Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Understand all the various types of "cash flow"

Finance professionals will frequently refer to EBITDA, Cash Flow (CF), Free Cash Flow (FCF), Free Cash Flow to Equity (FCFE), and Free Cash Flow to the Firm (FCFF – Unlevered Free Cash Flow), but what exactly do they mean? There are major differences between EBITDA vs Cash Flow vs FCF vs FCFE vs FCFF and this Guide was designed to teach you exactly what you need to know!

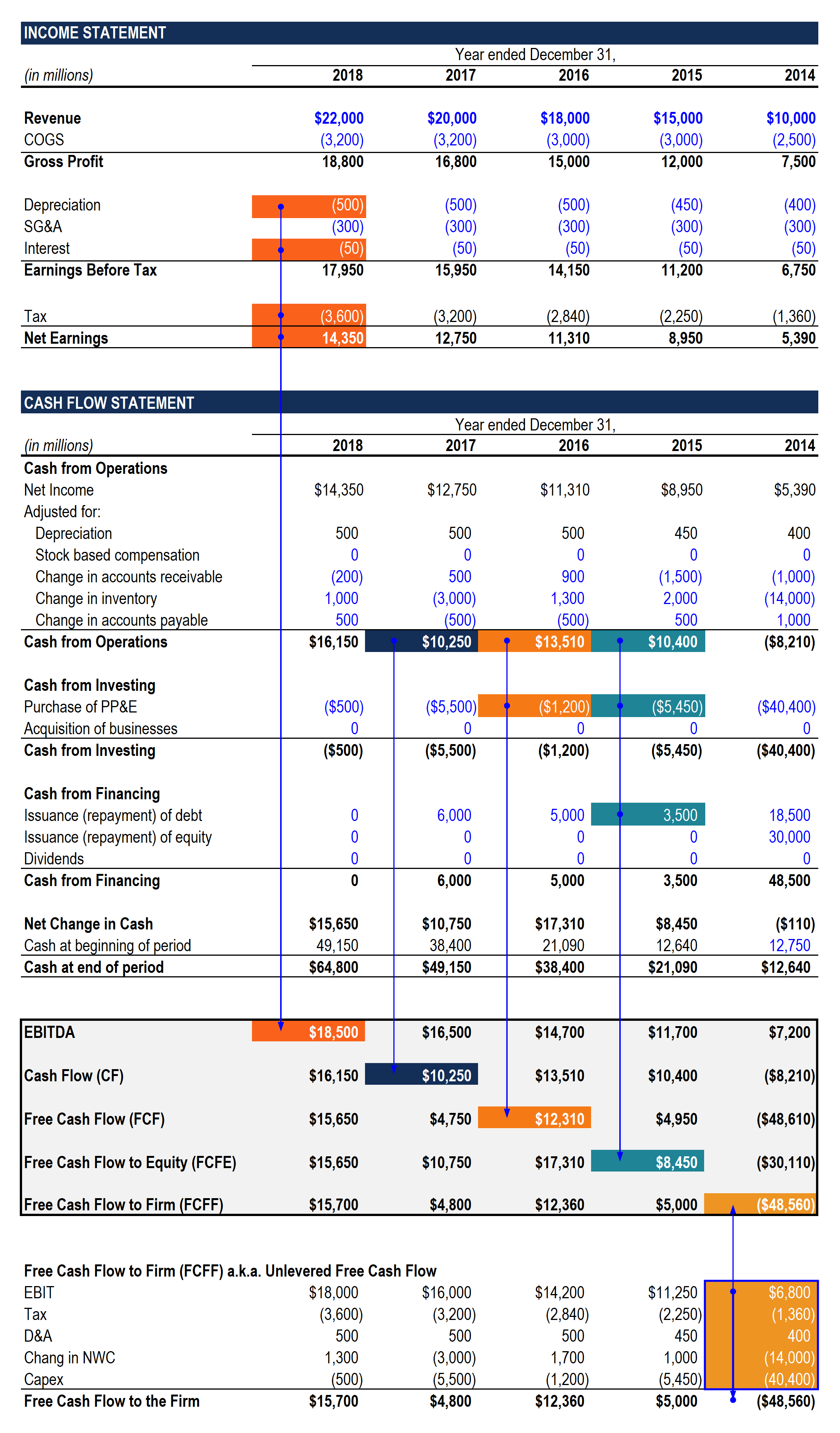

Below is an infographic that we will break down in detail in this guide:

CFI has published several articles on the most heavily referenced finance metric, ranging from what is EBITDA to the reasons Why Warren Buffett doesn’t like EBITDA.

In this cash flow (CF) guide, we will provide concrete examples of how EBITDA can be massively different from true cash flow metrics. It is often claimed to be a proxy for cash flow, and that may be true for a mature business with little to no capital expenditures.

EBITDA can be easily calculated off the income statement (unless depreciation and amortization are not shown as a line item, in which case it can be found on the cash flow statement). As our infographic shows, simply start at Net Income then add back Taxes, Interest, Depreciation & Amortization and you’ve arrived at EBITDA.

As you will see when we build out the next few CF items, EBITDA is only a good proxy for CF in two of the four years, and in most years, it’s vastly different.

Operating Cash Flow (or sometimes called “cash from operations”) is a measure of cash generated (or consumed) by a business from its normal operating activities.

Like EBITDA, depreciation and amortization are added back to cash from operations. However, all other non-cash items like stock-based compensation, unrealized gains/losses, or write-downs are also added back.

Unlike EBITDA, cash from operations includes changes in net working capital items like accounts receivable, accounts payable, and inventory.

Operating cash flow does not include capital expenditures (the investment required to maintain capital assets).

Free Cash Flow can be easily derived from the statement of cash flows by taking operating cash flow and deducting capital expenditures.

FCF gets its name from the fact that it’s the amount of cash flow “free” (available) for discretionary spending by management/shareholders. For example, even though a company has operating cash flow of $50 million, it still has to invest $10million every year in maintaining its capital assets. For this reason, unless managers/investors want the business to shrink, there is only $40 million of FCF available.

Free Cash Flow to Equity can also be referred to as “Levered Free Cash Flow”. This measure is derived from the statement of cash flows by taking operating cash flow, deducting capital expenditures, and adding net debt issued (or subtracting net debt repayment).

FCFE includes interest expense paid on debt and net debt issued or repaid, so it only represents the cash flow available to equity investors (interest to debt holders has already been paid).

FCFE (Levered Free Cash Flow) is used in financial modeling to determine the equity value of a firm.

Free Cash Flow to the Firm or FCFF (also called Unlevered Free Cash Flow) requires a multi-step calculation and is used in Discounted Cash Flow analysis to arrive at the Enterprise Value (or total firm value). FCFF is a hypothetical figure, an estimate of what it would be if the firm was to have no debt.

Here is a step-by-step breakdown of how to calculate FCFF:

This is the most common metric used for any type of financial modeling valuation.

| EBITDA | Operating CF | FCF | FCFE | FCFF | |

|---|---|---|---|---|---|

| Derived From | Income statement | Cash Flow Statement | Cash Flow Statement | Cash Flow Statement | Separate Analysis |

| Used to determine | Enterprise value | Equity value | Enterprise value | Equity | Enterprise value |

| Valuation type | Comparable Company | Comparable Company | DCF | DCF | DCF |

| Correlation to Economic Value | Low/Moderate | High | High | Higher | Highest |

| Simplicity | Most | Moderate | Moderate | Less | Least |

| GAAP/IFRS metric | No | Yes | No | No | No |

| Includes changes in working capital | No | Yes | Yes | Yes | Yes |

| Includes taxe expense | No | Yes | Yes | Yes | Yes (re-calculated) |

| Includes CapEx | No | No | Yes | Yes | Yes |

The answer is, it depends. They likely don’t mean EBITDA, but they could easily mean Cash from Operations, FCF, and FCFF.

Why is it so unclear? The fact is, the term Unlevered Free Cash Flow (or Free Cash Flow to the Firm) is a mouth full, so finance professionals often shorten it to just Cash Flow. There’s really no way to know for sure unless you ask them to specify exactly which types of CF they are referring to.

The answer to this question is, it depends. EBITDA is good because it’s easy to calculate and heavily quoted, so most people in finance know what you mean when you say EBITDA. The downside is that EBITDA can often be very far from cash flow.

Operating Cash Flow is great because it’s easy to grab from the cash flow statement and represents a true picture of cash flow during the period. The downside is that it contains “noise” from short-term movements in working capital that can distort it.

FCFE is good because it is easy to calculate and includes a true picture of cash flow after accounting for capital investments to sustain the business. The downside is that most financial models are built on an unlevered (Enterprise Value) basis, so it needs some further analysis. Compare Equity Value and Enterprise Value.

FCFF is good because it has the highest correlation of the firm’s economic value (on its own, without the effect of leverage). The downside is that it requires analysis and assumptions to be made about what the firm’s unlevered tax bill would be. This metric forms the basis for the valuation of most DCF models.

CF is at the heart of valuation. Whether it’s comparable company analysis, precedent transactions, or DCF analysis. Each of these valuation methods can use different cash flow metrics, so it’s important to have an intimate understanding of each.

In order to continue developing your understanding, we recommend our financial analysis course, our business valuation course, and our variety of financial modeling courses in addition to this free guide.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

We hope this guide has been helpful in understanding the differences between EBITDA vs Cash from Operations vs FCF vs FCFF.

CFI is the global provider of the Financial Modeling and Valuation Analyst (FMVA)™ certification program, designed to help anyone become a world-class financial analyst. To help you advance as an analyst and take your finance skills to the next level, check out the additional free resources below: