Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The amount of cash a business generates that is available to be potentially distributed to shareholders

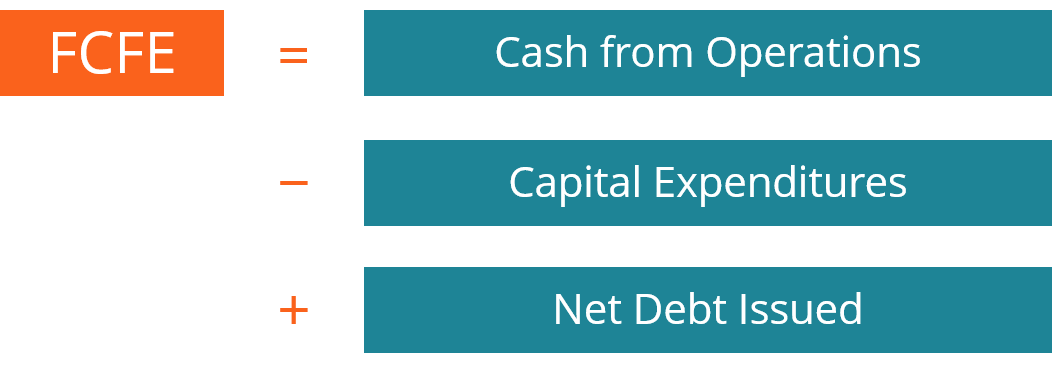

Free cash flow to equity (FCFE) is the amount of cash a business generates that is available to be potentially distributed to shareholders. It is calculated as Cash from Operations less Capital Expenditures plus net debt issued. This guide will provide a detailed explanation of why it’s important and how to calculate it, along with several examples.

Let’s look at how to calculate Free Cash Flow to Equity (FCFE) by examining the formula. It can easily be derived from a company’s Statement of Cash Flows.

Formula:

FCFE = Cash from Operating Activities – Capital Expenditures + Net Debt Issued (Repaid)

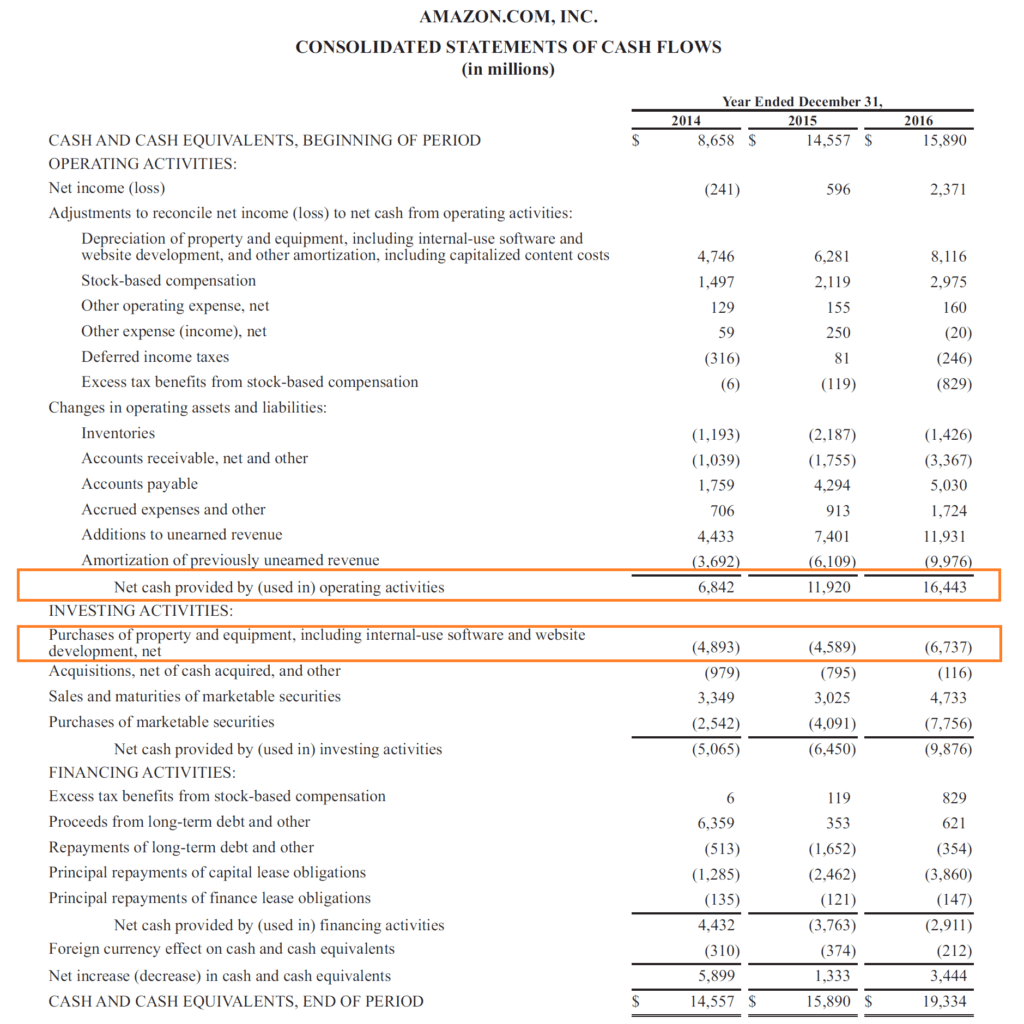

Below is a screenshot of Amazon’s 2016 annual report and statement of cash flows, which can be used to calculate free cash flow to equity for years 2014 – 2016.

As you can see in the image above, the calculation for each year is as follows:

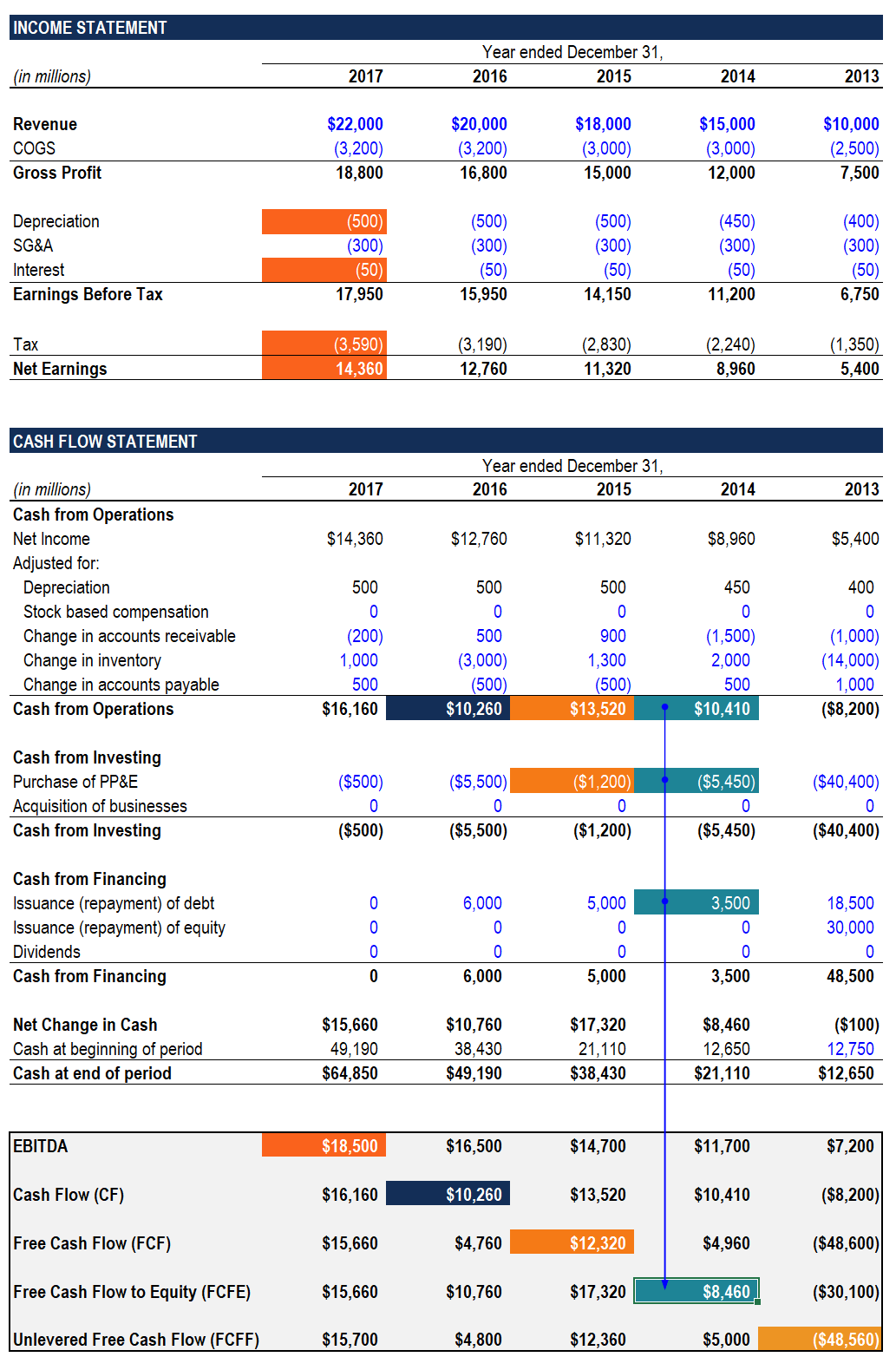

Let’s look at an Excel spreadsheet a financial analyst would use to perform an FCFE analysis for a company.

As you can see in the figures below, the company has a clearly laid out Statement of Cash Flows, which includes three sections: Operations, Investments, and Financing.

In 2018, the company reported cash from operations of $23,350 million, spent $500 million on purchasing property, plant, and equipment (PP&E) and issued no new debt, which results in an FCFE of $22,850 million.

In 2014, the numbers tell a very different story, the company reported cash from operations of -$5,490 million, spent $40,400 million on purchasing property, plant, and equipment (PP&E) and issued $18,500 million of debt, which results in an FCFE of -$27,390 million.

As you can see, in one year the company posted very positive FCFE and in another year, it was very negative, even though operating activities weren’t as dissimilar. The reason for this was the significant investment that was made in purchasing additional PP&E.

Since equity investors must fund the purchase of such assets, the Free Cash Flow to Equity figure must account for this.

FCFF stands for Free Cash Flow to the Firm and represents the cash flow that’s available to all investors in the business (both debt and equity).

The only real difference between the two is interest expense and their impact on taxes. Assuming a company has some debt, its FCFF will be higher than FCFE by the after-tax cost of debt amount.

To learn more about FCFF and how to calculate it, read CFI’s Ultimate Cash Flow Guide.

When valuing a company, it’s important to distinguish between the Enterprise Value and Equity Value. The Enterprise Value is the value of the entire business without taking its capital structure into account. Equity Value is the value attributable to shareholders, which includes any excess cash and exclude all debt and financial obligations.

The type of value you’re trying to arrive at will determine which cash flow metric you should use.

Use FCFE to calculate the net present value (NPV) of equity.

Use FCFF to calculate the net present value (NPV) of the enterprise.

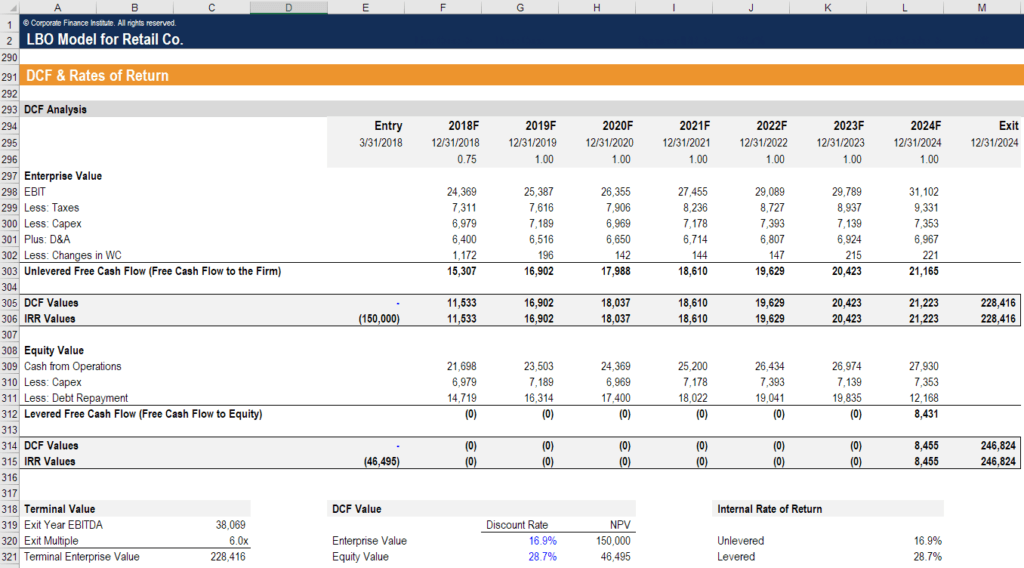

As you can see in the image above from CFI’s LBO Financial Modeling Course, an analyst can build a schedule for both Firm-wide and Equity-only cash flows.

Here are a couple of ways you can arrive at FCFE Formula from different Income Statement Items:

How to Calculate FCFE from Net Income

How to Calculate FCFE from EBIT

How to Calculate FCFE from CFO

How to Calculate FCFE from EBITDA

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading this guide to FCFE and why it’s an important metric in corporate finance. To continue developing your career as an analyst, please check out these supplemental resources: