Negative Gearing

Occurs when an investment that is made using borrowed funds produces cash flows that are lower than the interest and other expenses

What is Negative Gearing?

Negative gearing occurs when an investment that is made using borrowed funds produces cash flows that are lower than the interest and other expenses paid towards that investment.

Summary

- Negative gearing occurs when an investment that is made using borrowed funds produces cash flows that are lower than the interest and other expenses paid towards that investment.

- A benefit of negative gearing is that any value of net loss can be offset against any other income that will be taxable.

- Negative gearing is mostly beneficial for individuals who are earning high income and are in a larger tax bracket, which will allow them to reap the tax benefit.

Understanding Negative Gearing

The concept can be explained using the figure below:

Normally, negative gearing is seen in the real estate market where properties are rented. For a person who bought the property and leased it out to a tenant, the biggest expense he faces is the interest on the loan to buy the property.

Other expenses are also incurred, which can be in the form of maintenance fees, repairs, and property taxes. The cash flow from the property is the rental income received from the tenant.

Positive Gearing

The term gearing is often used when money is borrowed to invest in an asset, typically an investment property. The income that yields from the investment can be either positively or negatively geared.

Positive gearing is when the return you get from the investment (rental income) is greater than the interest paid on the borrowed amount and other expenses related to the property.

Normally, the income derived from positive gearing can be used to meet future repayments or investment purposes.

Tax Implications of Negative Gearing

Negative gearing can be triggered by several factors. One possibility is if you are in a high-interest-rate environment and rental payments are not sufficient to cover your expenses.

Another situation can be when the loss is magnified by the depreciation of the property or any capital expenditure related to the property. Since both are tax-deductible, it can result in negative gearing as well.

A benefit of negative gearing is that any value of net loss can be offset against any other income that will be taxable. For example, if the income you earn is taxed at a rate of 30%, each dollar contributing towards negative gearing loss will help you save $0.30.

There are also certain downsides to negative gearing. The tax benefits are normally advantageous for individuals who earn a high income. If someone is earning and paying little or no tax, having negative gearing on your investment property will not make a big difference.

Negative gearing can also inflate the value of the property if expenses are not controlled in an orderly fashion – rental payments may be increased, leading them to be higher than the market rental yield.

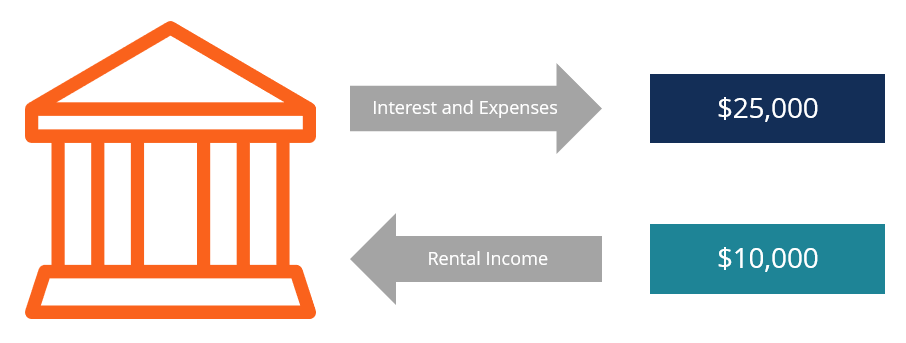

Negative Gearing Example

Suppose a person named Bob buys a property for investment purposes by taking a loan from the bank. He rents that property to his friend and receives a rental income of $10,000 per annum.

Bob pays interest on the bank loan and bears the expenses related to the investment property. The total annual amount of interest and expenses is $25,000. In this case, it is evident that because the inflows are less than outflows, we see a case of negative gearing of an amount equal to $15,000.

Now suppose that the year has passed, and Bob’s annual income is $150,000 from his full-time job. As he has faced a loss of $15,000, the amount will be reduced, and his total taxable income will now be $135,000.

Bob is essentially saving the tax incurred equivalent to the loss amount on his annual earnings.

Risks Associated with Negative Gearing

1. Lack of cash flow for repayments

Negative gearing can lead to a high risk for the investor. The biggest risk is when he borrows money for buying the investment property. It is possible that the investor may not have enough cash flows to make the interest and principal payments on the loan.

2. Lack of tenants (and loss of rental payments)

The risk can also arise if the investor is unable to find a tenant and the property is unoccupied for a long time, leading to a loss of rental payments.

3. Significant property depreciation

Another risk can arise in the form of significant value depreciation of the property or any changes in tax laws that may be unfavorable for the investor.

All the things above must be accounted for when deciding to invest in a property to avoid a negative gearing situation.

Related Readings

CFI offers the Commercial Banking & Credit Analyst (CBCA)™ certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following resources will be helpful:

Analyst Certification FMVA® Program

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

Additional Questions & Answers

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover:

- What is Financial Modeling?

- How Do You Build a DCF Model?

- What is Sensitivity Analysis?

- How Do You Value a Business?