the security’s interest rate sensitivity because it will have higher interest rate risk.

To measure interest rate sensitivity, duration is a great metric because it takes such characteristics into consideration. The general rule of thumb is the higher the duration, the higher the interest rate sensitivity. The three most common types of duration are:

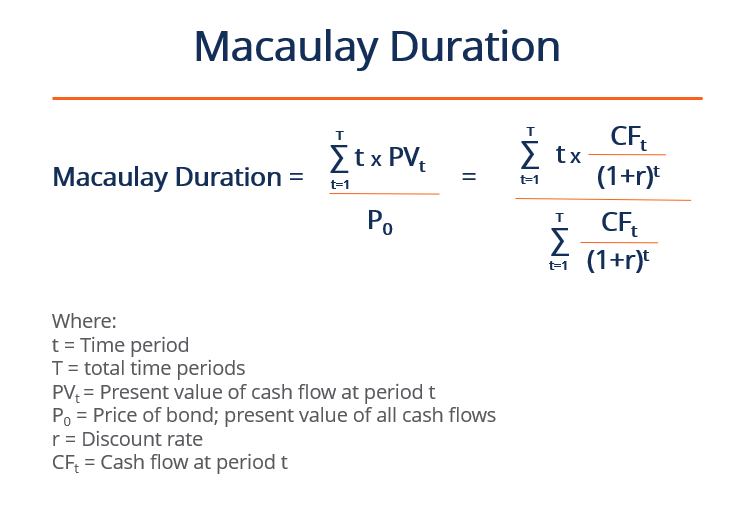

The Macaulay duration represents the length of time the investor must hold the security until its total cash flows can repay the bond’s price. For coupon-paying bonds, the Macaulay duration is always shorter than its time to maturity. With zero-coupon bonds (bonds without coupon payments that are sold at a discount), the Macaulay duration is equal to its time to maturity.

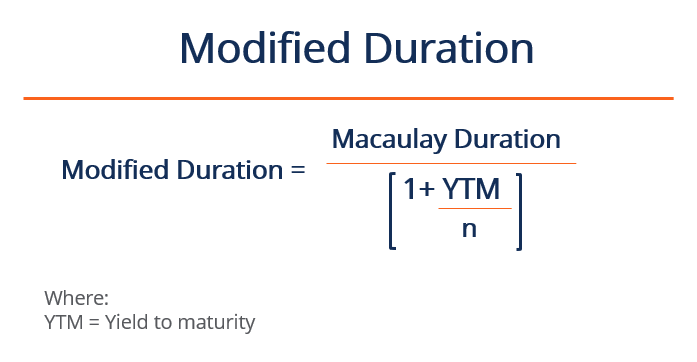

The Modified duration builds on the Macaulay duration by integrating the yield to maturity. It represents the percentage change in bond price in relation to the percentage change in the interest rate.

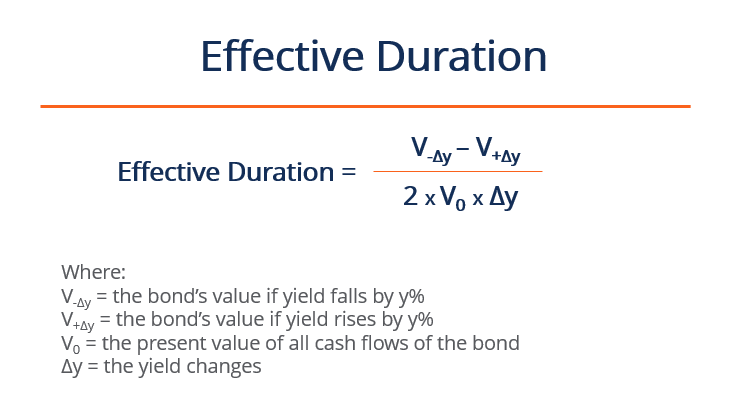

The effective duration is applied specifically to bonds with embedded options to account for its uncertainty of future cash flows. The effective duration serves as the percentage change in price relative to the percentage change in yield to maturity.

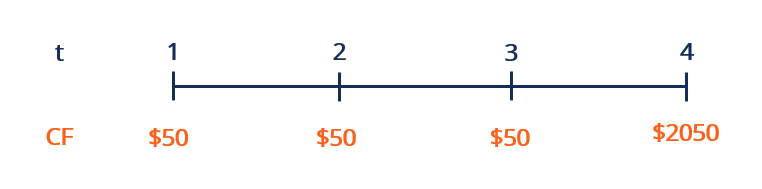

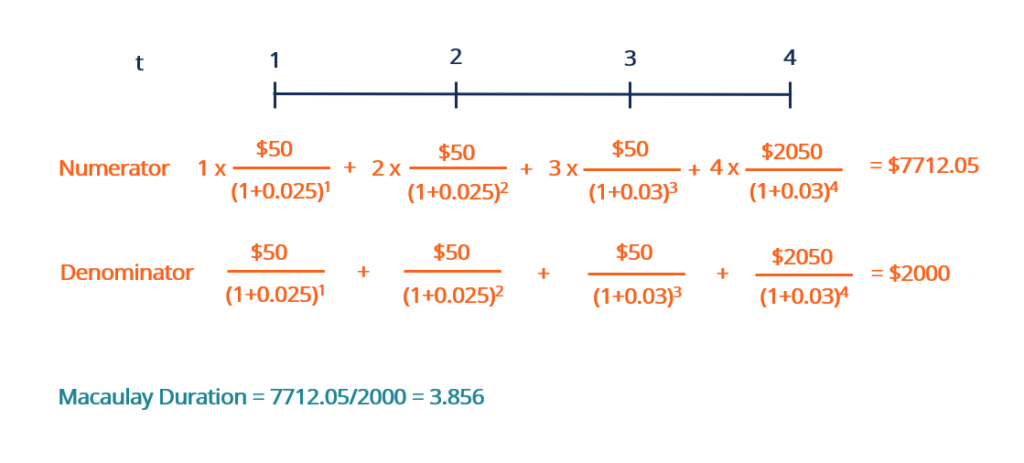

Suppose an investor purchases a $2,000 par value bond with a 2.5% coupon rate compounded annually. The maturity date is four years from today, on which the principal $2,000 will be returned. What is the Macaulay duration of the bond?

While the formula may look intimidating, the numerator and the denominator are almost identical, except each cash flow in the numerator is multiplied by its respective time period t. For the discount rate r, we are using the coupon rate of the bond.

With the numerator and denominator solved, we put those together to get a Macaulay duration of 3.856. It means that it will take approximately 3.856 years of holding the bond for its cash flows to cover its price. Because the bond pays coupon payments, the Macaulay duration is shorter than its time to maturity of four years.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI offers the Capital Markets & Securities Analyst (CMSA)® certification program for those looking to take their careers to the next level. To keep learning and advance your career, the following resources will be helpful: